Tag: digital identity

This post was updated in 2022. Fraud prevention can seem like a moving target. Criminals often shift from one scheme to the next, forcing organizations to play catch up to protect consumers’ identities and funds. But with the right technology, it’s possible to implement a fraud solution that provides protection and enhances the consumer journey. The pandemic fraud boom Government stimulus funds, COVID-19 testing and the loosening of business controls were a boon for criminals and levied an immense cost against businesses and consumers. Consumer fraud losses rose to $3.3 billion in 2020, up from $1.8 billion in 2019. The rapid increase in digital activity had two significant impacts. First, it shifted new account applications to the digital channel, where increased anonymity favors fraudsters by creating an environment where identity thieves could hide among the immense volume of applicants and monetize stolen personally identifiable information (PII). Second, it fueled account takeover (ATO) attacks by introducing digital “newbies” with unsophisticated password habits and limited ability to recognize and protect themselves from malware or social engineering, making them easy targets for credential theft. The return of old-school fraud Now that businesses and consumers are growing wise to some of the fraud schemes brought on by the COVID-19 pandemic, criminals are turning to new avenues, including tried-and-true methods like account opening and ATO fraud. New account fraud is expected to cost U.S. financial institutions $3.5 billion in 2021 alone. Fraud organizations will take the PII available and match it with automated tools to increase their efficiency and success rates while continuing with phishing and other schemes to gain new information that can fuel further attacks. Building a fraud solution Staying ahead of fraudsters may feel like a losing proposition but equipped with the proper fraud controls, you can enhance the customer experience, increase operational efficiency and protect against developing fraud schemes. With a fraud solution that uses multiple tools in concert, it’s possible to recognize, verify and holistically risk assess most consumers that pass through your portfolio. The right platform — ideally one that can call upon different services to perform each job — will enable your organization to flag suspicious activity, increase insight into large-scale attacks, track risky users and break down traditional internal silos. By coordinating efforts and adding multiple touchpoints to run both in the foreground and background, you can ensure the right friction is applied at the right time without diminishing the end-user experience. In fact, by improving your recognition tools, you can make the experience for recognized, legitimate customers even easier. To learn more about the potential impacts of traditional fraud and how your organization can leverage a fraud prevention solution to achieve your retention and growth goals, read our latest white paper or request a call. Read white paper Schedule a call

To drive profitable growth and customer retention in today’s highly competitive landscape, businesses must create long-term value for consumers, starting with their initial engagement. A successful onboarding experience would encourage 46% of consumers1 to increase their investments in a product or service. While many organizations have embraced digital transformation to meet evolving consumer demands, a truly exceptional onboarding experience requires a flexible, data-driven solution that ensures each step of customer acquisition in financial services is as quick, seamless, and cohesive as possible. Otherwise, financial institutions may risk losing potential customers to competitors that can offer a better experience. Here are some of the benefits of implementing a flexible, data-driven decisioning platform: Greater efficiency From processing a consumer’s application to verifying their identity, lenders have historically completed these tasks manually, which can add days, if not weeks, to the onboarding process. Not only does this negatively impact the customer experience, but it also takes resources away from other meaningful work. An agile decisioning platform can automate these tedious tasks and accelerate the customer onboarding process, leading to increased efficiency, improved productivity, and lower acquisition costs2. Reduced fraud and risk Onboarding customers quickly is just as important as ensuring fraudsters are stopped early in the process, especially with the rise of cybercrime. However, only 23% of consumers are very confident that companies are taking steps to secure them online. With a layered digital identity verification solution, financial institutions can validate and verify an applicant’s personal information in real time to identify legitimate customers, mitigate fraud, and pursue growth confidently. Increased acceptance rates Today’s consumers demand instant responses and easy experiences when engaging with businesses, and their expectations around onboarding are no different. Traditional processes that take longer and require heavy documentation, greater amounts of information, and continuous back and forth between parties often result in significant customer dropout. In fact, 40% of digital banking consumers3 abandon opening an account online due to lengthy applications. With a flexible solution powered by real-time data and cutting-edge technology, financial institutions can reduce this friction and drive credit decisions faster, leading to more approvals, improved profitability, and higher customer satisfaction. Having a proper customer onboarding strategy in place is crucial to achieving higher acceptance and retention rates. To learn about how Experian can help you optimize your customer acquisition strategy, visit us and be sure to check out our latest infographic. View infographic Visit us 1 The Manifest, Customer Onboarding Strategy: A Guide to Retain Customers, April 2021. 2 Deloitte, Inside magazine issue 16, 2017. 3 The Financial Brand, How Banks Can Increase Their New Loan Business 100%, 2021.

“Businesses are managing vast and growing amounts of consumer data – all while ensuring consumers’ privacy and complying with complex government regulations.” This is one of the many reasons there’s an increasing need for innovative digital identity solutions, as explored in a in Axios in a new Experian advertorial. Experian Identity, an integrated suite of identity solutions, products, and services, solves for challenges presented by the continuing migration of consumers to the internet and the resulting growth of consumer data. Leveraging that data stemming from diverse sources and combining it with advanced technologies, is critical to better determining and understanding a company’s best marketing prospects, as well as making confident decisions that enhance and safeguard the consumer experience. How? By leveraging multidimensional data and adhering to all consumer protection laws and industry self-regulatory standards, businesses can best recognize and connect with their consumers in more personalized, meaningful and secure ways. The Axios article discusses the benefits of Experian Identity, including strengthening fraud detection, solving for identity resolution, and helping to uncover business opportunities through segmenting, targeting and engaging consumers. “While today’s consumers are intensely interested in protecting their personal data and identities, they also want to be recognized and understood by the companies they do business with,” said Kathleen Peters, Chief Innovation Officer of Experian Decision Analytics, in the article. Read more about how Experian’s identity solutions helps businesses stay relevant with audiences, create a positive consumer experience, and meet people’s desire to be recognized in Axios’ new article. AXIOS: Making identities personal Learn more about Experian Identity

Experian recently announced Experian Identity and published an advertorial in American Banker outlining the integrated approach to identity that recognizes the full breadth of the company’s authoritative data solutions that help businesses better connect with their consumers in more personalized, meaningful and secure ways. The efforts address the rapidly changing definition and landscape of identity and take on the importance and needs for identity which span across the entire customer journey. From marketing to a specific consumer’s needs, to facilitating a friction-right customer experience, to protecting personal information. As such, there’s a gap for single-partner providers to help businesses navigate this change, while also putting the needs of the consumer first. “Identity data sets are constantly growing with inputs from new interactions. Many future sources of data have yet to be even conceived or developed,” said Kathleen Peters, Chief Innovation Officer, Experian Decision Analytics. “Staying ahead of the identity market curve is vital, and it requires building and continually evolving an enterprise-scale identity solution that interconnects with your own unique data and systems to create attribute-rich profiles of your customers that work across any identity application. That’s Experian Identity.” Experian Identity underscores the need businesses have to respond to increasing identity needs with interconnected, scalable technology, products and services that optimize the consumer experience. While the integrated approach announcement is new, the capability is not. Experian has been trusted for decades to secure individuals’ identity around the most important decisions in their lives – think purchasing a car or home, being identified at the doctor’s office, and more. As such, consumers remain at the center of every action. Experian Identity offers identity resolution, verification, authentication and protection, and fraud management solutions that include first- and third-party fraud, account takeover, credit card verification, identity resolution and restoration, risk-based authentication, synthetic identity protection and more. Additionally, we’ve included a special blog post introducing Experian’s identity capabilities from Kathleen Peters on the Experian Global News Blog and additional coverage. Stay tuned for more updates. Experian Global News Blog - Making Identities Personal: Experian Helps Businesses Build Consumer Trust American Banker – Making Identities Personal: Building Trust and Differentiating Your Brand Experian White Paper - Making Identities Personal For more information about Experian Identity, visit www.experian.com/identity-solutions.

“Disruption has caused enormous amounts of innovation,” said Jennifer Schulz, CEO of Experian, North America. “We must continue to be the disruptors in our industry which takes effort, data, technology, bright minds and vision for what the future will be.” Schulz kicked off the 39th Vision conference with a future-focused keynote delivered to a crowd of more than 400 attendees. Alex Lintner, Group President, Experian Consumer Information Services, talked about the next phase of great, highlighting the digital transformation that has taken place in the generations of the past and the disruption and innovation happening today and in the future. Keynote speaker: Dr. Mohamed A. El-Erian Dr. Mohamed A. El-Erian, renowned economist and author, President of Queens’ College, Cambridge, Chief Economic Advisor at Allianz, Chair of President Obama’s Global Development Council and Former CEO and Co-Chief Investment Officer of PIMCO, spoke about the Fed, inflation, negative interest rates and the labor market, as well as the importance of inclusion. El-Erian, who said he reads the Financial Times religiously, acknowledged that we will make mistakes on the journey as we work to be even more inclusive. To navigate what’s ahead, he said we will need resilience, optionality and agility. “It’s important to connect with information, acknowledge the insecurity, in a language people understand, in order to connect,” he said. Session highlights – day 1 The conference hall was buzzing with conversations, discussions and thought leadership. Buy Now Pay Later A large audience was in attendance for a session that introduced Experian’s Buy Now Pay Later Bureau™ and explored how it’s the first and only solution of its kind — serving consumers, BNPL providers, financial institutions and regulators. Identity Identity is constantly evolving, and while biometrics and authentication may have become ubiquitous, there is much activity around the concepts of eIDs, identity wallets and identity networks. Experian is making identities personal and helping businesses to recognize, manage and connect customer identities in new ways using data, analytics and technology. Marketing In today’s hypercompetitive world, businesses need to engage the freshest data and increase velocity when it comes to time to market. An average of 120 days won’t cut it. Ascend Marketing speeds time to market and helps achieve higher ROI. Regulatory Landscape With so much happening at Capitol Hill, a panel of experts from DC discussed a number of topics and proposals (and their impacts), including the defense for risk-based pricing, the impact of suppressing negative data, and trending topics like Buy Now Pay Later and data portability. All the while, the tech showcase had a constant flow of attendees with demos ranging from data and decisioning to financial inclusion and technology. This is just the beginning. And as Schulz said, “There’s more to do.” More insights from Vision to come. Follow @ExperianVision to see more of the action.

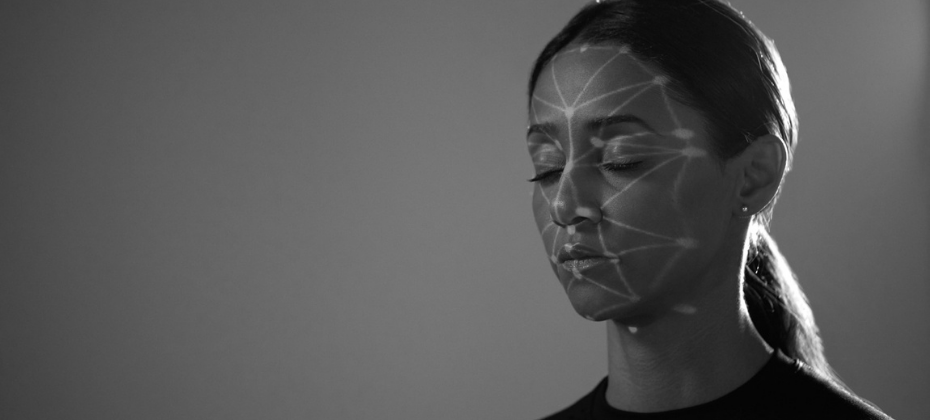

It’s time for organizations to harness the power artificial intelligence (AI) can bring to digital identity management – quickly and accurately identifying consumers throughout the lifecycle. The rise in crime The acceleration to digital platforms created a perfect storm of new opportunities for fraudsters. Synthetic identity fraud, stimulus-related fraud, and other types of cybercrime have seen huge upticks within the past year and a half. In fact, the Federal Trade Commission revealed that consumers reported over 360,000 complaints, resulting in more than $580 million in COVID-19-related fraud losses as of October 2021. To protect both themselves and consumers, businesses — especially lenders — will have to find and incorporate new strategies to identify customers, deter fraudsters and mitigate cybercrime. The benefits of AI for digital identity In our latest e-book, we explore the impacts of AI on organizations’ digital identity strategies, including: How changing consumer expectations increased the need for speed The challenges associated with both AI and digital identities The path forward for digital identity and AI How to develop the right strategy Building a solution It’s clear that current digital identity and fraud prevention tools are not enough to stop cybercriminals. To stay ahead of fraudsters and keep consumers happy, businesses need to look to new technologies — ones that can intake and compute large data sets in near-real time for better and faster decisions throughout the customer lifecycle. By using AI, businesses will enjoy a fast and consistent decisioning system that automatically routes questionable identities to additional authentication steps, allowing employees to focus on the riskiest cases and maximizing efficiency. Read our latest e-book to dive into the ways artificial intelligence and digital identity interact, and the benefits a clear identity strategy can have for the entire user journey. Download the e-book

Over the past year and a half, the development of digital identity has shifted the ways businesses interact with consumers. Companies across every industry have incorporated digital services, biometrics, and other verification tools to enhance the consumer experience without increasing risk. Changing consumer expectations A digital identity strategy is no longer a nice-to-have, it’s table stakes. Consumers expect to be recognized across platforms and have a seamless experience every time. 89% of consumers use mobile banking 80% of companies now have a customer recognition strategy in place 55% of banking customers say they plan to visit the bank branch less often moving forward Businesses are responding to these changing expectations while working to grow during the economic recovery – trying to balance consumer experience with risk appetite and bottom-line goals. The present state of digital identity Digital identity strategies require both standardization and interoperability. The first provides the ability to consistently capture data and characteristics that can be used to recognize a specific individual. The second allows businesses to resolve an identity to a specific person – recognizing a phone number, user ID and password, or a device – and use that information to determine if the user of the identity is in fact the identity owner. There are some roadblocks on the road to a seamless digital identity strategy. Issues include a lack of consumer trust and an ambiguous regulatory landscape – creating friction on both ends of the equation. Recipe for success To succeed, businesses need a framework that can reliably use different combinations of physical and digital identity data to determine that the person behind the identity is a known, verified, and unique individual. A one-size-fits-all solution doesn’t exist. However, a layered approach allows businesses to modernize identity, providing the services consumers want and expect while remaining agile in an ever-changing environment. In our newest white paper, developed in partnership with One World Identity, we explore the obstacles hindering digital identity management, and the best way to build a layered solution that is flexible, trustworthy, and inclusive. To learn more, download our “Capturing the Digital Evolution Through a Layered Approach” white paper. Download white paper

The surge in digital demand over the past year reinforced the deep connection between recognition, fraud prevention and the online customer experience. As businesses transformed their operations to accommodate the rapidly growing volume of digital transactions, consumer expectations for easy, secure interactions increased at an even faster pace. That meant less tolerance for the interruptions caused by security and risk controls. We surveyed more than 9,000 consumers and 2,700 businesses worldwide about this connection for our 2021 Global Identity and Fraud Report. This year’s report dives into: Business priorities for the year ahead Why the digital customer experience remains siloed Consumer preferences that impact the digital customer journey Pandemic-era digital activities that have changed consumer expectations As we move forward into the rest of 2021 it’s crucial that businesses continue to focus on fraud prevention. In order to implement an effective fraud strategy that also makes it easier for customers to engage, businesses need to move away from a one-size-fits-all approach and focus on applying the right level of protection to each and every transaction. Download the report Review your fraud strategy

The sharp uptick in fraud that coincided with the digital evolution made it clear that banks, credit unions, and fintechs need to invest in a strategy that utilizes identity layers to keep their customers and their finances safe. The steady rise in fraud over the last several years spiked—payment fraud rose 70% last year and is expected to increase by 95% in 2021—making it more challenging than ever to address the fraud threat while meeting increasing customer expectations. The rising fraud threat 2020 saw a rapid influx of customers using digital channels and the amount of data flowing into financial systems. There’s been a seismic shift, and we’re not going back. According to a recent study, 80% of consumers now prefer to manage their finances digitally, leaving the door open for fraudsters to take advantage of digital newbies. The increase in online activity corresponded with criminal activity. The rates of synthetic identity, account opening, and account takeover fraud have risen as fraudsters’ tactics have evolved. 80% of fraud losses now come from synthetic identities In 2020 the rate of new account credit card fraud attempts rose 48% Account takeover accounted for 54% of all fraud attacks in 2020 Fraudsters will continue to take advantage of current conditions, moving from stimulus-related fraud back to more traditional forms of financial theft, and financial institutions must adapt in turn with robust identity layers. Resolving the identity threat In our recent white paper, developed in partnership with One World Identity, we explore how businesses can address the fraud threat. It requires a multilayered identity proofing strategy for both onboarding and ongoing authentication. By doing this, financial institutions can gain a holistic view of consumers and their associated risks, decreasing friction while enabling robust fraud protection. To learn more, download our “Improving Fraud by Increasing Identity Layers” white paper. Download white paper

Update: After closely monitoring updates from the WHO, CDC, and other relevant sources related to COVID-19, we have decided to cancel our 2020 Vision Conference. If you had the chance to experience tomorrow, today, would you take it? What if it meant you could get a glimpse into the future technology and trends that would take your organization to the next level? If you’re looking for a competitive edge – this is it. For more than 38 years, Experian’s premier conference has connected business leaders to data-driven ideas and solutions, fueling them to target new markets, grow existing customer bases, improve response rates, reduce fraud and increase profits. What’s in it for you? Everything to gain and nothing to lose. Are you a marketer? These sessions were made to drive your conversion rates to new heights: Know your customers via omnichannel marketing: Your customers are everywhere, but can you reach them? Learn how to drive business-expansion strategy, brand affinity and customer engagement across multiple channels. Plus, gain insight into connecting with customers via one-to-one messaging. By invitation only, the future of ITA marketing: An evolving landscape means marketers face new challenges in effectively targeting consumers while staying compliant. In this session, we’ll explore how you can leverage fair lending-friendly marketing data for targeting, analysis and measurement. Want the latest in technology trends? Dive into discussions to transform your customer experience: Credit in the age of technology transformation: Machine learning and artificial intelligence are the current darlings of big data, but the platform that drives the success of any big data endeavor is crucial. This session will dive into what happens behind the curtain. Put away your plastic – next-generation identity: An industry panel of experts discusses the newest digital identity and authentication capabilities – those in use today and also exciting solutions on the horizon. How about for the self-proclaimed data geeks? Analyze these: Alternative data: Listen in on an in-depth conversation about creative and impactful examples of using emerging data assets, such as alternative and consumer-permissioned data, for improved consumer inclusion, risk assessment and verification services. The next wave in open data: Experian will share their views on the potential of advanced data and models and how they benefit the global value chain – from consumer scores to business opportunities – regardless of local regulations. And the risk masters? Join us as we kick fraud to the curb: Understanding and tackling synthetic ID fraud: Synthetic IDs present a serious challenge for our entire industry. This expert panel will explore the current landscape – what’s working and what’s not, the expected impact of the next generation SSA eCBSV service, and best practice prevention methods. You are your ID – the new reality of biometrics: Consumers are becoming increasingly comfortable with biometrics. Just as CLEAR has transformed how we use our biometric identity to move through airports, sports venues and more, financial transactions can also be made friction-free. The point is, there’s something for everyone at Vision 2020. It’s not just another conference. Trade in stuffy tradeshow halls and another tri-fold brochure for the insights and connections you need to take your career and organization to the next level. Like technology itself, Vision 2020 promises to connect us, unify us and enable us all to create a better tomorrow. Join us for unique networking opportunities, one-on-one conversations with subject-matter experts and more than 50 breakout sessions with the industry’s most sought-after thought leaders.

As the holiday shopping season kicks off, it’s prime time for fraudsters to prey on consumers who are racking up rewards points as they spend. Find out how fraud trends in loyalty and rewards programs can impact your business: Are you ready to prevent fraud this holiday season? Get started today

How can fintech companies ensure they’re one step ahead of fraudsters? Kathleen Peters discusses how fintechs can prepare for success in fraud prevention.

We live in a digital world where online identities are ubiquitous. But with the internet’s inherent anonymity, how do you know you’re interacting with a legitimate individual rather than an imposter? Too often we hear stories about consumers who see unauthorized purchases on their credit cards, enable access to their devices based on an imposter claiming to be a security vendor or send money to someone they met online only to learn they’ve been “catfished” by a fraudster. These are growing problems, as more consumers transition to digital services and look to businesses to protect them, enable seamless trusted interactions and maintain their privacy. I recently chatted with MarketWatch about how consumers can protect themselves and their privacy when using online dating apps, as well as what businesses are doing to safeguard digital data. As part of the discussion, I mentioned that a simple, standard verification process companies of all sizes can leverage is vital to our rapidly evolving digital economy. Today, companies have their own policies, processes and definitions of identity verification, depending on the services they offer. This ranges from secure access requiring strong identity proofing, document verification, multifactor authentication and biometric enrollment to new social profiles that do little more than validate receipt of an email to establish an online account. To satisfy those diverse risk-based needs, more organizations are turning to federated identity verification options. A federated system allows businesses to leverage trusted, reputable, third-party sources to validate identity by cross-referencing the information they’ve received from a consumer against these sources to determine whether to establish an account or allow a transaction. While some organizations have attempted to develop similar identity verification capabilities, many lack a trusted identity source. For example, there are solutions that leverage data from social media accounts or provide multifactor fraud and authentication options, but they often become easily compromised because of the absence of verifiable data. A trusted solution aggregates data across multiple providers that have undergone thorough security and data quality vetting to ensure the identity data is accurately submitted in accordance with business and compliance requirements. In fact, there are only a handful of trusted identity sources with this level of due diligence and oversight. At Experian, we assess verification requests against an aggregate of hundreds of millions of records that include identity relationships, profile risk attributes, historical usage records and demographic data assets. With decades of knowledge about identity management and fraud prevention, we help companies of all sizes balance risk mitigation and maintain compliance requirements — all while ensuring consumer data privacy. Trust takes years to build and mere seconds to lose, and the industry has made undeniable progress in security. But there is much left to do. Consumers are increasingly involved in the protection and use of their data. However, they often don’t realize downloading a hot new app and entering personal details or linking to their friends exposes them to unnecessary risk. It’s important for businesses to be clear about their identity verification processes so consumers can make educated decisions before electing to provide invaluable identity data. The most effective fraud prevention and identity strategy is one that quickly establishes trust without inconveniencing the consumer. By staying up to date on verification methods, businesses can ensure customers have a smooth, personalized and engaging online experience.

Reinventing Identity for the Digital Age Electronic Signature & Records Association (ESRA) conference I recently had the opportunity to speak at the Electronic Signature & Records Association (ESRA) conference in Washington D.C. I was part of a fantastic panel delving into the topic, ‘Reinventing Identity for the Digital Age.’ While certainly hard to do in just an hour, we gave it a go and the dialogue was engaging, healthy in debate, and a conversation that will continue on for years to come. The entirety of the discussion could be summarized as: An attempt to directionally define a digital identity today The future of ownership and potential monetization of trusted identities And the management of identities as they reside behind credentials or the foundations of block chain Again, big questions deserving of big answers. What I will suggest, however, is a definition of a digital identity to debate, embrace, or even deride. Digital identities, at a minimum, should now be considered as a triad of 1) verified personally identifiable information, 2) the collective set of devices through which that identity transacts, and 3) the transactional (monetary or non-monetary) history of that identity. Understanding all three components of an identity can allow institutions to engage with their customers with a more holistic view that will enable the establishment of omni-channel communications and accounts, trusted access credentials, and customer vs. account-level risk assessment and decisioning. In tandem with advances in credentialing and transactional authorization such as biometrics, block chain, and e-signatures, focus should also remain on what we at Experian consider the three pillars of identity relationship management: Identity proofing (verification that the person is who they claim to be at a specific point in time) Authentication (ongoing verification of a person’s identity) Identity management (ongoing monitoring of a person’s identity) As stronger credentialing facilitates more trust and open functionality in non-face-to-face transactions, more risk is inherently added to those credentials. Therefore, it becomes vital that a single snapshot approach to traditionally transaction-based authentication is replaced with a notion of identity relationship management that drives more contextual authentication. The context thus expands to triangulate previous identity proofing results, current transactional characteristics (risk and reward), and any updated risk attributes associated with the identity that can be gleaned. The bottom line is that identity risk changes over time. Some identities become more trustworthy … some become less so. Better credentials and more secure transactional rails improve our experiences as consumers and better protect our personal information. They cannot, however, replace the need to know what’s going on with the real person who owns those credentials or transacts on those rails. Consumers will continue to become more owners of their digital identity as they grant access to it across multiple applications. Institutions are already engaged in strategies to monetize trusted and shareable identities across markets. Realizing the dynamic nature of identity risk, and implementing methods to measure that risk over time, will better enable those two initiatives. Click here to read more about Identity Relationship Management.