You just finished redeveloping an existing scorecard, and now it’s time to replace the old with the new. If not properly planned, switching from one scorecard to another within a decisioning or scoring system can be disruptive. Once a scorecard has been redeveloped, it’s important to measure the impact of changes within the strategy as a result of replacing the old model with the new one. Evaluating such changes and modifying the strategy where needed will not only optimize strategy performance, but also maximize the full value of the newly redeveloped model. Such an impact assessment can be completed with a swap set analysis.

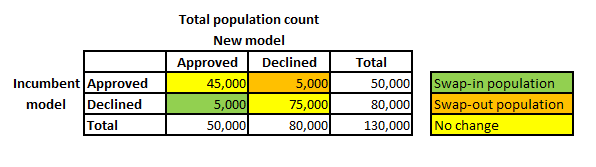

The phrase swap set refers to “swapping out” a set of customer accounts — generally bad accounts — and replacing them with, or “swapping in,” a set of good customer accounts. Swap-ins are the customer population segment you didn’t previously approve under the old model but would approve with the new model. Swap-outs are the customer population segment you previously approved with the old model but wouldn’t approve with the new model. A worthy objective is to replace bad accounts with good accounts, thereby reducing the overall bad rate. However, different approaches can be used when evaluating swap sets to optimize your strategy and keep:

- The same overall bad rate while increasing the approval rate.

- The same approval rate while lowering the bad rate.

- The same approval and bad rate but increase the customer activation or customer response rates.

It’s also important to assess the population that doesn’t change — the population that would be approved or declined using either the old or new model. The following chart highlights the three customer segments within a swap set analysis.

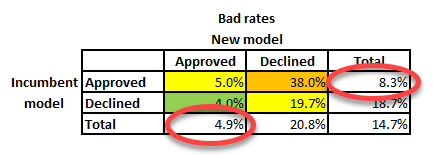

With the incumbent model, the bad rate is 8.3%. With the new model, however, the bad rate is 4.9%. This is a reduction in the bad rate of 3.4 percentage points or a 41% improvement in the bad rate.

This type of planning also is beneficial when replacing a generic model with another or a custom-developed model.

Click here to learn more about how the Experian Decision Analytics team can help you manage the impacts of migrating from a legacy model to a newly developed model.