Tag: consumer credit behavior

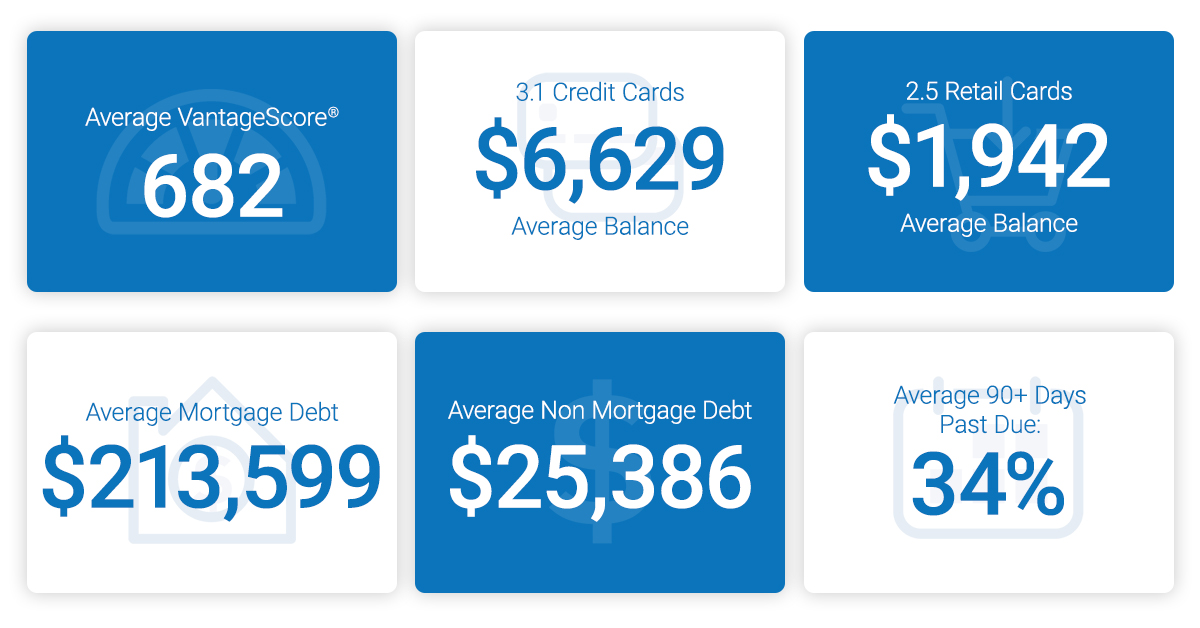

As consumers prepare for the next decade, we look at how we’re rounding out this year. The results? The average American credit score is 682, an eight-year high. Experian released the 10th annual state of credit report, which provides a comprehensive look at the credit performance of consumers across America by highlighting consumer credit scores and borrowing behaviors. And while the data is spliced to show men vs. women, as well as provides commentary at the state and generational level, the overarching trend is up. Even with the next anticipated economic correction often top of mind for financial institutions, businesses and consumers alike, 2019 was a year marked by more access, more spending and decreasing delinquencies. Things are looking up. “We are seeing a promising trend in terms of how Americans are managing their credit as we head into a new decade with average credit scores increasing two points since 2018 to 682 – the highest we’ve seen since 2011,” said Shannon Lois, Senior Vice President and Head of EAS, Analytics, Consulting & Operations for Experian Decision Analytics. “Average credit card balances and debt are up year over year, yet utilization rates remain consistent at 30 percent, indicating consumers are using credit as a financial tool and managing their debts responsibly.” Highlights of Experian’s State of Credit report: 3-year comparison 2017 2018 2019 Average number of credit cards 3.06 3.04 3.07 Average credit card balances $6,354 $6,506 $6,629 Average number of retail credit cards 2.48 2.59 2.51 Average retail credit card balances $1,841 $1,901 $1,942 Average VantageScore® credit score[1, 2] 675 680 682 Average revolving utilization 30% 30% 30% Average nonmortgage debt[3] $24,706 $25,104 $25,386 Average mortgage debt $201,811 $208,180 $231,599 Average 30 days past due delinquency rates 4.0% 3.9% 3.9% Average 60 days past due delinquency rates 1.9% 1.9% 1.9% Average 90+ days past due delinquency rates 7.3% 6.7% 6.8% In the scope of the credit score battle of the sexes, women have a four-point lead over men with an average credit score of 686 compared to 682. Their lead is a continued trend since 2017 where they’ve bested their male counterparts. According to the report, while men carry more non-mortgage and mortgage debt than women, women have more credit cards and retail cards (albeit they carry lower balances). Generationally, Generations X, Y and Z tend to carry more debt, including mortgage, non-mortgage, credit card and retail card, than older generations with higher delinquency and utilization rates. Segmented by state and gender, Minnesota had the highest credit scores for both men and women, while Mississippi was the state with the lowest average credit score for females and Louisiana was the lowest average credit score state for males. As we round out the decade and head full-force into 2020, we can reflect on the changes in the past year alone that are helping consumers improve their financial health. Just to name a few: Experian launched Experian BoostTM in March, allowing millions of consumers to add positive payment history directly to their credit file for an opportunity to instantly increase their credit score. Since then, there has been over 13 million points boosted across America. Experian LiftTM was launched in November, designed to help credit invisible and thin-file consumers gain access to fair and affordable credit. Long-standing commitments to consumer education, including the Ask Experian Blog and volunteer work by Experian’s Education Ambassadors, continue to offer assistance to the community and help consumers better understand their financial actions. From what we can tell, this is just the beginning. “Understanding the factors that influence their overall credit profile can help consumers improve and maintain their financial health,” said Rod Griffin, Experian’s director of consumer education and awareness. “Credit can be used as a financial tool. Through this report, we hope to provide insights that will help consumers make more informed decisions about credit use as we prepare to head into a new decade.” Learn more 1 VantageScore® is a registered trademark of VantageScore Solutions, LLC. 2 VantageScore® credit score range is 300 to 850. 3 Average debt for this study includes all credit cards, auto loans and personal loans/student loans.

Your consumers’ credit score plays an important role in how lenders and financial institutions measure their creditworthiness and risk. With a good credit score, which is generally defined as a score of 700 or above, they can quickly be approved for credit cards, qualify for a mortgage, and have easier access to loans with lower interest rates. In the spirit of Financial Literacy Month, we’ve rounded up what it takes for consumers to have a good credit score, in addition to some alternative considerations. Pay on Time Life gets busy and sometimes your consumers miss the “credit card payment due” note on their calendar squished between their work meetings and doctor’s appointment. However, payment history is one of the top factors in most credit scoring models and accounts for 35% of their credit score. As the primary objective of your consumers’ credit score is to illustrate to lenders just how likely they are to repay their debts, even one missed payment can be viewed negatively when reviewing their credit history. However, if there is a missed payment, consider checking their alternative financial services payments. They may have additional payment histories that will skew their creditworthiness more so than just their record according to traditional credit lines alone. Limit Credit Cards When your consumers apply for a new loan or credit card, lenders “pull” their credit report(s) to review their profile and weigh the risk of granting them credit or loan approval. The record of the access to their credit reports is known as a “hard” inquiry and has the potential to impact their credit score for up to 12 months. Plus, if they’re already having trouble using their card responsibly, taking on potential new revolving credit could impact their balance-to-limit ratio. For your customers that may be looking for new cards, Experian can estimate your consumers spend on all general-purpose credit and charge cards, so you can identify where there is additional wallet share and assign their credit lines based on actual spending need. Have a Lengthy Credit History The longer your consumers’ credit history, the more time they’ve spent successfully managing their credit obligations. When considering credit age, which makes up 21% of their credit score, credit scoring models evaluate the ages of your consumers’ oldest and newest accounts, along with the average age of all their accounts. Every time they open new credit cards or close an old account, the average age of their credit history is impacted. If your consumer’s score is being negatively affected by their credit history, consider adding information from alternative credit data sources for a more complete view. Manage Debt Wisely While some types of debt, such as a mortgage, can help build financial health, too much debt may lead to significant financial problems. By planning, budgeting, only borrowing when it makes sense, and setting themselves up for unexpected financial expenses, your consumers will be on the path to effective debt management. To get a better view of your consumers spending, consider Experian’s Trended3DTM, a trended attribute set that helps lenders unlock valuable insights hidden within their consumers’ credit scores. By using Trended3DTM data attributes, you’ll be able to see how much of your consumers’ credit line they typically utilize, whether they tend to revolve or transact, and if they are likely to transfer a balance. By adopting these habits and making smart financial decisions, your consumers will quickly realize that it’s never too late to rebuild their credit score. For example, they can potentially instantly improve their score with Experian Boost, an online tool that scans their bank account transactions to identify mobile phone and utility payments. The positive payments are then added to their Experian credit file and increase their FICO® Score in real time. Learn More About Experian Boost Learn More About Experian Trended 3DTM

Consumer credit scores A recent survey* released by the Consumer Federation of America and VantageScore Solutions, LLC, shows that potential borrowers are more likely to have obtained their credit score than nonborrowers. 70% of those intending to take out a consumer or mortgage loan in the next year received their credit score in the past year, compared with 57% of those not planning to borrow. Consumers who obtained at least one credit score in the past year were more likely to say their knowledge of scores is good or excellent compared with those who haven’t (68% versus 45%). While progress is being made, there’s still a lot of room for improvement. By educating consumers, lenders can strengthen consumer relationships and reduce loss rates. It’s a win-win for consumers and financial institutions. Credit education for your customers>

In 2017, a meaningful jump in consumer sentiment bolstered spending, and caused the spread between disposable personal income and consumer spending to reach an all-time high. This increase in spread was mostly financed through consumer debt, which according to the Federal Reserve Bank of New York has brought total consumer debt to a new peak of $12.8 Trillion surpassing the prior peak in 2008. The Experian eighth annual State of Credit report greatly supported the consumer behavior trends observed for the past year. Spanning the generations It is no surprise that generation Z (the “Great Recession Generation”) is conservative and prudent in their approach to credit because they are the most familiar with the post financial crisis economy. Results showed Millennials experienced a drop in overall debt, and an increase in mortgage debt reflects the national homeownership affordability challenge facing this generation. As first time homebuyers, millennials have to relatively tighten their spending as they dedicate an ever-growing portion of their income to housing. On the other end of the spectrum, the results of the study showed that Baby Boomers’ had sizable debt (including mortgage debt), which reflects the generation’s intent to stay active in their communities and in their homes much longer than prior generations have done. A recent Harvard study reported that by 2035, one out of three American households will be headed by an individual 65 years of age or older, compared to current ratio of one out of five households. What’s on the horizon? It is reasonable to assume that these trends may continue into 2018, as the underlying conditions continue to persist. A closer eye should be kept on student and auto loans due to the significant increase in portfolio size and increasing default rates compare to other debt. Editor’s note: This post was written by Fadel N. Lawandy, Director of the C. Larry Hoag Center for Real Estate and Finance and the Janes Financial Center at the George L. Argyros School of Business and Economics, Chapman University. Fadel joined the George L. Argyors School of Business and Economics, Chapman University after retiring as a Portfolio Manager from Morgan Stanly Smith Barney in 2009. He has two decades of experience in the financial industry with banking, credit management, commercial/residential real estate acquisition and financing, corporate finance, mergers and acquisitions, quantitative and qualitative analysis and research, and portfolio management. Fadel currently serves as the Chairman of the Board and President of CFA Society Orange County, and is an active member of the CFA Institute.

The economy is accelerating at a sluggish pace, and world headlines cause business leaders to swing between optimism and pessimism daily. Risk managers must look more closely and much more frequently at their customers' behavior to stay ahead of emerging credit problems. Some tips: Use all customer information when making decisions. Combining both internal and external data can paint a clearer picture of your customers. Identify the customer relationships that have value and should be retained. Apply resources accordingly. Implement daily triggers so you have the latest customer information around bankruptcy, repossession or loan delinquency, as well as positive information such as payments made to other financial institutions. Spend more time examining consumers who are delinquent on their home mortgage payments to determine their behavior on your portfolio. Use next-generation collections software to keep collectors up to date on account-level strategies. Download our white paper on how changes in the economy have impacted consumer credit behavior and what risk managers should analyze in order to determine portfolio strategies. Source: Experian News