By: Perry DeFelice & Angad Paintal, Experian, and Michael Pyatski, IVolatility

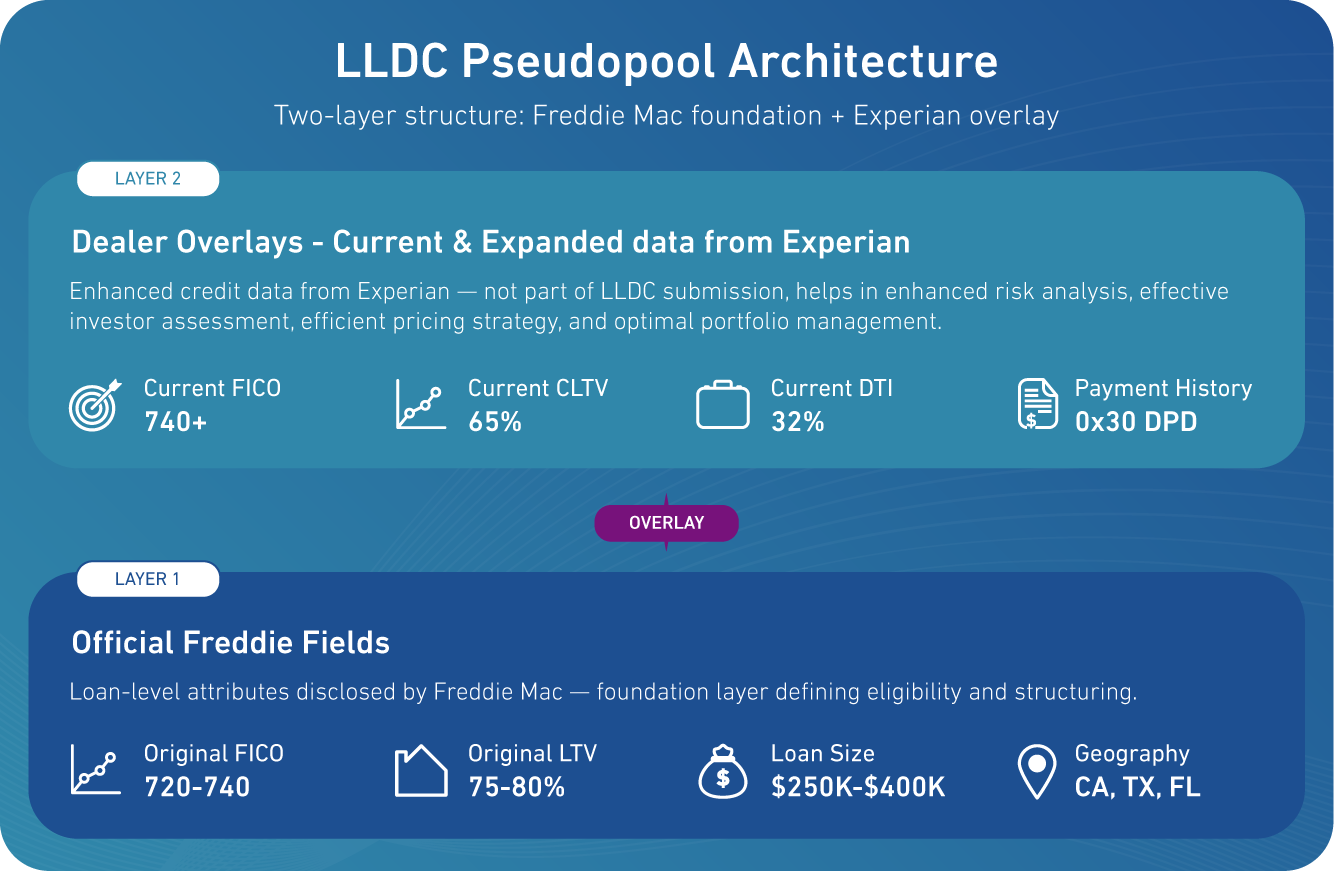

Freddie Mac’s November 2025 launch of Loan-Level Directed Collateral (LLDC) capabilities (details here) marks a significant advancement in mortgage-backed securities (MBS) capital markets. Historically, investors have been constrained by security-level pooling constructs that limit the expression of differentiated loan-level analytics. By allowing loan-level customization of Freddie pools & REMIC classes, LLDC empowers institutional investors to construct pools which reflect differentiated analytics—creating a competitive edge while simultaneously enhancing market-wide efficiency.

A historical lens: Evolution of MBS disclosure

The agency MBS market began its transformation in the 1980s with the release of pool-level data, enabling the rise of specified (“spec”) pools that traded on unique characteristics like origination loan size, credit score at origination, or geography. Specifications made the MBS market incrementally more efficient by allowing finer gradation of pricing for prepayment and credit risk.

The next leap came in 2013 with the public release of agency MBS loan-level data, which kicked off a new era of advanced analytics and precision modeling. The introduction of loan-level data further improved pricing efficiency by allowing the evaluation of layered risk (ie, credit score + LTV) at the loan level.

Unlike agency MBS markets, non-agency MBS disclosure remains fragmented. Hundreds of issuers lack a standardized data format. Third-party aggregators attempt to normalize disparate trustee and servicer data, but uniformity and quality still lags behind agency disclosures. The rise of 144a private placements over the past decade has reversed transparency progress—despite broader data availability and technological breakthroughs. The opacity of the growing 144a MBS market is particularly concerning and carries public policy implications, since market discipline for performance degradation is most efficiently meted out with greater transparency.

Despite AI-driven advances in data processing, disclosure remains stuck in an analog past. Borrower and property data remain static snapshots at origination, rarely updated. As a result, market participants operate with stale inputs, undermining the accuracy of risk assessments and pricing.

The Data Gap: What’s Missing in Current MBS Datasets

Across the MBS landscape, investors lack visibility into:

- Borrowers’ current credit health (beyond loan pay status)

- Borrowers’ current income and DTI

- Updated property valuations and lien statuses

- Behavioral trends like refinance propensity, ie, how many mortgages has this borrower refinanced in the past?

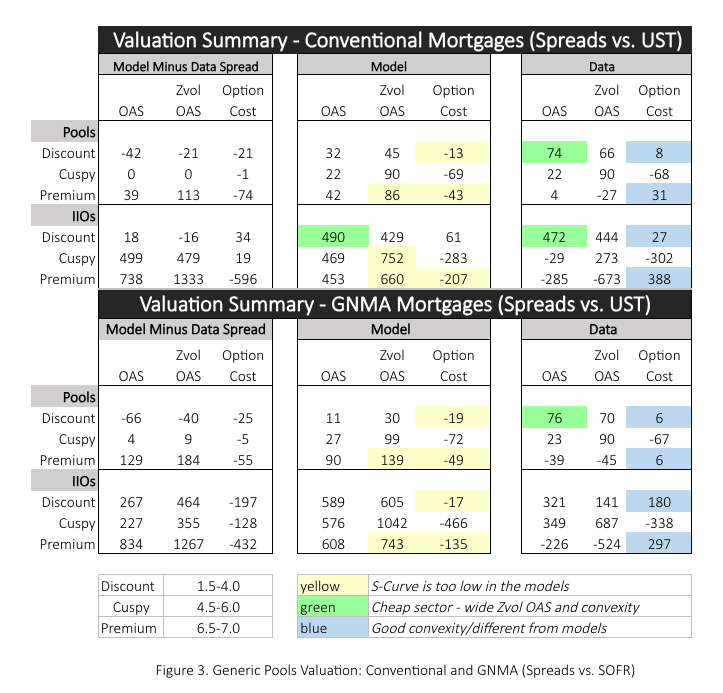

Even state-of-the-art prepayment and pricing models frequently diverge from empirical performance. As shown in the table below, models often misalign with actual data from agency pools and inverse IO CMOs (IIOs):

*Source: IVolatility MBS Data-Driven portal, and a prevalent Agency MBS valuation model

A Data Renaissance: Experian’s Mortgage Loan Performance Dataset (MLP)

To address these shortcomings, Experian created the Mortgage Loan Performance Dataset (MLP), a joined dataset capturing real-time borrower credit behavior, loan performance, and subject property data. MLP covers nearly 100% of U.S. mortgage loans dating back to 2005.

MLP Highlights:

- Current Credit Profile: Updated credit scores, credit inquiry activity (ie, is borrower shopping for a new mortgage?), non-mortgage debt balances and pay performance (student loan, auto loan, credit card, etc.)

- Current modeled income and DTI

- Behavioral History: Number of past refinances, payment habits (does this borrower pay off credit card balance in full each month?), utilization patterns

- Property Insights: Current AVM, current junior liens (including those opened after the loan was securitized), total CLTV

With this richer dataset, investors can:

- Improve credit and prepayment modeling accuracy

- Create new spec pool stories (e.g., serial refinancer, credit revolver utilization, current CLTV inclusive of subsequent second liens, credit inquiry activity)

- Overlay cohort-level data to bid more confidently on highly customized pools and REMICs structured under LLDC

Market Impacts: Efficiency and Equity

LLDC’s value lies in enabling more refined segmentation—particularly when enhanced with datasets like MLP. This facilitates better execution for originators and more precise pricing for investors. In turn, borrowers benefit from lower mortgage rates.

Importantly, MLP-driven segmentation could especially aid lower-income or weaker-credit borrowers. Currently, the less negatively-convex loans of these borrowers subsidize (from a pricing and rate perspective) the more negatively-convex loans of stronger credit, higher-income borrowers due to the averaging effect within generic pools. By identifying loans with better convexity (lower prepay likelihood), investors can price them more favorably, improving affordability in the form of lower mortgage rates for lower-income, weaker-credit borrowers.

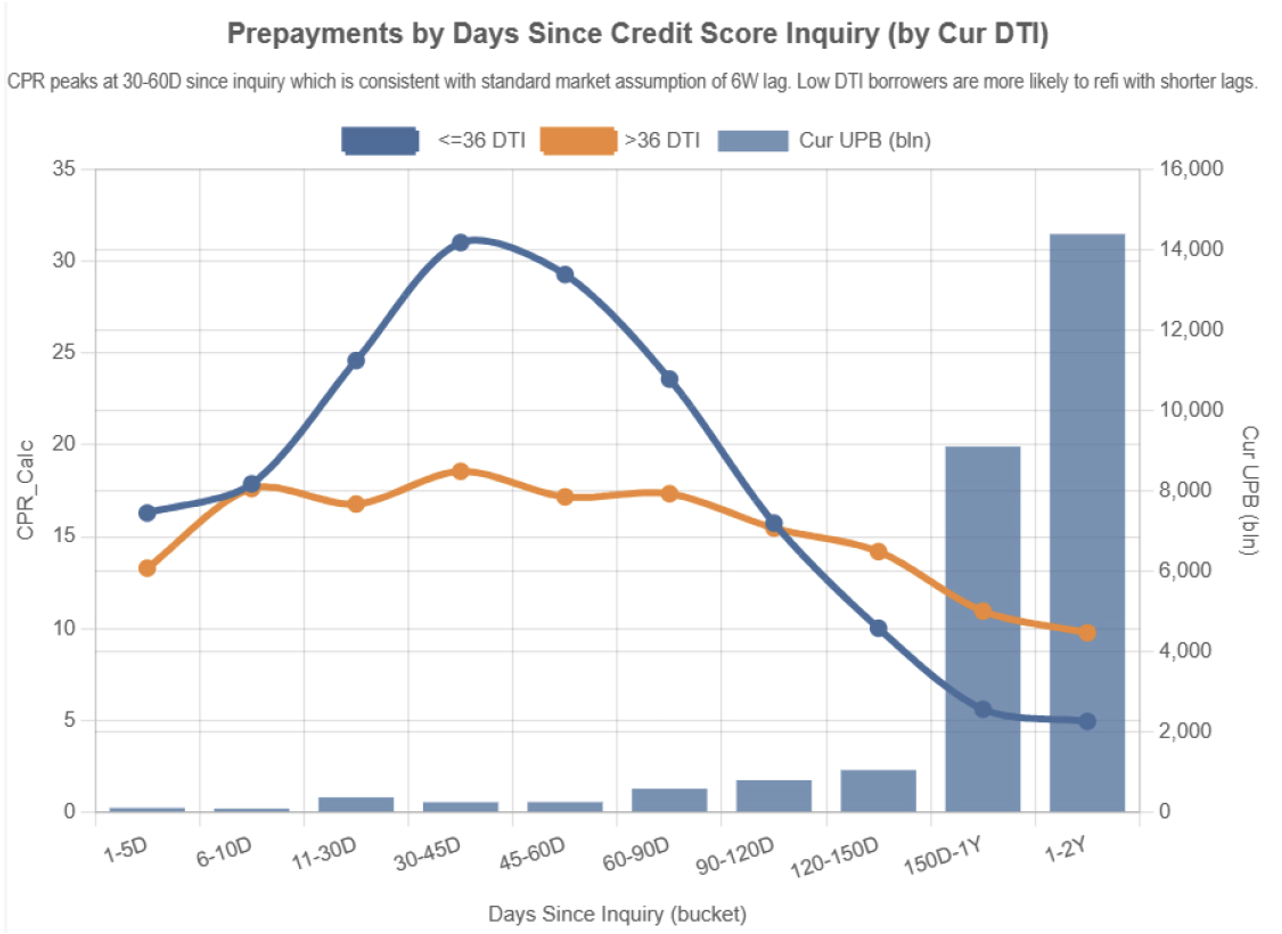

Case Study: Predicting Prepayment with Credit Inquiry Data

In the coming weeks, we’ll provide illustrative analyses that highlight new fields and scores available in the MLP dataset. To start, we’ll focus on perhaps the most intuitive datapoint for prepayment prediction: mortgage credit inquiry activity by the borrower. Specifically, credit inquiry activity is captured in a newly introduced field: Days Since Latest Mortgage Credit Inquiry.

Why It Matters:

- Traditional prepayment models rely on widely available market-level data (e.g., PMMS, HPI, MBA Index) and loan characteristics (loan size, fixed vs. ARM, margin, etc.)

- MLP offers new and scarce loan and borrower-level inputs, which provide additional forecasting power

Key Insight:

Borrowers with low current DTI (≤36%) are significantly more likely to refinance compared to those with high current DTI (>36%), and to do it faster after mortgage credit inquiry activity. Note that the current DTI is available in MLP, but not in most MBS disclosures.

*Source: Experian Mortgage Loan Performance Dataset, hosted on the IVolatility MBS Data-Driven Portal

This field is especially useful and practical for traders targeting specific mortgage cohorts (coupons, loan sizes, credit score range) for TBA roll trades, as an example.

Looking Ahead: A Richer Lens for MBS Analysis

This article is the first in a series exploring new data fields in the MLP dataset. Future installments will examine:

- Prior refinance behavior

- Total number of owned properties, credit card utilization, and payment behavior

Want to explore how MLP insights could improve your portfolio strategy?

Contact Experian to access the full MLP dataset and see your lift potential.

_____________________________________________________

Michael Pyatski advises MBS traders, portfolio managers, quants, risk managers, loan originators, and technology professionals on making informed, data-driven business decisions that drive revenue growth, enhance risk management, and reduce trading costs.

With more than 15 years of experience as an Agency RMBS trader—including serving as Head of the Proprietary Trading Desk at BNP Paribas—Michael developed and successfully implemented relative-value, data-driven profitable trading strategies to capture market opportunities embedded in data but not fully priced by the market. His trading experience, combined with a Ph.D. in econometrics, led him to found the Data-Driven Portal (https://datadrivenportal.com/), a platform that provides advanced technology for MBS trading and risk management.

The platform’s No-Model Data-Driven technology leverages big data, econometric analysis, and AI to help traders identify relative-value opportunities in RMBS markets and generate above-market, risk-adjusted returns.

_____________________________________________________