Tag: customer retention

Delivering a superior customer experience has become the key goal for nearly every business across almost every industry. The banking industry is no exception. A recent trend highlighting the importance of customer experience is the drop in customer loyalty. Customer expectations are higher than ever, heightening competition between traditional banks and newer market entrants. This creates a need for banks to stand out and succeed by offering a superior customer experience. That experience starts with customer engagement in banking. According to a recent Forrester study, only two out of 10 retail banks regularly engage with customers to enhance their experience. The same study found that when retail banks consistently focus on improving the customer experience, they tend to grow more than three times faster than their competitors that do not. Forrester also found that over 70% of retail banks consider digital customer engagement essential for their current success and future growth.1 The key to customer engagement in banking: understanding the customer The good news for banks is that when they engage with customers by offering the services and guidance they want, those customers tend to respond with increased loyalty. Research indicates that 54% of customers rely on their banks to help them achieve their financial objectives. Most encouragingly, this same research indicates that 71% of actively engaged customers are likely to stay with their bank for the foreseeable future.2 At the heart of today’s evolving efforts to retain customers and build stronger loyalty are innovative tools that deliver on consumer demand for greater personalization and digital experiences in day-to-day engagement with the bank. With rising interest rates and more choices in financial services, consumers are actively seeking better rates for savings accounts, loans, and credit products. A 2024 Salesforce survey reveals that 72% of consumers are motivated to switch providers in search of better deals.3 Another report indicates that 50% of banking customers expect personalized offers for tools, products, and services to help them achieve their financial goals.4 In response to this trend, banks have an opportunity to go above and beyond to attract and retain customers by focusing on delivering exceptional customer service, innovative product offerings and personalized solutions to prevent customer churn. This requires embracing innovative approaches to engagement. For example, banks can leverage customer engagement services that empower customers to better manage their financial well-being. Such services might include smart tools that provide timely alerts and reminders, enabling customers to avoid delinquency and stay current with their payments. Strategies for enhancing engagement Banks aiming to enhance customer engagement can achieve this by utilizing data-driven insights, innovative technologies and customized partner solutions to foster loyalty and long-term trust. Customer engagement strategies should consider the following: Omnichannel experience – Banks aim to deliver a seamless, consistent experience across all touchpoints, whether it is a branch, mobile device, online platform, or contact center. Customers should be able to start an interaction on one channel and finish it on another without any friction. Connecting physical and digital touchpoints builds trust, convenience, and loyalty. Financial wellness tools and empowerment - Banks can utilize customer engagement services to provide customers with smart financial management tools, including budgeting dashboards, automated savings features, credit score monitoring, and investment advice. Providing customers with real-time insights into their financial health enhances engagement and fosters long-term loyalty. Identity protection and security tools – Banks can build trust through proactive identity protection, continuous monitoring and alerts that help customers feel protected and in control. Customer education and financial literacy – The bank can engage customers through educational content like webinars, tutorials, and in-app tips that help clarify financial products and promote better decision-making. Educated customers tend to be more confident, satisfied, and more likely to expand their relationship with the bank. Personalization through data and analytics – Banks can utilize data to deliver highly personalized recommendations, product offers, and experiences specific to individual life stages, behaviors, and goals. Predictive analytics can forecast needs, such as suggesting mortgage advice when spending and saving habits indicate a possible interest in homebuying, thus improving relevance and connection. It can also alert customers about savings opportunities. This kind of proactive engagement helps build stronger relationships. Customer engagement services: the key to driving revenue growth and enduring relationships At Experian®, we offer world-class customer engagement services that can enable banks to meet customer expectations and build stronger, long-lasting relationships. By providing tailored financial services and credit education, banks can help customers reach their financial goals. At the same time, banks can build stronger trust by empowering customers to avoid risks and take action to recover when identity theft occurs. All our solutions can be smoothly integrated into a bank’s existing ecosystem, making it quicker and easier to deliver these services to customers. As banks continue to seek ways to deliver exceptional customer experiences, it is essential to offer innovative tools and services that better engage customers. Customer engagement in banking is crucial for attracting and retaining clients. When banks go the extra mile to meet the evolving needs of customers, they are repaid with greater loyalty and long-term trust. Learn more about our customer engagement services Download the infographic 1https://www.kameleoon.com/blog/18-stats-understand-future-cx-optimization-and-banking2https://www.postgrid.com/customer-engagement-strategies-banking/3https://www.experian.com/content/dam/marketing/na/thought-leadership/business/documents/infographic-fostering-relationships-to-unlock-growth.pdf4https://www.experian.com/content/dam/marketing/na/thought-leadership/business/documents/infographic-fostering-relationships-to-unlock-growth.pdf

Building loyalty and improving customer retention are sensible business practices, and they're essential banking growth strategies for long-term success.

Customer retention is crucial for lenders to maximize lifetime value, especially during economic uncertainty. Increasing customer retention rates by just 5% can boost profits by 25% to 95%. However, many lenders struggle with loyalty, as seen in Q2 2024 when mortgage servicers’ retention rates for refinances dropped to 20%, the second lowest in 17 years. Nonbanks and banks also saw significant declines. This is due to increased competition, changing economic conditions, and a lack of personalization. Key strategies for improving customer retention Lenders can improve retention by leveraging data for personalization, maintaining consistent communication, offering loyalty rewards, and utilizing retention triggers. Leverage data for personalization. Use customer data to offer tailored products and refinancing options based on financial behaviors. Using credit attributes, trended data and alternative credit data (alternative financial services data, cashflow attributes, etc.) can help provide deeper insights of your customers. Maintain consistent communication. Keep customers informed with regular updates about interest rate changes or new loan products. Use a variety of communication channels, including email and in-app messaging, to ensure customers are kept in the loop. Ensure your customer service team is always available and responsive, offering clear answers to any financial concerns. Offer loyalty rewards. Develop programs that reward repeat business and referrals. Offer special rates or discounts for returning customers or for those who refer friends and family to your services. Increase customer lifetime value (LTV) by offering additional services like financial planning or credit score monitoring. Utilize retention triggers. Identify key events for engagement with automated retention triggers. For example, a borrower who has a mortgage with a fixed rate may be less likely to consider refinancing unless prompted. Experian’s Retention TriggersSM can notify lenders when refinancing might be beneficial to their customer, offering them personalized incentives or new product options at the right time. Why Experian’s Retention Triggers? By integrating Experian’s Retention Triggers, lenders can keep borrowers engaged, increase retention, and boost profitability even in tough economic times. Advanced data insights: Gain deeper insights into your customers’ behavior to identify those at risk of leaving and take proactive action. Personalized engagement: Automate personalized communications based on customer behaviors, ensuring timely engagement. Increased revenue: By offering personalized, timely and relevant offers, you can increase the likelihood of retaining your customers and growing your revenue. Make customer retention a priority In today’s challenging economic climate, lenders who focus on personalized experiences, consistent communication, and relevant offers will stand out and retain borrowers. Leverage tools like Experian’s Retention Triggers to proactively engage customers, reduce churn, and foster long-term relationships for increased profitability and success. Learn more

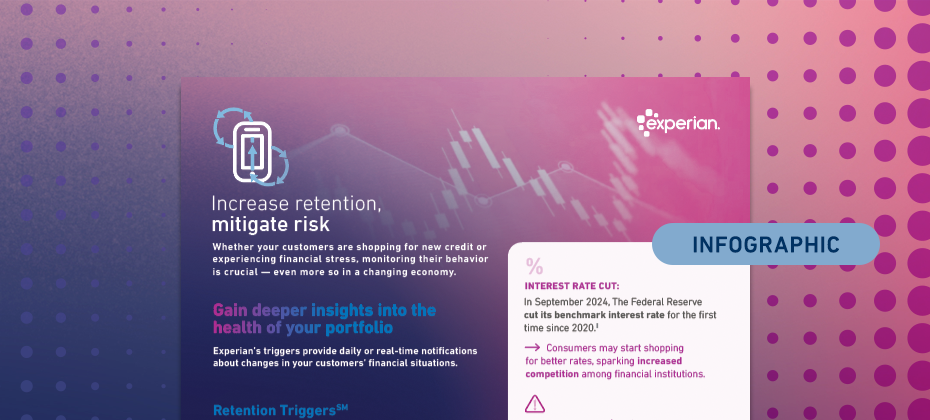

Whether consumers are shopping for new credit or experiencing financial stress, monitoring their behavior is crucial — even more so in an ever-changing economy. Our latest infographic explores economic trends impacting consumers’ financial behaviors and how Experian’s Risk and Retention TriggersSM enable lenders to detect early signs of risk or churn. Key highlights include: Credit card balances climbed to $1.17 trillion in Q3 2024. As prices of goods and services remain elevated, consumers may continue to experience financial stress, potentially leading to higher delinquency rates. Increasing customer retention rates by 5% can boost profits by 25% to 95%. View the infographic to learn how Risk and Retention Triggers can help you advance your portfolio management strategy. Access infographic

Do you know where your customers stand? Not literally, of course, but do you know how recent macroeconomic changes and their personal circumstances are currently affecting your portfolio? While refreshing your customers’ credit data quarterly works for some aspects of portfolio management, you need more frequent access to fresh data to quickly respond to risky customer behavior and new credit needs before your portfolio takes a hit. Use triggers to improve portfolio management Event-based credit triggers provide daily or real-time alerts about important changes in your customers’ financial situations. You can use these to manage risk by promptly responding to signs of changing creditworthiness or to prevent attrition by proactively reaching out to customers who are shopping for credit. Risk Triggers℠ and Retention Triggers℠ offer a real-time solution that can be customized to fit your needs for daily portfolio management. What are Risk Triggers? Experian’s Risk Triggers alert you of notable information, such as unfavorable utilization rate changes, delinquencies with other lenders and recent activity with high-interest, short-term loan products. This solution allows you to monitor how your customers manage accounts with other lenders to get ahead of potential risk on your book. You can use Risk Triggers to get daily insights into your customers’ activity — allowing you to quickly identify potentially risky behavior and take appropriate action to limit your exposure and losses. Types of Risk Triggers Choose from a defined Risk Triggers package that could help you identify high-risk customers, including: New trades Increasing credit utilization or balances over limit New collection accounts An account is charged-off A credit grantor closes an account New delinquency statuses (30 to 180 days past due) Consumers seeking access to short-term, high-risk financing options Bankruptcy and deceased events How to use Risk Triggers You can use the daily alerts from Risk Triggers to help inform your account management strategy. Depending on the circumstances, you might: Decrease credit limits Close or freeze accounts Accelerate payment requests Continue monitoring accounts for other signs of risk Spotlight on Experian’s Clarity Services events Included in Risk Triggers are events from Experian’s Clarity Services, which draw on expanded FCRA-regulated data* from a leading source of alternative financial credit data. For example, you could get an alert when someone has a new inquiry from non-traditional loans. These triggers provide a broader view of the customer – offering added protection against risky behavior. What are Retention Triggers? Experian’s Retention Triggers can alert you when a customer improves their creditworthiness, is shopping for new credit, opens a new tradeline or lists property. Proactively responding to these daily alerts can help you retain and strengthen relationships with your customers — which is often less expensive than acquiring new customers. Types of Retention Triggers Choose from over 100 Retention Triggers to bundle, including: New trades New inquiries Credit line increases Property listing statuses Improving delinquency status Past-due accounts are brought current or paid off How to use Retention Triggers You can use Retention Triggers to increase lifetime customer value by proactively responding to your customers’ needs and wants. You might: Increase credit limits Offer promotional financing, such as balance transfers Introduce perks or rewards to strengthen the relationship Append attributes for improved decisioning By appending credit attributes to Risk and Retention Trigger outputs, you can gain greater insight into your accounts. Premier AttributesSM is Experian's core set of 2,100-plus attributes. These can quickly summarize data from consumers' credit reports, allowing you to more easily segment accounts to make more strategic decisions across your portfolio. Trended 3DTM attributes can help you spot and understand patterns in a customer's behavior over time. Integrating trended attributes into a triggers program can help you identify risk and determine the next best action. Trended 3D includes more than 2,000 attributes and provides insights into industries such as bankcard, mortgage, student loans, personal loans, collections and much more. By working with both triggers and attributes, you'll proactively review an account, so you can then take the next best action to improve your portfolio's profits. Customize your trigger strategy When you partner with Experian, you can bundle and choose from hundreds of Risk and Retention Triggers to focus on risk, customer retention or both. Additionally, you can work with Experian’s experts to customize your trigger strategy to minimize costs and filter out repetitive or unneeded triggers: Use cool-off periods Set triggering thresholds Choose which triggers to monitor Establish hierarchies for which triggers to prioritize Create different strategies for segments of your portfolio Learn more about Risk and Retention Triggers. Learn more *Disclaimer: “Alternative Financial Credit Data” refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA-Regulated Data” may also apply in this instance, and both can be used interchangeably.

An intuitive digital customer experience in banking is more important than ever. Americans swipe, tap or insert their debit and credit cards at supermarkets, gas stations, restaurants, hotels and ATMs, conducting more than 74 million daily transactions.¹ Despite the volume of transactions, just 23% of banking customers give their bank high marks for its range of products, services and financial advice.² A hyper-digital, ever-changing banking industry means that there are more choices for financial service providers than ever before — and customers are taking full advantage of the options. On average, consumers have more than six different financial products and 82% of consumers between the ages of 18 and 24 acquired financial services products from new providers in the past 12 months.³ Digital transformation for banks is more crucial than ever, with some studies showing that 78% of bank customers prefer to access their accounts via a website or mobile app (with less than half of those surveyed ranking branch access as an important feature when shopping for a new checking account).4 Banks must embrace innovative strategies to elevate the banking customer experience in a competitive market. Here are some ways to boost customer retention and drive profitable growth. Rethink processes Complex processes and excessive paperwork needed to open accounts, approve credit cards and process loan applications can frustrate customers. In fact, more than 50% of consumers abandon the digital account opening process if it takes more than three to five minutes.5 Digital transformation initiatives can resolve these issues to improve the customer experience. Banks that leverage solutions, like artificial intelligence and automated data-driven decisioning solutions, to facilitate faster, more streamlined services can reduce friction, expedite processes and decrease wait times, resulting in improved customer satisfaction and retention. Reduce fragmentation Financial services are more fragmented than ever. Retail banking customers often use different providers for their checking and savings accounts, credit cards, investments, mortgages and other banking products. The options to access those accounts are also diverse, with customers choosing from brick-and-mortar branches, websites and mobile devices. Increased fragmentation means that the need to create an omnichannel experience should be top of mind for lenders. Additionally, the current retail banking landscape often fails to reward consumers for loyalty. Fewer than 15% of banks provide comprehensive rewards to those who use a single bank for multiple products or services, even though reducing fragmentation and taking a holistic approach to meeting customer needs can provide a competitive advantage.6 Personalize the digital experience While digital banking has reduced face-to-face interaction between banks and customers,7 consumers still expect a personalized banking experience. Experian has shown that using data analytics can lead to an improved understanding of customer needs and preferences, while customer segmentation enables the creation of targeted marketing campaigns, customized product offerings and tailored financial advice. These efforts towards a more personalized banking experience help increase customer satisfaction and loyalty. Provide more touchpoints An increasing number of branch closures and greater demand for digital banking services mean that just 3% of banking transactions are conducted in person.8 Customers are more willing to use digital channels for services like opening accounts and applying for loans. Banks can promote credit offers and product recommendations via email, social media and mobile banking applications while providing real-time digital customer experiences and prioritizing consistency across channels. Embracing a multichannel approach to marketing can help banks achieve better results, making it easier to cross-sell customers, amplify offers and meet consumer expectations for a personalized digital experience. Go beyond banking The customer experience in banking is about more than deposits, withdrawals and interest payments. Customers want resources and information to improve their financial well-being — and providing it can build trust, improve customer retention and boost revenue. Using digital channels to provide education might be more effective than encouraging appointments with customer service representatives. These tactics can help you: Leverage artificial intelligence to provide educational resources and personalized financial advice. Monitor user transactions for unusual activities and push information about online security or fraud protection. Employ chatbots to provide investment information and credit score monitoring and respond to questions about products ranging from mortgages to credit cards. Enhance your customer retention strategies by focusing on credit education and helping customers at every stage of their financial lives. Deliver a personalized customer experience in banking Globally, banks have invested $124 billion in artificial intelligence, machine learning and other technologies to make retail banking services more efficient and effective.9 Personalization is still imperative, and putting the customer first must remain the highest priority. Achieving those results requires a solid strategy for an improved banking customer experience. Experian leverages customer-level analytics and provides comprehensive solutions to expand digital transformation efforts, drive acquisition and improve customer retention. Learn more about our banking solutions. Learn more ¹Federal Reserve (2023). Commercial Automated Clearinghouse Transactions Processed by the Federal Reserve2,6-9Accenture (2023). Global Banking Customer Study3-4Forbes Advisor (2023). U.S. Consumer Banking Statistics5The Financial Brand (2023). How Credit Card Issuers Are Tackling Application Abandonment

Customer-driven marketing isn't just a buzzword — it's a strategic priority, especially in today's competitive digital landscape. Rather than pushing product-centric messaging, leading financial institutions (FIs) are shifting to strategies that put the customer at the core of every decision, message and experience. This means providing personalized experiences that enable customers to feel seen and heard. What is customer-driven marketing? Customer-driven marketing doesn't just improve visibility — it turns customers into brand advocates. It's a strategy that begins by understanding and prioritizing the needs, motivations and behaviors of customers, and then aligning every campaign, channel and touchpoint with those insights. This methodology focuses on relevance, personalization and responsiveness to customer signals. Why does customer-driven credit marketing matter? Today's consumers expect FIs to understand them beyond surface-level demographics. They demand tailored content, offers that match their needs and seamless interactions across channels. An effective customer-driven marketing strategy: Enhances personalization and relevance. By understanding consumer preferences, life stages and intent signals, FIs can move beyond generic messaging and create timely, relevant communications that resonate. The result is stronger engagement, higher response rates and more meaningful customer interactions. Boosts customer acquisition and retention. Customer-driven marketing enables FIs to identify and reach the most profitable, highly responsive prospects in the most efficient way, while also engaging with current customers to improve long-term retention. Improves campaign ROI and performance. By focusing marketing investments on the right audiences, customer-driven marketing ensures budgets are allocated strategically and impact is maximized. Enables stronger brand loyalty and trust. Customer-driven marketing fosters trust by respecting consumer preferences, delivering helpful content and creating seamless omnichannel experiences. Over time, this builds deeper brand loyalty, increases customer lifetime value and turns satisfied customers into advocates. Step-by-step: Developing the strategy Customer-driven marketing is less funnel, more spiral. You research, test, refine and repeat, all while taking into account customer feedback and campaign results. Start with deep audience understanding The foundation of effective customer-driven marketing lies in data-informed customer insights. Unlock a comprehensive view of your customers by combining first-party data with enriched analytics from trusted data partners. For example, Experian’s ConsumerView database lets marketers build audiences of more than 300 million U.S. consumers and 126 million households, supporting granular segmentation and personalization. Define and prioritize target segments Once your data foundation is in place, identify high-value segments based on behavior, purchase history, and life stage — not just basic demographics. This is where customer-driven marketing shines: instead of broad audience buckets, you target precise groups with tailored communications that feel 1:1. Deliver personalized experiences across channels Customers interact with brands in many ways — from email and social media to connected TV, search and in-store visits. A customer-driven marketing strategy ensures your brand message feels cohesive, relevant and timely across every touchpoint. Measure, learn and iterate A core part of customer-driven marketing is continuous improvement. Track how audiences respond to messaging and experiences — and refine your approach based on performance metrics. This “research, test, refine, repeat” mindset is essential for staying aligned with evolving customer expectations and maximizing ROI over time. Importance of a customer-driven marketing strategy Putting consumers at the center of credit marketing strategies — and at the center of your business as a whole — is the foundation for personalized experiences that can ultimately increase response rates and customer satisfaction. For more on how your organization can develop an effective customer-driven marketing strategy, learn about our credit marketing solutions. Learn more

"Out with the old and in with the new" is often used when talking about a fresh start or change we make in life, such as getting a new job, breaking bad habits or making room in our closets for a new wardrobe. But the saying doesn't exactly hold true in terms of business growth. While acquiring new customers is critical, increasing customer retention rates by just 5% can increase profits by up to 95%.1 So, what can your organization do to improve customer retention? Here are three quick tips: Stay informed Keeping up with your customers’ changing interests, behaviors and life events enables you to identify retention opportunities and create personalized credit marketing campaigns. Are they new homeowners? Or likely to purchase a vehicle within the next five months? With a comprehensive consumer database, like Experian’s ConsumerView®, you can gain granular insights into who your customers are, what they do and even what they will potentially do. To further stay informed, you can also leverage Retention TriggersSM, which alert you of your customers changing credit needs, including when they shop for new credit, open a new trade or list their property. This way, you can respond with immediate and relevant retention offers. Be more than a business – be human Gen Z's spending power is projected to reach $12 trillion by 2030, and with 67% looking for a trusted source of personal finance information,2 financial institutions have an opportunity to build lifetime loyalty now by serving as their trusted financial partners and advisors. To do this, you can offer credit education tools and programs that empower your Gen Z customers to make smarter financial decisions. By providing them with educational resources, your younger customers will learn how to strengthen their financial profiles while continuing to trust and lean on your organization for their credit needs. Think outside the mailbox While direct mail is still an effective way to reach consumers, forward-thinking lenders are now also meeting their customers online. To ensure you’re getting in front of your customers where they spend most of their time, consider leveraging digital channels, such as email or mobile applications, when presenting and re-presenting credit offers. This is important as companies with omnichannel customer engagement strategies retain on average 89% of their customers compared to 33% of retention rates for companies with weak omnichannel strategies. Importance of customer retention Rather than centering most of your growth initiatives around customer acquisition, your organization should focus on holding on to your most profitable customers. To learn more about how your organization can develop an effective customer retention strategy, explore our marketing solutions. Increase customer retention today 1How investing in cardholder retention drives portfolio growth, Visa. 2Experian survey, 2023.