Tag: men vs. women

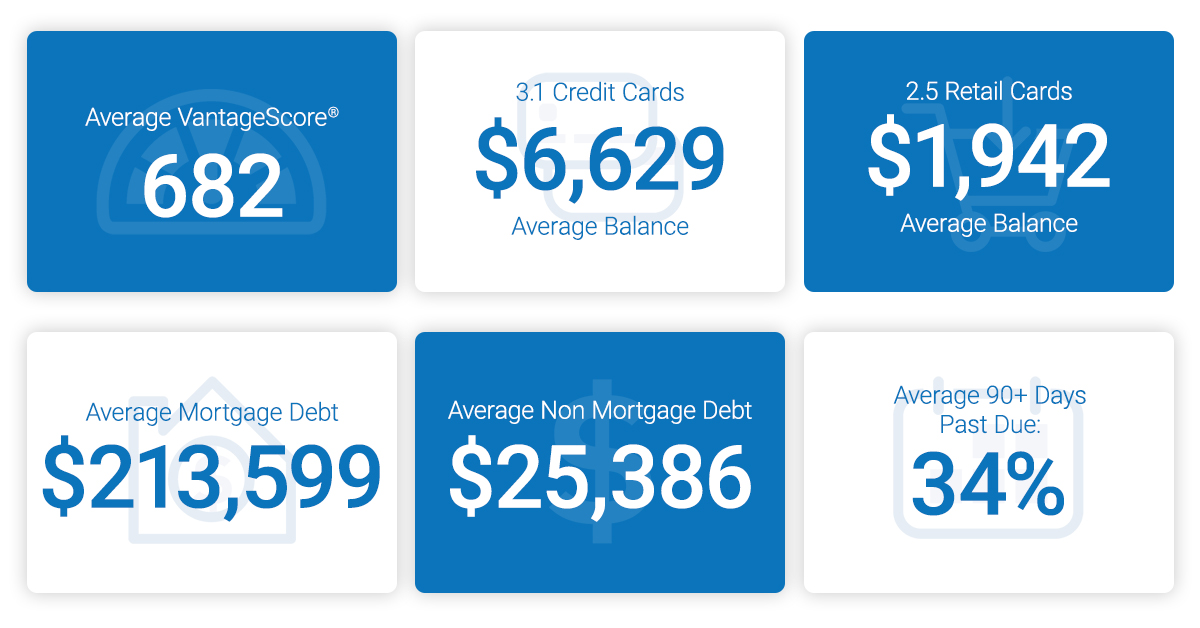

As consumers prepare for the next decade, we look at how we’re rounding out this year. The results? The average American credit score is 682, an eight-year high. Experian released the 10th annual state of credit report, which provides a comprehensive look at the credit performance of consumers across America by highlighting consumer credit scores and borrowing behaviors. And while the data is spliced to show men vs. women, as well as provides commentary at the state and generational level, the overarching trend is up. Even with the next anticipated economic correction often top of mind for financial institutions, businesses and consumers alike, 2019 was a year marked by more access, more spending and decreasing delinquencies. Things are looking up. “We are seeing a promising trend in terms of how Americans are managing their credit as we head into a new decade with average credit scores increasing two points since 2018 to 682 – the highest we’ve seen since 2011,” said Shannon Lois, Senior Vice President and Head of EAS, Analytics, Consulting & Operations for Experian Decision Analytics. “Average credit card balances and debt are up year over year, yet utilization rates remain consistent at 30 percent, indicating consumers are using credit as a financial tool and managing their debts responsibly.” Highlights of Experian’s State of Credit report: 3-year comparison 2017 2018 2019 Average number of credit cards 3.06 3.04 3.07 Average credit card balances $6,354 $6,506 $6,629 Average number of retail credit cards 2.48 2.59 2.51 Average retail credit card balances $1,841 $1,901 $1,942 Average VantageScore® credit score[1, 2] 675 680 682 Average revolving utilization 30% 30% 30% Average nonmortgage debt[3] $24,706 $25,104 $25,386 Average mortgage debt $201,811 $208,180 $231,599 Average 30 days past due delinquency rates 4.0% 3.9% 3.9% Average 60 days past due delinquency rates 1.9% 1.9% 1.9% Average 90+ days past due delinquency rates 7.3% 6.7% 6.8% In the scope of the credit score battle of the sexes, women have a four-point lead over men with an average credit score of 686 compared to 682. Their lead is a continued trend since 2017 where they’ve bested their male counterparts. According to the report, while men carry more non-mortgage and mortgage debt than women, women have more credit cards and retail cards (albeit they carry lower balances). Generationally, Generations X, Y and Z tend to carry more debt, including mortgage, non-mortgage, credit card and retail card, than older generations with higher delinquency and utilization rates. Segmented by state and gender, Minnesota had the highest credit scores for both men and women, while Mississippi was the state with the lowest average credit score for females and Louisiana was the lowest average credit score state for males. As we round out the decade and head full-force into 2020, we can reflect on the changes in the past year alone that are helping consumers improve their financial health. Just to name a few: Experian launched Experian BoostTM in March, allowing millions of consumers to add positive payment history directly to their credit file for an opportunity to instantly increase their credit score. Since then, there has been over 13 million points boosted across America. Experian LiftTM was launched in November, designed to help credit invisible and thin-file consumers gain access to fair and affordable credit. Long-standing commitments to consumer education, including the Ask Experian Blog and volunteer work by Experian’s Education Ambassadors, continue to offer assistance to the community and help consumers better understand their financial actions. From what we can tell, this is just the beginning. “Understanding the factors that influence their overall credit profile can help consumers improve and maintain their financial health,” said Rod Griffin, Experian’s director of consumer education and awareness. “Credit can be used as a financial tool. Through this report, we hope to provide insights that will help consumers make more informed decisions about credit use as we prepare to head into a new decade.” Learn more 1 VantageScore® is a registered trademark of VantageScore Solutions, LLC. 2 VantageScore® credit score range is 300 to 850. 3 Average debt for this study includes all credit cards, auto loans and personal loans/student loans.

It’s the “Battle of the Sexes” credit edition. Who sports higher scores, less debt and more on-time payments? According to Experian’s latest analysis, women take the credit title. Thank you very much. The report analyzed multiple categories including credit scores, average debt, number of open credit cards, utilization ratios, mortgage amounts and mortgage delinquencies of men and women in the United States. Results revealed: Women’s average credit score of 675 compared to men’s score of 670 Women have 3.7 percent less average debt than men Women have 23.5 percent more open credit cards Women and men have the same revolving utilization ratio of 29.9 percent Women’s average mortgage loan amount is 7.9 percent less than men’s Women have a lower incidence of late mortgage payments by 8.1 percent “There were several gaps between men and women in this study, including the five-point credit score lead that the women hold,” said Michele Raneri, Experian’s Vice President of Analytics and New Business Development. “Even with more credit cards, women have fewer overall debts and are managing to pay those debts on time.” The report also takes a look at the vehicle preferences of men and women and how those choices play into their overall credit and financial health. Below are the top-line results: Women were more likely to purchase a more functional, utilitarian vehicle, while men tended to lean toward sports cars and trucks The top three vehicle segments men purchased in 2015 were mid-size pickup trucks, large pickup trucks and standard specialty cars. In fact, they were 1.37 times more likely to purchase a mid-sized pickup truck than the general population The top three vehicle segments for women were small crossover-utility vehicles, mid-size sports-utility vehicles and compact crossover-utility vehicles. Women were 1.40 times more likely to purchase the small crossover-utility vehicle than the general population Experian conducted a similar study, comparing men and women on various credit attributes in 2013. At that time, women also scored higher than men in the credit score category - holding steady with a 675 VantageScore® credit score compared to the men’s 674 VantageScore® credit score, but the gap has widened, with the men’s score further lowering to 670. While men’s scores have dropped since 2013, the overall financial health for both sexes is strong. Most notably, the mortgage 60-plus delinquency rate has dropped significantly. In the 2013 pull, men were tracking at 5.7 percent and women were 5.3 percent. Today, those numbers have dropped to .86 percent for men and .79 percent for women. What a difference a few years has made in regards to the recovering housing market. Time will tell if the country’s state of credit will continue to trend higher, as indicated in the 2015 annual report, or if the buzz of potential recession and an election year will reverse the positive trend. As for now, the women once again claim bragging rights as it pertains to credit. Analysis methodology The analysis is based on a statistically relevant, sampling of depersonalized data of Experian’s consumer credit database from December 2015. Gender information was obtained from Experian Marketing Services.