Banking uncertainty creates opportunity for fraud

The recent regional bank collapses left anxious consumers scrambling to withdraw their funds or open new accounts at other institutions. Unfortunately, this situation has also created an opportunity for fraudsters to take advantage of the chaos. Criminals are exploiting the situation and posing as legitimate customers looking to flee their current bank to open new accounts elsewhere. Financial institutions looking to bring on these consumers as new clients must remain vigilant against fraudulent activity.

Fraudsters also prey on vulnerable individuals who may be financially stressed and uncertain about the future. This creates a breeding ground for scams as fear and uncertainty cloud judgment and make people more susceptible to manipulation.

Beware of fraudulent tactics

Now, it is more important than ever for financial institutions to be vigilant in their due diligence processes. As they navigate this period of financial turbulence, they must take extra precautions to ensure that new customers are who they say they are by verifying customer identities, conducting thorough background checks where necessary, and monitoring transactions for any signs of suspicious activity.

Consumers should also maintain vigilance — fraudulent schemes come in many forms, from phishing scams to fake investment opportunities promising unrealistic returns. To protect yourself against these risks, it is important to remain vigilant and take precautions such as verifying the legitimacy of any offers or investments before investing, monitoring your bank and credit card statements regularly for suspicious activity, and being skeptical of unsolicited phone calls, emails, or text messages.

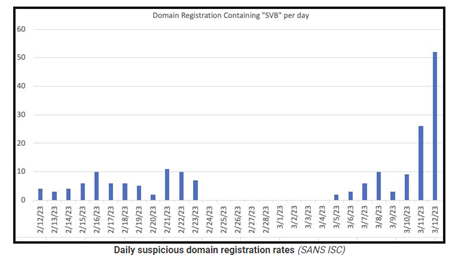

Security researcher Johannes Ulrich reported that threat actors are jumping at the opportunity, registering suspicious domains related to Silicon Valley Bank (SVB) that are likely to be used in attacks. Ulrich warned that the scammers might try to contact former clients of SVB to offer them a support package, legal services, loans, or other fake services relating to the bank’s collapse.

Meanwhile, on the day of the SVB closure, synthetic identity fraud began to climb from an attack rate of .57 to a first peak of 1.24% on the Sunday following the closure, or an increase of 80%. After the first spike reduced on March 14, we only saw a return of an even higher spike on March 21 to 1.35%, with bumps continuing since then.

As the economy slows and fraud rises, don’t let your guard down

The recent surge in third-party attack rates on small business and investment platforms is a cause for concern. There was a staggering nearly 500% increase in these attacks between March 7th and 11th, which coincided with the release of negative news about SVB.

Bad actors had evidently been preparing for this moment and were quick to exploit vulnerabilities they had identified across our financial system. They used sophisticated bots to create multiple accounts within minutes of the news dropping and stole identities to perpetrate fraudulent activities.

This underscores the need for increased vigilance and proactive measures to protect against cyber threats impacting financial institutions. Adopting stronger security measures like multi-factor authentication, real-time monitoring, and collaboration with law enforcement agencies for timely identification of attackers is of paramount importance to prevent similar fraud events in the future.

From frictionless to friction-right

As businesses seek to stabilize their operations in the face of market turbulence, they must also remain vigilant against the threat of fraud. Illicit activities can permeate a company’s ecosystem and disrupt its operations, potentially leading to financial losses and reputational damage.

Safeguarding against fraud is not a simple task. Striking a balance between ensuring a smooth customer experience and implementing effective fraud prevention measures can be a challenging endeavor. For financial institutions in particular, being too stringent in fraud prevention efforts may drive customers away, while being too lenient can expose them to additional fraud risks.

This is where a waterfall approach, such as that offered by Experian CrossCore®, can prove invaluable. By leveraging an array of fraud detection tools and technologies, businesses can tailor their fraud prevention strategies to suit the specific needs and journeys of different customer segments. This layered, customized approach can help protect businesses from fraud while ensuring a seamless customer experience.