At A Glance

Summary Borrower risk continues to evolve after loan origination. Credit scores, income, debt-to-income ratios, and escrow costs all change over time, shaping mortgage performance in ways traditional market data can’t track. This article uses Experian’s Mortgage Loan Performance dataset to uncover how borrower credit profiles evolve, why those shifts matter for lenders and investors, and how complete visibility into credit, income, and insurance trends can strengthen credit and prepayment risk modeling.After a borrower opens a mortgage, their financial profile doesn’t stay static. Credit scores, debt-to-income ratios (DTI), and annual incomes evolve—sometimes positively, sometimes negatively—depending on both the individual borrower’s specific behavior and situation, as well as broader economic conditions, including factors like unemployment and interest rates. When we factor in rising escrow costs for home insurance and property taxes, the picture becomes even more complex.

Unfortunately, traditional market data for both private label and agency MBS, as well as “servicing” datasets generally used to build analytics for whole loan strategies, contain virtually no information regarding a borrower’s current credit profile. The current pay status of the subject loan is sometimes provided. However, credit score and DTI values (if provided at all) are as of the origination date only. No information is provided regarding the borrower’s home insurance or property tax premiums.

In other words, as a mortgage loan seasons and the borrower’s credit profile drifts as new debts are added or paid off, payments on auto loans, student loans, credit cards, even other mortgages on the subject property are made or missed, and home insurance policy costs double (or triple!) in some cases, MBS investors using traditional market data only are truly flying blind with respect to the borrowers’ current credit health.

Fortunately, more complete alternatives to supplement traditional market data exist. In this article, we’ll analyze Experian’s Mortgage Loan Performance (MLP) data, a monthly-refreshed join across loan level performance, borrower credit profile and property data for all US mortgages since 2005, to explore borrowers’ credit profile drift since loan origination. This dataset contains current credit scores, tradeline balances and performance, escrow account information, and modeled income for all borrowers.

Section 1: Credit Score Migration Since Origination — Who Improves and Who Slumps?

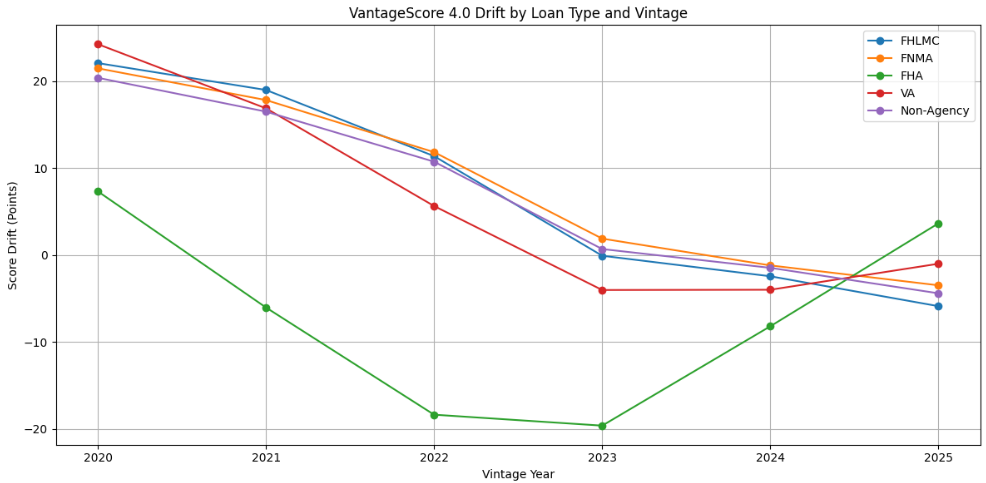

Using the MLP dataset, we examined current and at-origination borrower credit profiles for over 42 million mortgages originated from January 2020 through July 2025. Segmenting the data by different mortgage products shows distinct score migration patterns since loan origination as illustrated in Figure 1:

Conventional Loans (FNMA/FHLMC):

- Conventional borrowers have experienced strong positive gains in credit score since origination for the 2020–2022 vintages with average VantageScore 4.0 migration of +11 to +22 points

- For the more recent 2023-2025 vintages, borrowers have experienced flat or negative drift of averaging -6 to +2 points

FHA Loans:

- FHA borrowers have experienced mostly negative VantageScore 4.0 drift of -6 to -19 points, with the steepest decline to date in the 2022–2023 vintages

VA Loans:

- We see a positive drift for early vintages, especially 2020 to 2022 vintages, but a slightly negative drift for more recent vintages of -1 to -4 points.

Non-Agency Loans:

- Similar to conventional loans, we see a positive credit score drift for 2020–2022 vintages, turning negative for 2024–2025 with an average drift of -1.5 to -4 points

Figure 1: Vantage 4.0 Migration Drift Since Origination[1]

Key Insights: Over the past 6 years, Conventional borrowers have generally improved their credit profile post-origination, notwithstanding small dips to–date for the last couple vintages. On the other extreme, 4 of the 6 last FHA vintages have experienced credit score deterioration to date.

Beyond the obvious increase in delinquency and default risk due to deteriorating credit scores, a borrower’s ability to refinance efficiently is also impacted by credit score deterioration. A loan’s propensity to default or voluntarily refinance is influenced by the borrower’s current credit score, which is absent from traditional market data, though present in MLP. In this way, current credit score is a critical field for both nonagency and agency MBS analyses.

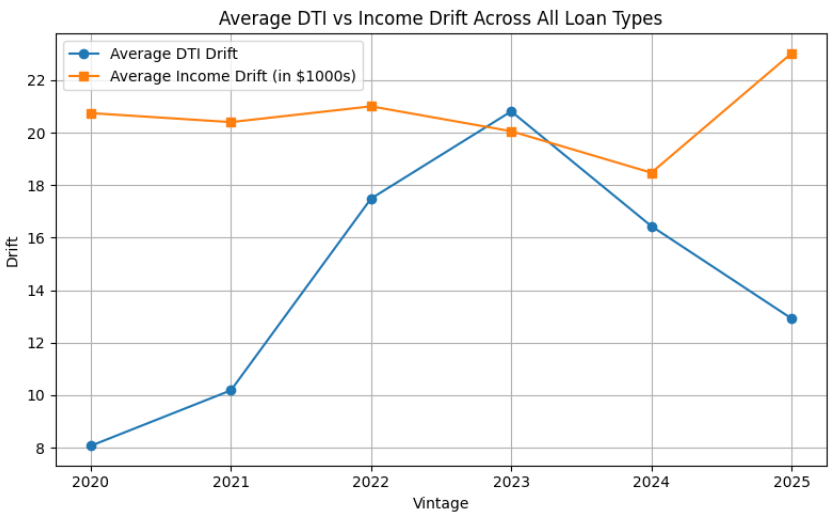

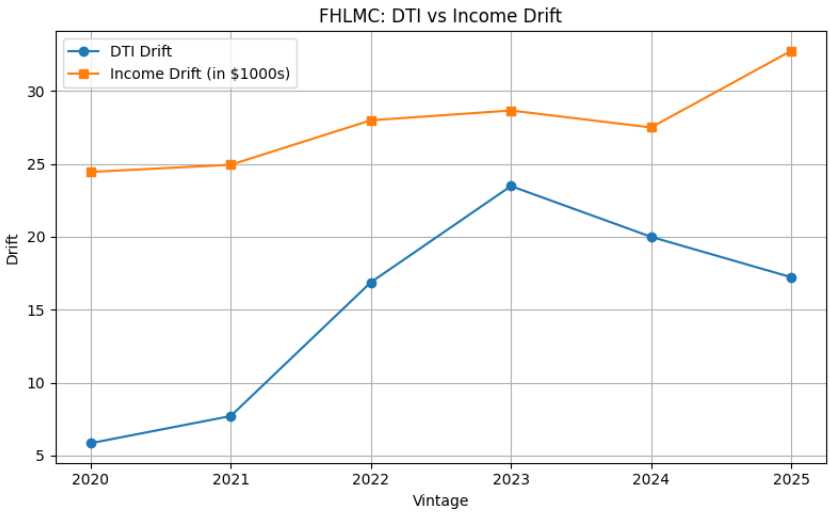

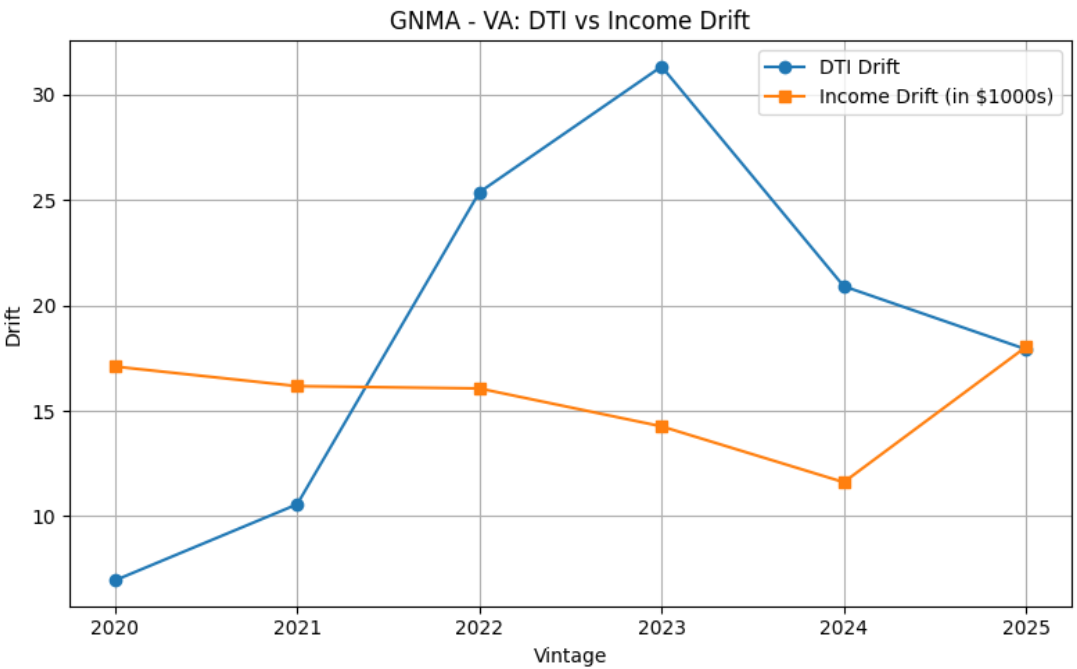

Section 2: DTI and Income

As illustrated in Figures 2 through 4, even as incomes rise, DTI often climbs faster, signaling potential borrower stress:

Example (FHLMC):

- 2020 Vintage: DTI +5.9 points, Income +$24K

- 2023 Vintage: DTI +23.5 points, Income +$28K

Figure 2: DTI and Income Drift Since Origination for all mortgages

Figure 3: DTI and Income Drift Since Origination for Freddie Mac mortgages

Figure 4: DTI and Income Drift Since Origination for GNMA, VA mortgages

Insights: Across all loan types, on average, borrowers are earning more relative to when they opened the loan but also taking on additional obligations over time at an even faster rate, which inflates their debt-to-income ratio. Particularly striking is the DTI drift for the 2023 GNMA VA vintage, rising over 30 points in two years! In addition to elevated risk of delinquency and default, elevated DTI also reduces the borrower’s ability to refinance efficiently by affecting the borrower’s ability to qualify for competitive refinancing rate. Investors relying solely on traditional market data have no vision into the borrower’s current DTI, thereby limiting their ability to model and manage both default and voluntary prepayment risk.

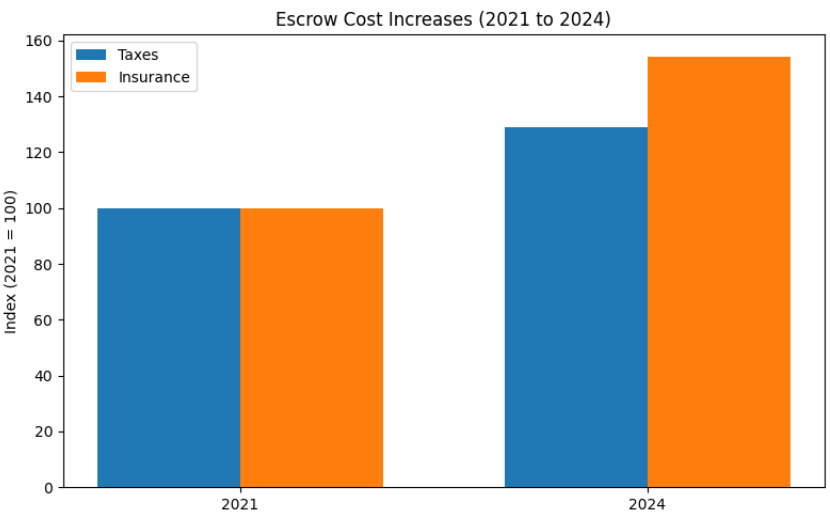

Section 3: Escrow Pressure—Taxes and Insurance Surge

As illustrated in Figure 5, MLP data reveals that from 2021 to 2024:

- Taxes haves increased by an average of 28.8%

- Home Insurance rates have increased by an average of 54.4%, becoming the fastest-growing home ownership expense within this period

Higher escrow payments squeeze borrower budgets, driving increased delinquency risk and decreased affordability. Traditional market data contains no information regarding borrowers’ tax or insurance premium burdens.

Figure 5: Average escrow payment increases from 2021 to 2024

Conclusion

Score migration, evolving income and DTI, and escalating escrow & tax costs create a dynamic risk environment for borrowers. Borrowers’ constantly changing credit health drives both credit (likelihood of default) and voluntary prepayment (credit score and DTI influence both ability and incentive to refinance) risks. In this context, monitoring borrower credit and income post-origination is critical.

Traditional market data for both private label and agency MBS contains no information related to a borrower’s current credit score, DTI, income or tax & escrow burden. Experian’s Mortgage Loan Performance dataset contains all this information, at the loan level, for ~100% of the US mortgage market, enabling better segmentation, predictive modeling, and risk management for both credit and prepayment risk.

Read our previous blog about Residential Mortgage Prepayments

[1] All statistics are derived from Experian’s Mortgage Loan Performance (MLP) Dataset