All posts by Guest Contributor

The holidays can be a stressful time for consumers — and an important time for lenders to anticipate the aftermath of big credit card spending. According to our recent study with Edelman Intelligence: 56% of respondents said holiday shopping puts a strain on their finances. 43% said the stress of holiday shopping makes it difficult to enjoy the season. With the holiday shopping season over, those hefty credit card statements are coming soon. Now is the time for lenders to prepare for the January and February consolidations. Want to know more?

Using digital technology like a big bank How was your holiday? Are the chargebacks rolling in yet? It’s no secret - digital technology like mobile device usage has increased significantly over the years, making it a breeding ground for fraudsters. As credit unions continue to grow their membership, their fraud security treatments need to grow as well. Bigger banks are constantly updating their fraud tools and strategies to fight against cybercrime and, therefore, fraudsters are setting their eyes on credit unions. Even as I write this, fraudsters are searching and targeting credit unions that don’t have their mobile channel secured. They attempt to capitalize on any weakness or opportunity: Registering stolen cards to mobile wallets Taking over an account via mobile banking apps Using a retailers’ mobile app to make fraudulent payments Disabling the SIM card in the victim’s phone and diverting the one-time password sent through text message to their own phones These are clever ways to commit fraud. But credit unions are becoming wise to these new threats and are serious about protecting their members. They are incorporating device intelligence with a solid identity authentication service. This multi-layered approach is essential to securing mobile channels, and protecting your Credit Union from chargebacks. To learn more about our fraud solutions, click here.

As we kick off the new year, let’s take a look at some interesting things we learned about data quality in 2016. Our latest data quality report found some concerning statistics about companies and their data quality: 56% of organizations report losing sales opportunities due to bad data. 79% say data clearly ties directly to business objectives, but only 2% trust their data completely. 83% report that poor data quality impacts their business initiatives. Data is at the heart of your organization, and the quality of that data underpins the success of many of your business initiatives. Implementing a successful data quality program, therefore, is imperative to your organization’s future. Building a business case for data quality

Fraud and cybersecurity are two of the biggest risks challenging organizations and the economy today. Fraud has become its own industry, to the tune of $500 billion in estimated losses annually. To strengthen your fraud risk strategies, you need: A multilayered authentication and risk-based approach to prevent fraud. A comprehensive approach to identity with true customer intelligence. To avoid silos and recognize the value of combining your solutions into one platform. The rapid growth of fraud-related activity only reinforces the need for aggressive fraud prevention strategies and the adoption of new technology to prepare for the latest emerging cybersecurity threats. Want to know more?

Experian’s latest Market Trends and Loyalty report shows that for the first time in history, cars with four-cylinder engines have outpaced any other light-duty vehicle type on the road. That’s because the auto industry has been hard at work the past two decades improving both power and fuel efficiency of its engines. Auto manufacturers have been given aggressive fuel efficiency targets (54.5 mpg by 2025), but still need to meet consumer demand for performance. The net result is today’s average four-cylinder engine (188.1 hp) actually has more horsepower than the average V8 from 20 years ago (188 hp). It has helped four-cylinder engines become the most prominent engine type on the road, according to Experian Automotive Vehicles in Operation (VIO) database. Of the vehicles on the road, 37.7 percent are being powered by a four-cylinder engine, compared to 37.6 percent of six-cylinder engines. The top five vehicles at both the VIO and registration levels shows that all but one have four-cylinder engines. Top segments Total VIO Q3 vehicle registrations 1. Full-size pickup 1. Entry-level CUV 2. Standard midrange car 2. Full-size pickup 3. Small economy car 3. Small economy car 4. Lower midrange car 4. Standard midrange car 5. Entry-level CUV 5. Lower midrange car The four-cylinder VIO market share growth will continue in the future. In 2016, for example, four-cylinder engines accounted for 54.2 percent of all engines in new vehicles sold. It is the fifth consecutive year that four-cylinder engines had more than 50 percent market share. Market share for six-cylinder engines has dropped from 32.5 percent in 2012 to 29.7 percent in 2016, while eight-cylinder engines have dropped from 16.1 percent to 12.1 percent.

As 2016 comes to a close, many in the financial services industry are trying to assess the impact the Trump administration and Republican controlled Congress will have on regulatory issues. Answers to these questions may be clearer after President-elect Trump is inaugurated on Jan. 20. However, those in the federal regulatory environment are already exploring oversight and regulation of the FinTech and marketplace lending sector. Warning on alternative credit risk models Inquiries by federal and state policymakers over the past year have centered on how FinTech and marketplace lenders are assessing credit risk. In particular, regulators have asked about how credit models different from traditional credit scoring models and what, if any, new attributes or data are being incorporated into credit risk models for consumers and small businesses. On Dec. 2, Federal Reserve Governor Lael Brainard signaled that policymakers continue to be interested in this area during a wide-ranging speech on the potential opportunities and risks associated with FinTech. In particular, Brainard warned that “While nontraditional data may have the potential to help evaluate consumers who lack credit histories, some data may raise consumer protection concerns” and that nontraditional data “… may not necessarily have a broadly agreed upon or empirically established nexus with creditworthiness and may be correlated with characteristics protected by fair lending laws.” Brainard also suggested that there are transparency concerns with alternative scoring models, saying that “alternative credit scoring methods present new challenges that could raise questions of fairness and transparency” given that consumers may not always understand what data is used utilized and how it impacts a consumer’s ability to access credit at an affordable price. Look for regulators and Congress to continue to focus on the fairness and accuracy of new credit risk models and the data underpinning those models in debates surrounding FinTech and Marketplace lending in 2017. A national charter for FinTech? Earlier this month, the Office of the Comptroller of the Currency (OCC) announced that it was considering the creation of a national charter for FinTech lenders. There has long been speculation that the OCC would offer a national charter for FinTech. Analysts have suggested that the creation of a charter could help increase regulatory oversight of the growing market and also provide additional regulatory certainty for the emerging FinTech industry. The OCC’s proposal would create a special purpose national bank charter for FinTech businesses that are engaged in at least one of three core banking activities: receiving deposits; paying checks; or lending money. The OCC will be developing a formal agency policy for evaluating special purpose bank charters for Fintech companies that will designate the specific criteria that companies applying for a charter will have to meet for approval. OCC has suggested that this will likely focus on safety and soundness; financial inclusion; consumer protection; and community reinvestment. The OCC is collecting comments on the proposed policy through Jan. 15, 2017.

At Experian, we’re proud to be the backbone of financial progress. We’re making sense of data and information in powerful new ways. For example, we are: Opening credit bureaus in developing countries, where access to credit was virtually non-existent. Finding new ways to help consumers better understand credit and how to impact their financial future. Protecting consumers from identity theft and businesses from fraud. Volunteering our time and expertise to improve the communities in which we live and work. We’re investing in the future, through new technologies, talented people and innovations – all of it to help create a better tomorrow. Want to know more?

Regardless of personal political affiliation or opinion, the presidential election is over, and the focus has shifted from debate to the impact the new administration will have on the regulatory landscape for banks. While many questions remain regarding the policy direction of a Trump administration, one thing is near certain: change is on the horizon. While on the campaign trail, Trump took aim at banking regulation: “Dodd-Frank has made it impossible for bankers to function. It makes it very hard for bankers to loan money…for people with businesses to create jobs. And that has to stop.” And in his first post-election interview, Trump outlined named financial industry deregulation to allow “banks to lend again” as a priority. Before Election Day, Experian surveyed members of the financial community about their thoughts on regulatory affairs. An overwhelming majority—85 percent—believed the election outcome would impact the current environment. Most surveyed are also feeling the weight of financial regulations established by the Obama administration in the wake of the severe financial crisis of 2008. Five out of six respondents feel current regulations have placed an undue burden on financial institutions. Three-quarters believe the regulations reduce the availability of credit. And less than half believe the regulations are positive for consumers. According to our survey, complying with Dodd-Frank and other regulations has a financial impact for most, with 76 percent realizing a significant increase in spend since 2008. Personnel and technology spend top the list, with an increase of 78 percent and 76 percent, respectively. Top regulations that require the most resources to ensure compliance: the Dodd-Frank Act (70 percent), Fair Lending Act (55), Bank Secrecy Act/Anti-Money Laundering (47) and Fair Credit Reporting Act (42). Specifically, the Dodd Frank and TILA-RESPA Integrated Disclosure were the two most frequently mentioned regulations requiring additional investment, followed by the Military Lending Act and Bank Secrecy Act/Anti-Money Laundering. What lies ahead? It’s difficult to determine how the Trump administration will tackle banking regulations and policy, but change is in the air.

Looking to score more consumers, but worried about increased risk? A recent VantageScore® LLC study found that consumers rendered “unscoreable” by commonly used credit scoring models are nearly identical in their financial and credit behavior to scoreable consumers. To get a more detailed financial portrait of the “expanded” population, credit files were supplemented with demographic and economic data. The study found: Consumers who scored above 620 using the VantageScore® credit score exhibited profiles of sufficient quality to justify mortgage loans on par with those of conventionally scoreable consumers. 3 to 2.5 million – a majority of the 3.4 million consumers categorized as potentially eligible for mortgages – demonstrated sufficient income to support a mortgage in their geographic areas. The findings demonstrate that the VantageScore® credit score is a scalable solution to expanding mortgage credit without relaxing credit standards should the FHFA and GSEs accept VantageScore® credit scores. Want to know more?

As we kick off the holiday shopping season, let’s look at the increasingly popular smart voice/artificial intelligent assistant. Here are some insights from a recent Experian survey on how consumers are using one such device: 9% use their Amazon Echo in the kitchen and 33.5% in the living room. Echo users are overwhelmingly satisfied with Alexa’s voice recognition interface — with 39% planning to use it more frequently. Top tasks asked of Alexa are set a timer, play a song, read the news, set an alarm, check the time and tell a joke. Devices that use voice and messaging can significantly increase the accessibilities and usability of applications for consumers. Do you have the right strategy in place to support these new technologies? >>View inforgraphic

It’s that time of year — for turkey. During Thanksgiving 2015, 736 million pounds of turkey were consumed in the United States. Hungry for more turkey data? The average weight of turkeys purchased for Thanksgiving is 16 pounds. An estimated 46 million turkeys were eaten on Thanksgiving, 22 million on Christmas and 19 million on Easter last year. More than 212 million turkeys were consumed in the United States in 2015. From all of us at Experian, we wish you a very happy Thanksgiving! Courtesy of the National Turkey Federation

The best way to increase email open rates? Include a subscriber’s name in the subject line. A recent Experian study found that in addition to higher open rates, personalized subject lines have a27% higher unique click rate, an 11% higher click-to-open rate and more than double the transaction rates of other promotional mailings from the same brands. Other proven personalization tactics include: Customizing subject lines based on browsing behavior Dynamically populating product choices based on the past purchases of the subscriber Triggering emails based on Instagram or Pinterest selections, connecting social media choices to email opportunities In addition to personalization, companies should coordinate social media programs with email and mobile campaigns in order to optimize engagement across all channels. >> Consumer credit trends

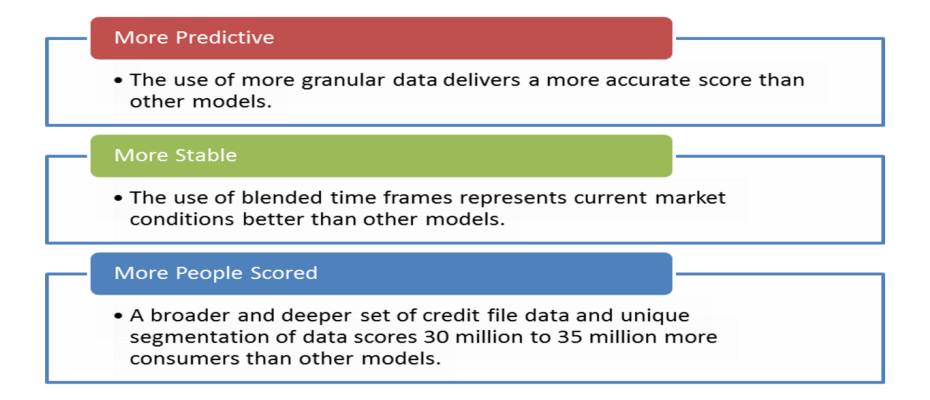

Lenders are looking for ways to accurately score more consumers and grow their applicant pool without increasing risk. And it looks like more and more are turning to the VantageScore® credit score to help achieve their goals. So, who’s using the VantageScore® credit score? 9 of the top 10 financial institutions. 18 of the top 25 credit card issuers. 21 of the top 25 credit unions. VantageScore leverages the collective experience of the industry’s leading experts on credit data, modeling and analytics to provide a more consistent and highly predictive credit score. >>Want to know more?

For members of the U.S. military, relocating often, returning home following a lengthy deployment and living with uncertainty isn’t easy. It can take an emotional and financial toll, and many are unprepared for their economic reality after they separate from the military. As we honor those who have served our country this Veterans Day, we are highlighting some of the special financial benefits and safeguards available to help veterans. Housing Help One of the best benefits offered to service members is the Veteran’s Administration (VA) home-loan program. Loan rates are competitive, and the VA guarantees up to 25 percent of the payment on the loan, making it one of the only ways available to buy a home with no down payment and no private mortgage insurance. Debt Relief Having a VA loan qualifies military members for a Military Debt Consolidation Loan (MDCL) that can help with overcoming financial difficulties. The MDCL is similar to a debt consolidation loan: take out one loan to pay off all unsecured debts, such as credit cards, medical bills and payday loans, and make a single payment to one lender. The advantage of a MDCL? Paying a lower interest rate and closing costs than civilians and far less interest than paying the same bills with credit cards. These refinancing loans can be spread out over 10, 15 and sometimes 30 years. Education Benefits The GI Bill is arguably the best benefit for veterans and members of the armed forces. It helps service members pay for higher education for themselves and their dependents, and is one of the top reasons people enlist. Eligible service members receive up to 36 months of education benefits, based on the type of training, length of service, college fund availability and whether he or she contributed to a buy-up program while on active duty. Benefits last up to 10 years, but the time limit may be extended. Saving & Investing Money According to the Department of Defense’s annual Demographics Report, 87 percent of military families contribute to a retirement account. Service members who participated in the Thrift Savings Plan, however, are often unaware of their options after they separate from service, and many don’t realize the advantages of rolling their plans into an IRA or retirement plan of a new employer. Safeguarding Identity Everyone is a potential identity theft target, but military personnel and veterans are particularly vulnerable. Routinely reviewing a credit report is one way to detect a breach. The Attorney General's Office provides general information about what steps to take to recover from identify theft or fraud. Today is a great time to consider ways to support your veteran and active military consumers. They are deserving of our support and recognition not just today but continuously. Learn more about services for veterans and active military to understand the varying protections, and how financial institutions can best support military credit consumers and their families.

Experian is recognized as a leading security solution provider for fraud and identity solutions in order to protect customers and financial institutions