At A Glance

Introducing Experian Credit + Cashflow Score, our most advanced credit decisioning model yet, integrating unparalleled data to expand credit access and empower consumers.Every credit decision relies on data, but traditional credit information may capture only part of a consumer’s financial story. Some of that story is reflected in credit reports, the loans repaid, the cards managed, and the steady progress toward financial goals. Others live quietly in bank statements and transaction histories, like the rent paid on time, the savings set aside, and the bills managed responsibly.

Yet for millions of consumers, that second story has rarely been part of the credit conversation.

Expanding the credit conversation can give lenders and financial institutions an edge, helping them separate genuine risk from missed opportunity. In a lending environment defined by volatility and evolving consumer habits, having a more complete picture of each applicant can help make the difference between sustainable growth and risk management.

At the same time, open-banking frameworks and consumer-permissioned data have made it possible to understand financial health more clearly than traditional models. That’s where Experian’s Credit + Cashflow Score comes in.

A unified view of credit and cash flow

The Credit + Cashflow Score is the first-of-its-kind model combining multiple data sources into a single score. Based on our pre-production analytics, early results demonstrate a 40% improvement in predictive accuracy compared with conventional credit models.

It unites our proprietary and industry-leading credit data, alternative credit insights, 24 months of trended behavior, and consumer-permissioned cashflow information into a single score ranging from 300 to 850.* This goes beyond cashflow-augmented models that rely primarily on transaction data layered over credit files.

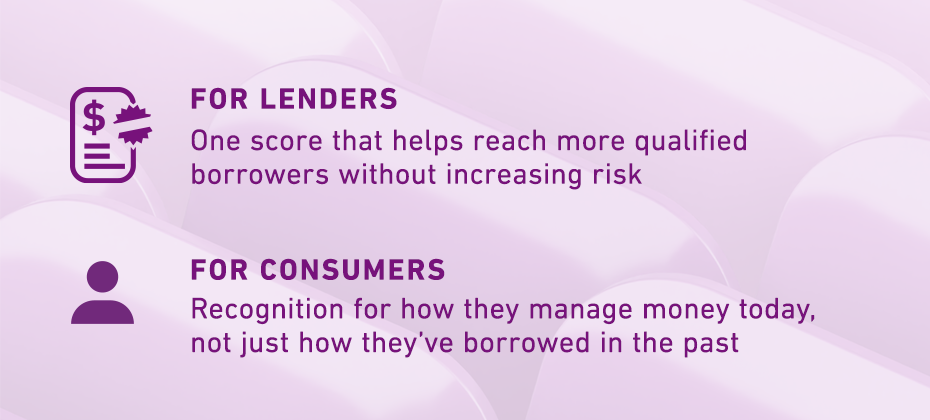

The result is a data-rich assessment of creditworthiness that allows lenders to strengthen portfolio performance, maintain disciplined risk management, and help identify qualified borrowers that traditional credit models might overlook.

Better risk control and stronger growth

Today’s lending landscape is being reshaped by rising interest rates, increased capital costs, and heightened regulatory oversight. These pressures are prompting institutions to tighten underwriting standards and reassess risk strategies as they navigate an uncertain economy. At the same time, competition for qualified borrowers continues to intensify, creating pressure to drive sustainable growth without compromising credit quality.

Meanwhile, on the consumer side, people are earning income through gig work or multiple income streams and using alternative financial products. According to our recent market estimates, 62 million U.S. consumers are thin-file or credit-invisible1. This is making it harder for lenders to assess true financial capacity using credit data alone.

Traditional credit scores continue to remain important, but they can potentially miss key indicators of stability and affordability that appear only in transactional data. The Credit + Cashflow Score bridges that gap, helping enable lenders to expand approvals responsibly while maintaining disciplined risk management.

See what’s next

As credit markets continue to evolve, lenders are looking for new ways to balance growth with risk. Having the whole financial picture may allow organizations to grow stronger portfolios, reach more qualified borrowers, and bring financial opportunity to more people.

Partner with Experian to leverage decades of credit expertise, the nation’s largest alternative credit bureau, and industry-leading open-banking solutions to help lenders innovate responsibly.

The Credit + Cashflow Score is built to deliver measurable performance lift, model transparency, and ease of integration through the Experian Ascend Platform.

* New score available in pre-production for analytics

1https://www.experian.com/thought-leadership/business/the-roi-of-alternative-data