Industries

In our July edition of the State of the Economy report, we’ll be breaking down the data that financial institutions can use to navigate a recovery.

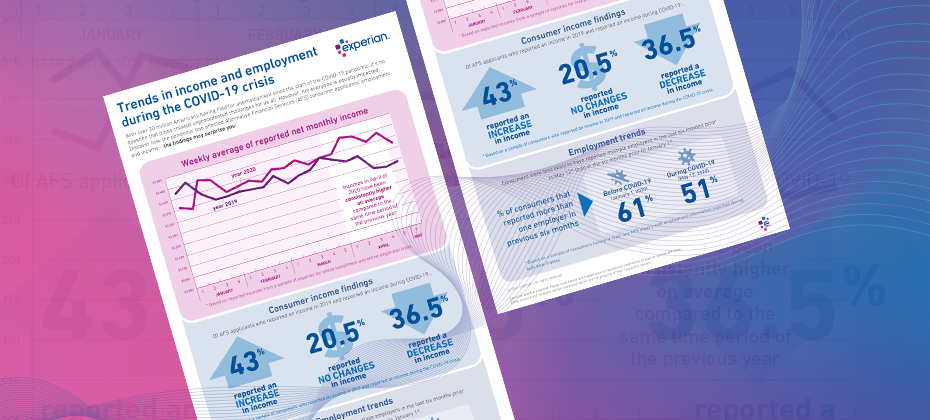

COVID-19 has had far-reaching economic consequences. When it comes to your consumers' finances, are you seeing the full picture?

Experian experts provide insight on how utility providers can evolve amidst COVID-19 and refine their collections and recovery processes.

To get a better picture of labor market health in the coming months, there are three components reported in BLS's employment release that require attention.

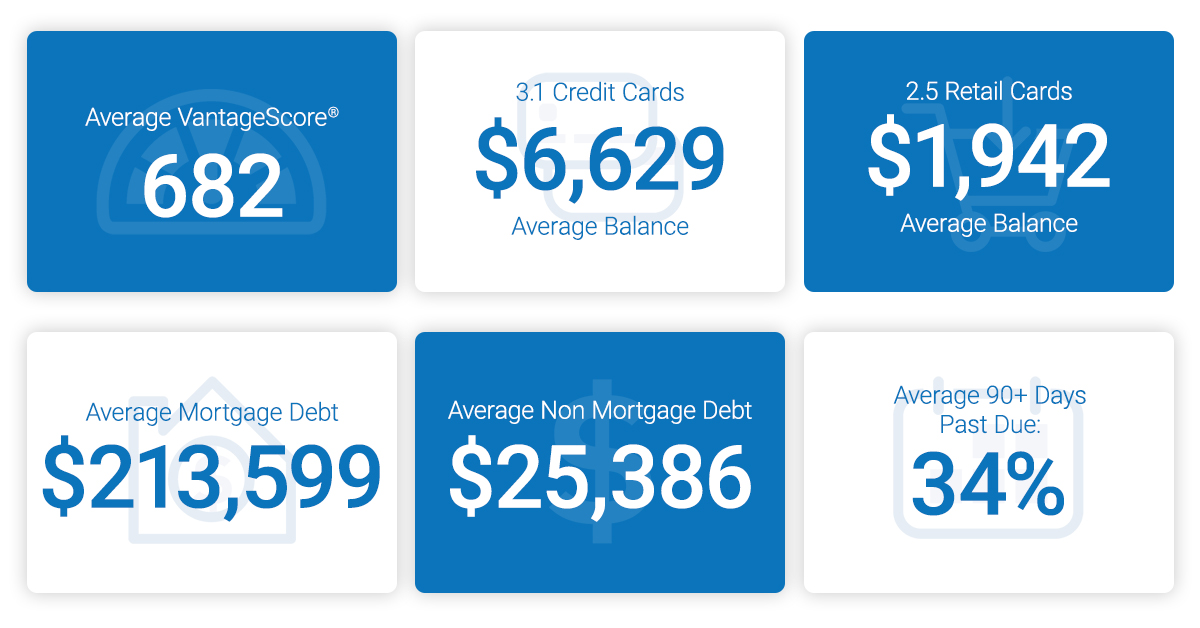

Download our case study to learn how home equity lender, Spring EQ, leveraged Experian Boost to help applicants qualify for better loan rates and terms.

Shannon Lois, Experian’s Head of DA Analytics and Consulting and Bryan Collins, Senior Product Manager, tackled questions for lenders amidst COVID-19.

Historically, economic hardships have directly impacted loan performance. Are you prepared to navigate and successfully respond to the current environment?

Learn the benefits of leveraging alternative credit data to better assess risk at the onset of the loan decisioning process. Read more.

At Experian, we are here to help consumers understand how the credit reporting system and personal finance overall will move forward during the pandemic.

According to Experian’s Q3 2019 State of the Automotive Finance Market report, used vehicle financing increased across all credit tiers.

According to research, only 15% of American consumers have swapped out their go-to credit card in the past year. Here's how to keep your card top of mind.

As look forward to the next decade, things are looking up. The 10th annual State of Credit Report highlights consumer credit scores and borrowing behavior.

Since the end of the recession, customer loyalty has been a focus for lenders, given that there are more options for AFS borrowers. Read more!

As we prepare for the excitement and challenges of a new decade, the same can be true for how we approach the use of alternative data. Read more!

What do Adam Sandler, Hugh Grant, Michael Bublé, Leo Tolstoy and Colonel Sanders have in common? They're all born on the most common birth date in the U.S.