Since mortgage rates have remained high even after recent Federal Reserve rate-cutting activity, there is limited rate incentive to refinance for the vast majority of borrowers. In the absence of significant rate incentive, borrower mobility and behavioral tendencies have become outsized drivers of both prepayment speeds and origination volumes.

Unfortunately, traditional MBS market data does not contain adequate information for investors to analyze either borrower mobility or behavioral tendencies like sources of payoff funds (i.e., cash payoff, refinance of existing loan, opening of a new lien on a 2nd home, etc.).

By using Experian’s Mortgage Loan Performance (MLP) Dataset, a monthly-updated time series featuring combined loan, borrower, and property-level details covering nearly the entire US mortgage market since 2005, it’s possible to examine patterns in behavior for borrowers who have prepaid their loans early, such as:

- The proportion of paid-off borrowers who retain the subject property (“stayers”) versus those who move (“movers”); and for both of these subsets, the percentage of people who re-enter the mortgage market with a new loan (“returners”) compared to those who leave the mortgage market after paying off their loan (“leavers”). Classification as returner or leaver in the charts below is based on whether the paid-off borrower opened a new mortgage loan as of the end-of-August observation date.

- Sources of mortgage payoff funds — what proportion of pay-off was via refinance of the subject property vs. opening a new lien on a 2nd home or investment property? What proportion pays off in cash resultant from a sale of the subject property or cash out-of-pocket while retaining the subject property?

- For the set of returners, what is the typical time lapse between payoff and opening of a new mortgage, i.e., are most payoffs simultaneous or are a significant number of borrowers utilizing bridge financing, or paying off a current loan while they shop for a new home and new loan?

- For the set of leavers, what are the credit, income and demographic characteristics of these borrowers? Are they leaving the mortgage market because they are unable to get a new loan due to weak credit or insufficient income?

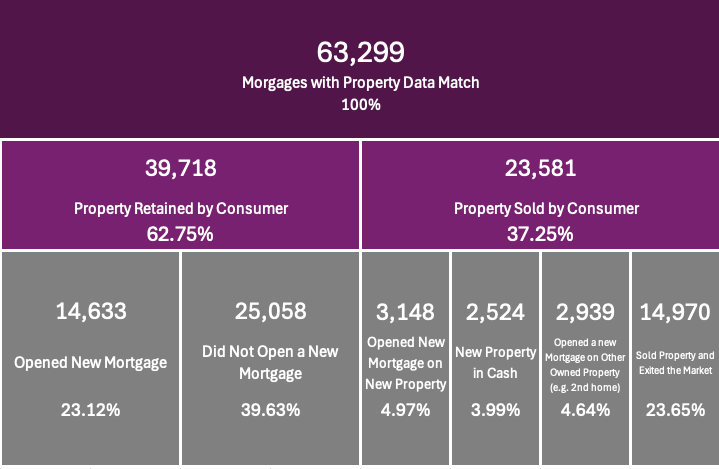

Mobility and source of payoff cash dynamics are summarized below for a sample of ~ 63,000 mortgage payoff events, drawn from MLP, which occurred from February to July 2025.

Amongst other trends, we see that approximately 70% of borrowers who paid off their loan exited the mortgage market (~40% retained property after a cash payoff + ~4% sold property and bought a new property in cash + ~24% sold property and didn’t purchase another property). This high proportion is probably driven in part by the relative lack of rate/term refinance and purchase activity given the current rate environment.

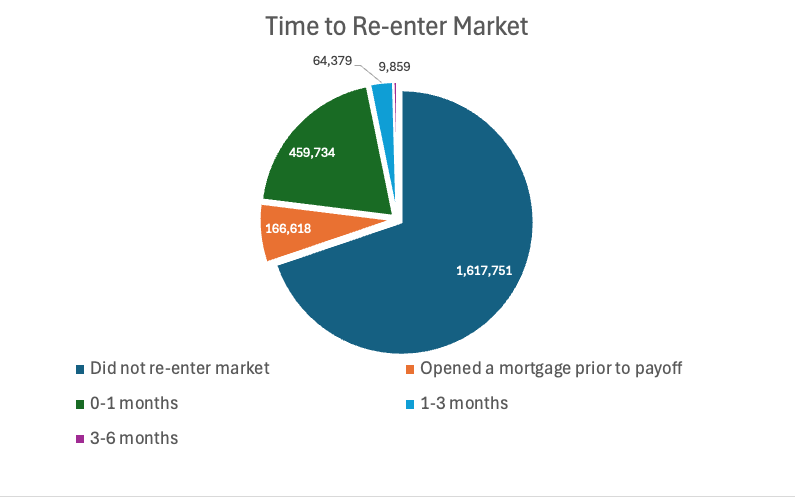

When we look at all payoffs in MLP over the same time period — 2.3 million payoff events — the ~70% proportion of leavers holds. Within this larger sample, we also break down time to re-entry for the returners. Unsurprisingly, of the 30% returners, the vast majority open a new loan just prior to or within a month of prepayment:

Since MLP contains monthly-refreshed, joined credit profile data for every mortgaged borrower, we can also examine the credit and income characteristics of leavers to determine if poor credit or limited income prohibited re-entry. This analysis reveals that leavers are generally not credit or income limited; the pool of leavers is characterized by the following average metrics:

- 746 current Vantage 3.0 credit score

- 49 years of age

- $99,759 current modeled income

- 34.8 back-end DTI

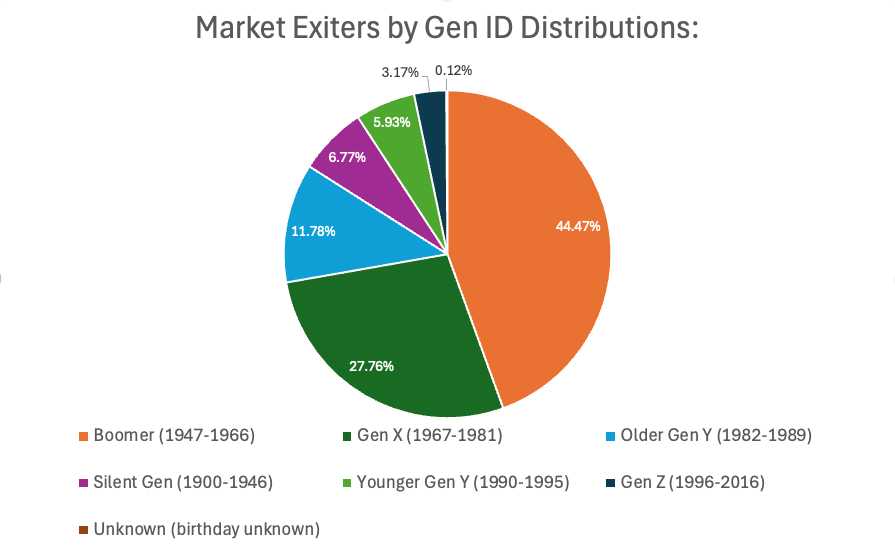

The following table stratifies the leaver population by generation:

Further segmentation by loan servicer, originator and borrower credit profile (e.g., dollar amount of student loan debt outstanding) and past behavior (e.g., how many mortgages has this borrower refinanced in the past?) across all tradelines are potential next steps.

As the rates environment evolves, we will monitor mobility trends, the ratio of borrowers paying off loans while moving versus those staying, and how borrowers decide to finance their prepayments.

In addition to rates, changes in HPI, unemployment and underwriting guidelines will influence these behaviors.

By leveraging new datasets like MLP which capture not only loan performance, but also regularly refreshed credit profile, behavioral trends and property details over the entire credit lifespan of a consumer and all their tradelines, investors can incorporate a 360-degree view of loan, borrower and property into their predictive analyses.