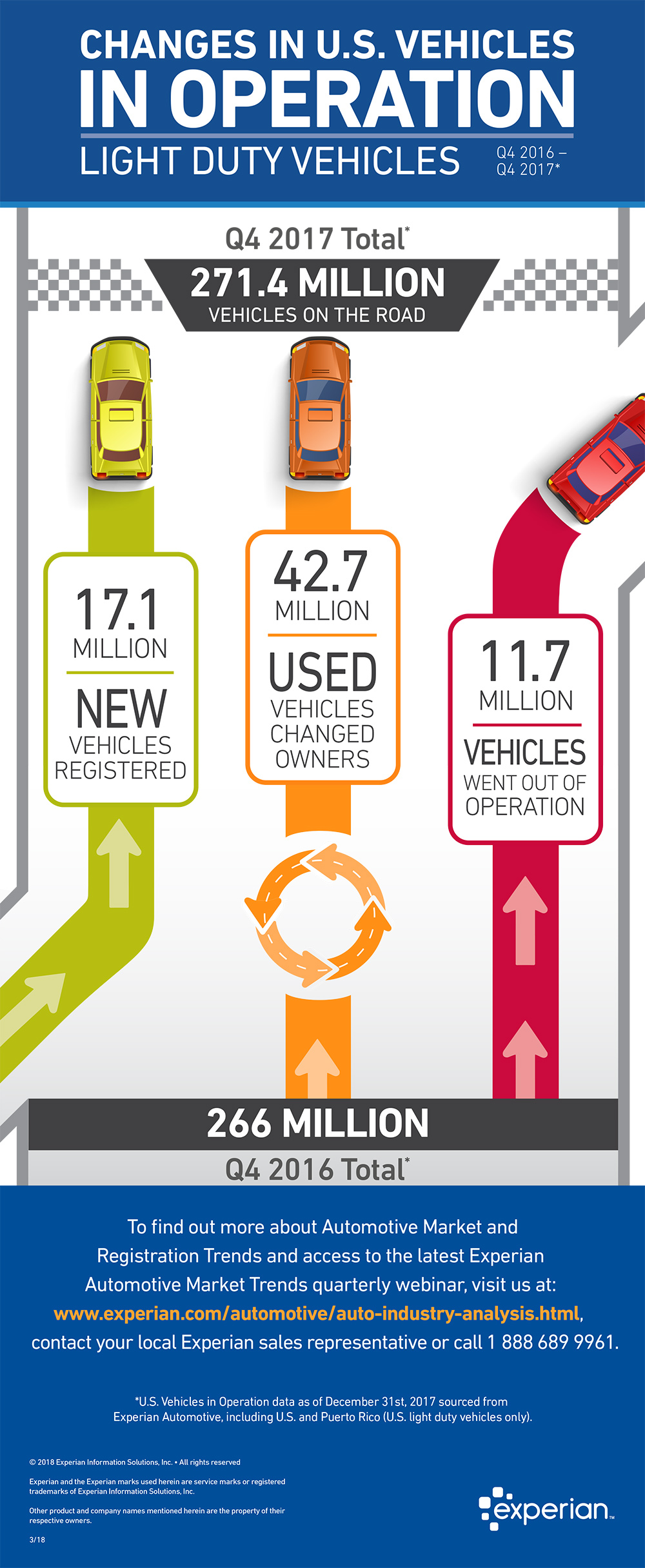

Changes in U.S. Vehicles in Operation: Q4 2016 – Q4 2017

Related Posts

Ian P. Moloney of the American Fintech Council discusses responsible fintech innovation and Experian’s role in expanding credit access.

For years, most electric vehicle (EV) adoption has been concentrated in California, New York, and other traditional early-adopter markets. And while those markets still lead the nation in total registrations, as of last year, some of the fastest-growing EV markets are in regions that haven’t played a significant role in the past. According to Experian Automotive’s 2025 EV Year in Review Report, EV adoptions seem to be entering a new phase that is spreading well beyond coastal strongholds. In fact, the top designated market areas (DMAs) that saw the fastest year-over-year growth for new retail individual EV registrations in the last five years were Detroit, MI (34.5%), Naples, FL (32.6%), Atlanta, GA (20.6%), Buffalo, NY (18.7%), and Charlotte, NC (17.3%). However, despite the growing demand in these market areas over the last few years, Los Angeles, CA still holds a strong lead in new retail individual EV registrations, with over 164,000 new adopters in 2025. Rounding out the top five were San Francisco, CA (85,000+), New York, NY (78,000+), Miami, FL (45,000+), and Seattle, WA (35,000+). EV adoption expanding well beyond the early-adopter markets could be a result of charging infrastructure growth, vehicle availability improvement, and consumer interest reaching new levels across the country. What does this mean for dealers? The extension of EV adoption into emerging markets signals that these vehicles are becoming a mainstream consideration for more consumers. As dealers look for ways to grow their presence in this segment, adopting marketing strategies, service operations, and inventory planning will be beneficial to meet changing buyer expectations and capitalize on the growing demand. The biggest takeaway isn’t necessarily which markets are selling the most EVs, it’s seemingly where adoption is gaining momentum. As new regions start to embrace these vehicles, it’ll be important to monitor the next phase of growth and where future opportunities may emerge. To learn more about EV insights, visit Experian Automotive’s EV Resource Center.

Learn how PREMIER Bankcard and Experian are helping expand financial access through data, technology and personalized decisioning.