As a follow‑up to our January post on Freddie Mac’s Loan-Level Directed Collateral (LLDC) program and its use of new loan‑level data fields from Experian’s Mortgage Loan Performance (MLP) dataset, we’re highlighting another newly available field: current second lien balance.

What kind of data moves markets?

Before diving into the new second lien field, we’ll outline the criteria we use to determine whether a new data field has the potential to move MBS markets—and therefore warrants the time and effort required to prepare and deliver it to our institutional investor clients. These criteria will apply to all new fields discussed in future posts.

Over the past decade, rapid technological innovation, combined with financial markets’ increasing focus on data and AI, has led to a steady stream of new market data and analytical products. Most of these releases don’t materially impact how MBS trade. As discussed in prior posts, two notable exceptions stand out:

- The introduction of pool‑level data in the 1980s enabled the rise of specified (“spec”) pools.

- The public release of agency MBS loan‑level data in 2013 ushered in a new era of advanced analytics and precision modeling.

So, what criteria must be met for new, incremental data to change how MBS trades? We believe three requirements must be met:

- New: Provides information not available in existing datasets (i.e., orthogonal to currently available data).

- Material: Impacts a sizeable portion of the MBS universe.

- Significant: Differentiates collateral performance by a large enough margin to influence trading and risk management decisions.

With these criteria in mind, we turn to one of several new fields from Experian’s MLP that meet all three: current second lien balance.

Subsequent Second Liens: An ‘Invisible’ CPR Throttle

MLP contains several fields related to open second liens, with each loan linked to both the individual borrower and the specific property. This structure allows visibility into a borrower’s full set of open second lien loans, even across multiple properties. For the illustrative exercise below, we focus on one field: the total balance on open second‑mortgage trades reported in the past three months.

Does this field meet the first criteria—New? Yes, the current presence of junior liens is new information in agency MBS markets. In standard agency and Government National Mortgage Association (GNMA) disclosures, second‑lien information appears only at the time of first‑lien origination. Any subsequent second liens remain unreported, preventing accurate calculations of current combined LTV post-origination.

The material blind spot: Missing junior‑lien data

The absence of updated junior lien status represents a material blind spot for investors seeking to predict prepayment behavior of the associated first lien in agency MBS. Current combined LTV, inclusive of subsequently opened second liens and adjusted for home price appreciation (HPA), is one of the most important drivers of both prepayment and credit performance. Without supplementary data from MLP, information on newly originated second liens go unobserved. As a result, prepayment and credit forecasts become overly aggressive, and prepayment call protection is therefore mispriced.

In addition to information regarding the junior lien loan, Experian’s MLP dataset includes a monthly refreshed AVM value for each property, ensuring an accurate current CLTV value. Having established newness, is current junior lien data material? Yes, particularly in the current environment of record-high home equity. Approximately 16% of active mortgages carry second liens, representing roughly $522 billion in outstanding balances—and growing (Source: Experian MLP dataset). In 2024 alone, second-lien originations exceeded $100 billion and continued to trend upward (Source: Experian MLP dataset).

Second liens added after primary‑mortgage origination, often layered onto low‑LTV agency MBS, aren’t captured in standard GSE data. Their impact is especially pronounced in periods of moderate or negative HPA. Borrowers who take on new second liens and then experience negative HPA may be unable to refinance due to re‑subordination limits, which materially affect prepayment behavior and call protection. Investors relying on standard agency disclosure have no visibility into post‑origination junior liens.

Is current junior‑lien data significant?

After having established newness and materiality, is the current junior lien data significant?

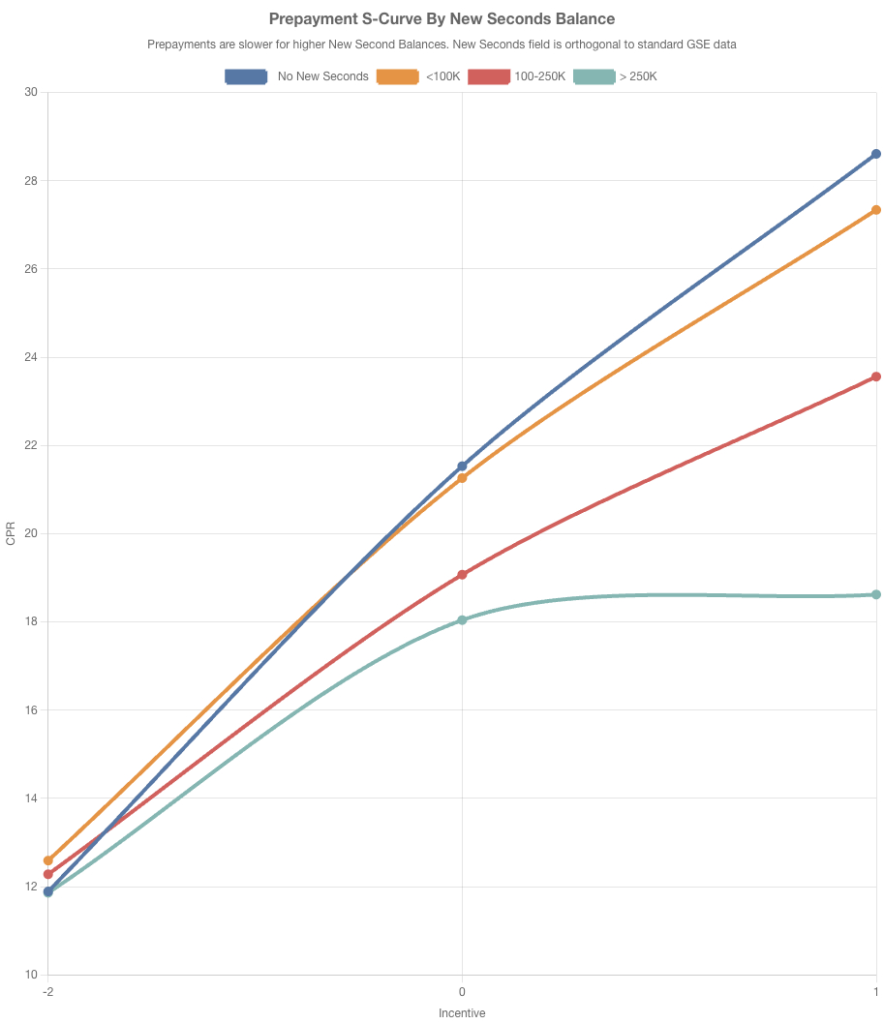

Yes—Figure 1 illustrates the impact of new second-lien balances on prepayments. This field is independent of other collateral characteristics available in standard GSE data, as the decision to take out a new second lien is made by the borrower after the primary mortgage has closed.

As shown in Figure 1, prepayments decline materially as new second-lien balances increase. On average, if approximately 20% of mortgages carry second liens and the CPR differential for in-the-money (ITM) mortgages with and without new second liens are 10 CPR, then new second liens account for roughly 2 CPR of prepayment impact on average (10 CPR × 20%).

This CPR-throttling effect is significantly more pronounced for mortgages with a current CLTV of around 80%. These loans may be effectively locked out of refinancing due to re-subordination constraints, yet they appear highly callable when evaluated using only standard GSE data, leading to materially overstated prepayment expectations.

Fig 1. Prepayments S-Curve: New Second Liens Balance Source: Experian Mortgage Loan Performance Dataset, hosted on the IVolatility MBS Data-Driven Portal

_____________________________________________________

Michael Pyatski advises MBS traders, portfolio managers, quants, risk managers, loan originators, and technology professionals on making informed, data-driven business decisions that drive revenue growth, enhance risk management, and reduce trading costs.

With more than 15 years of experience as an Agency RMBS trader—including serving as Head of the Proprietary Trading Desk at BNP Paribas—Michael developed and successfully implemented relative-value, data-driven profitable trading strategies to capture market opportunities embedded in data but not fully priced by the market. His trading experience, combined with a Ph.D. in econometrics, led him to found the Data-Driven Portal (https://datadrivenportal.com/), a platform that provides advanced technology for MBS trading and risk management.

The platform’s No-Model Data-Driven technology leverages big data, econometric analysis, and AI to help traders identify relative-value opportunities in RMBS markets and generate above-market, risk-adjusted returns.

_____________________________________________________