Tag: income

A high-level review of risk-adjusted yields across three common retail products offered by credit unions show that credit cards can be very profitable.

New challenges created by the COVID-19 pandemic have made it imperative for utility providers to adapt strategies and processes that preserve positive customer relationships. At the same time, they must ensure proper individualized customer treatment by using industry-specific risk scores and modeled income options at the time of onboarding As part of our ongoing Q&A perspective series, Shawn Rife, Experian’s Director of Risk Scoring, sat down with us to discuss consumer trends and their potential impact on the onboarding process. Q: Several utility providers use credit scoring to identify which customers are required to pay a deposit. How does the credit scoring process work and do traditional credit scores differ from industry-specific scores? The goal for utility providers is to onboard as many consumers as possible without having to obtain security deposits. The use of traditional credit scoring can be key to maximizing consumer opportunities. To that end, credit can be used even for consumers with little or no past-payment history in order to prove their financial ability to take on utility payments. Q: How can the utilities industry use consumer income information to help identify consumers who are eligible for income assistance programs? Typically, income information is used to promote inclusion and maximize onboarding, rather than to decline/exclude consumers. A key use of income data within the utility space is to identify the eligibility for need-based financial aid programs and provide relief to the consumers who need it most. Q: Many utility providers stop the onboarding process and apply a larger deposit when they do not get a “hit” on a certain customer. Is there additional data available to score these “no hit” customers and turn a deposit into an approval? Yes, various additional data sources that can be leveraged to drive first or second chances that would otherwise be unattainable. These sources include, but are not limited to, alternative payment data, full-file public record information and other forms of consumer-permissioned payment data. Q: Have you noticed any employment trends due to the COVID-19 pandemic? How can those be applied at the time of onboarding? According to Experian’s latest State of the Economy Report, the U.S. labor market continues to have a slow recovery amidst the current COVID-19 crisis, with the unemployment rate at 7.9% in September. While the ongoing effects on unemployment are still unknown, there’s a good chance that several job/employment categories will be disproportionately affected long-term, which could have ramifications on employment rates and earnings. To that end, Experian has developed exclusive capabilities to help utility providers identify impacted consumers and target programs aimed at providing financial assistance. Ultimately, the usage of income and employment/unemployment data should increase in the future as it can be highly predictive of a consumer’s ability to pay For more insight on how to enhance your collection processes and capabilities, watch our Experian Symposium Series event on-demand. Watch now Learn more About our Experts: Shawn Rife, Director of Risk Scoring, Experian Consumer Information Services, North America Shawn manages Experian’s credit risk scoring models while empowering clients to maximize the scope and influence of their lending universe. He leads the implementation of alternative credit data within the lending environment, as well as key product implementation initiatives.

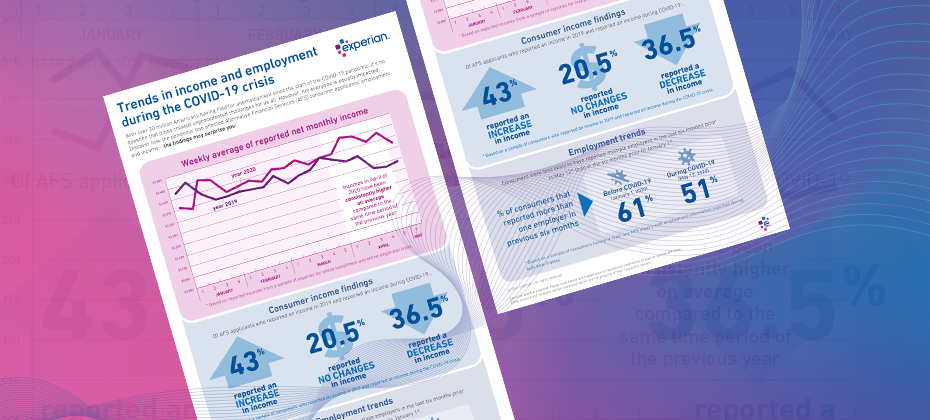

COVID-19 has had far-reaching economic consequences. When it comes to your consumers' finances, are you seeing the full picture?