Latest Posts

Panel discussion on Reinventing Identity for the Digital Age at Electronic Signature & Records Association (ESRA) conference

Under the updated requirements for Customer Due Diligence, financial institutions must expand programs.

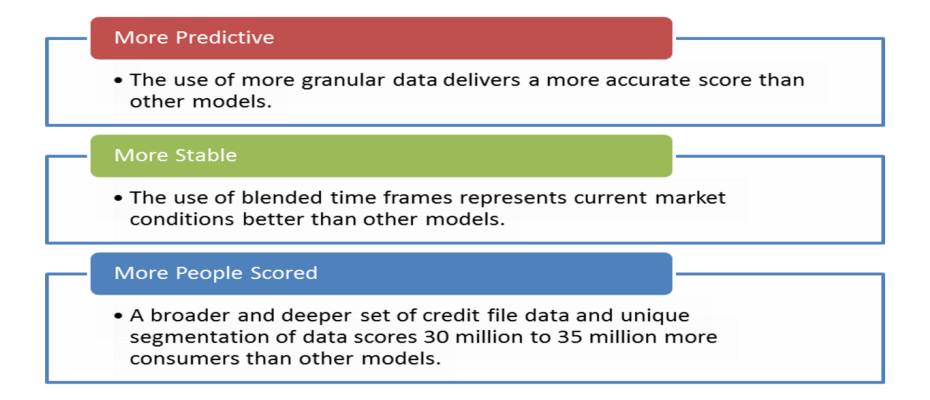

More lenders are turning to VantageScore® to help achieve their goals and reduce risk

For members of the U.S. military, relocating often, returning home following a lengthy deployment and living with uncertainty isn’t easy. It can take an emotional and financial toll, and many are unprepared for their economic reality after they separate from the military. As we honor those who have served our country this Veterans Day, we are highlighting some of the special financial benefits and safeguards available to help veterans. Housing Help One of the best benefits offered to service members is the Veteran’s Administration (VA) home-loan program. Loan rates are competitive, and the VA guarantees up to 25 percent of the payment on the loan, making it one of the only ways available to buy a home with no down payment and no private mortgage insurance. Debt Relief Having a VA loan qualifies military members for a Military Debt Consolidation Loan (MDCL) that can help with overcoming financial difficulties. The MDCL is similar to a debt consolidation loan: take out one loan to pay off all unsecured debts, such as credit cards, medical bills and payday loans, and make a single payment to one lender. The advantage of a MDCL? Paying a lower interest rate and closing costs than civilians and far less interest than paying the same bills with credit cards. These refinancing loans can be spread out over 10, 15 and sometimes 30 years. Education Benefits The GI Bill is arguably the best benefit for veterans and members of the armed forces. It helps service members pay for higher education for themselves and their dependents, and is one of the top reasons people enlist. Eligible service members receive up to 36 months of education benefits, based on the type of training, length of service, college fund availability and whether he or she contributed to a buy-up program while on active duty. Benefits last up to 10 years, but the time limit may be extended. Saving & Investing Money According to the Department of Defense’s annual Demographics Report, 87 percent of military families contribute to a retirement account. Service members who participated in the Thrift Savings Plan, however, are often unaware of their options after they separate from service, and many don’t realize the advantages of rolling their plans into an IRA or retirement plan of a new employer. Safeguarding Identity Everyone is a potential identity theft target, but military personnel and veterans are particularly vulnerable. Routinely reviewing a credit report is one way to detect a breach. The Attorney General's Office provides general information about what steps to take to recover from identify theft or fraud. Today is a great time to consider ways to support your veteran and active military consumers. They are deserving of our support and recognition not just today but continuously. Learn more about services for veterans and active military to understand the varying protections, and how financial institutions can best support military credit consumers and their families.

Experian is recognized as a leading security solution provider for fraud and identity solutions in order to protect customers and financial institutions

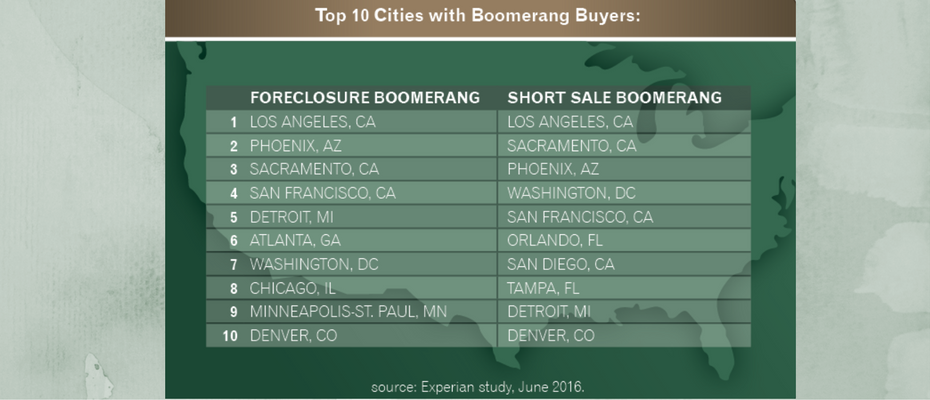

Experian analysis shows that 2.5M consumers will have a foreclosure, short sale or bankruptcy fall off their credit report between June 2016 and June 2017

The mortgage meltdown and Great Recession have translated into big shifts as it relates to financial services regulations. What's to come with a new administration coming soon?

The healthcare sector has been a hotbed of attacks due to the continued value of medical records sold on the dark web.

Experian announces partnership with U.S. Communities to help state and local public agencies prevent fraud, maximize revenue, strengthen security

$1.3 trillion. 41.1 million Americans. $31,590. These are the growing numbers associated with student loan debt in the United States: $1.3 trillion in outstanding student loans, spread across 41.1 million people, who are leaving college with an average balance of $31,590. The numbers are staggering, and for the first time student loan debt is playing a prominent role in a presidential election. For all of their differences, presidential nominees Hillary Clinton and Donald Trump seem to agree on one thing: student loan debt is a crushing burden. Both candidates have proposed solutions for student lending. Clinton’s “New College Compact” would allow borrowers to refinance their student loans at current rates available to students taking out new loans. She also wants to reduce interest rates on new student loans, and make it easier for borrowers to enroll in income-driven repayment programs that would cap monthly payments at 10 percent of discretionary income. Trump proposes giving more oversight to colleges to decide whether to grant loans to students based on their prospective major. The plan would also give private banks oversight over government-backed student loans—reversing a 2010 decision under President Obama to make the federal government the lender. Neither candidate, however, has outlined a solution for taming growing tuition costs. Tuition expenses are up 1,225 percent over the past 36 years, outpacing medical costs (634 percent rise) and the consumer price index (279 percent) over the same period, according to the Bureau of Labor Statistics. So it’s not surprising an Experian study shows the student loan rate has grown five percent in the past three years. What is surprising is the number of people and the average age of those people holding student loans. Experian found: 20 percent of people with a credit file hold a student loan that is being repaid or deferred. The average age of a consumer with a student loan is 37, with an average income of $47,200 compared to 53.8 and an average income is $44,500 for consumers without a student loan. The average age of a consumer with at least one deferred student loan is 32.7 with an average income of $32,900 compared to 38.7 and an average income of $53,200 for consumers with at least one non-deferred student loan. Candidate proposals aside, one thing is certain: student loan debt has a very real impact on the daily lives of people, many of whom have delayed buying homes, starting families, and saving for retirement. Until policymakers find a way to address bloated tuitions and student debt, it will take many longer to realize their dreams.

Reduce your TCPA compliance risk; Follow these steps when creating your dialing strategy

Businesses believe that 23% of their customer or prospect data is inaccurate.

Since 1948, International Credit Union Day – a time to recognize the credit union movement – has been celebrated the third Thursday of October. The day is the perfect time to remind your members and consumers about all of the services and benefits your credit union offers. This year’s theme, “The Authentic Difference,” celebrates what makes credit unions stand out. Here are 10 reasons CUs deserve a spotlight: Credit unions are non-profit cooperatives, owned and operated by its members. That means they emphasize consumer value to more than 217 million members worldwide. Profits go back to members in the form of reduced fees, higher savings rates and lower loan rates. Personal relationships are key. Credit unions pride themselves on developing relationships with their members, and CUs are typically staffed by friendly reps who know customers by name. Checking accounts are free. Roughly 80 percent of credit unions offer free checking accounts, compared to less than 50 percent of banks, according to economic research firm Moebs Services. Few ATM fees. Many credit union customers are able to avoid ATM fees because CUs typically give them access to a large network of ATMs by sharing branches and other resources. Savings rates are above average. Because credit unions don't have to pay dividends to shareholders and are exempt from federal taxes they can offer high rates on saving accounts. The average credit union offers CD, money market, and savings rates well above the national banking rates average. Lower interest rates. Credit unions offer lower interest rates on some loans. The difference between banks and credit unions was greatest in car-loan interest rates, according to a September report by SNL Financial. The average 36-month used-car loan interest rate offered by CUs was 2.67 percent compared to 4.45 percent for banks. For new-car loans, CUs offered an average interest rate for 48 months of 2.60 percent compared to 3.94 percent for banks. Invested in the community. A credit union’s core values are focused on its members and the communities where they live and work. Many provide financial education and outreach to consumers. It’s easier to get credit. CUs don’t have to abide by loan restrictions and qualifications mandated by a corporate office, so they have more flexibility to make loans when possible. Small-business support: CUs may know borrowers and are able to take into account intangibles like community reputation and accountability. Also, they understand the value to the community of a small business, its market and credit needs. Joining is easy. Many credit unions base eligibility simply on where you live, instead of restricting membership to a particular employer. Since expanding eligibility, credit union membership has grown by about two percent a year for the past decade.

Will they still aspire to achieve the “American Dream” of education, homeownership and raising a family? Are Millennials ready for a mortgage?

When financial planners and tax advisors meet with clients to review their portfolios, chances are they don't go over their credit reports often. Maybe they never do. Kiplinger’s estimates less than half of professional financial advisors take the time to review credit reports with clients. But taking this step is critical to understanding a person’s complete financial situation and creating a realistic plan. Prepare for Future Opportunities Clients may have all the credit they need at the moment, but if their credit score is mediocre or low, they might end up paying for it in the future. Just when they want to refinance a loan, buy more insurance, apply for a dream job or buy a business, they may discover their credit score is an obstacle. Check for Errors Credit bureaus collect billions of data points from millions of businesses each year, and it’s important to check a credit report for accuracy. If there are errors in a client’s file, he or she may be unfairly penalized. Keep in mind that nearly every company checks credit reports to determine who to do business with. Potential employers, business partners and insurance companies give credit files a look before deciding whether or not to make an offer to a person. Awareness Mistakes aren't the only factor leading to a low credit score. Too many hard inquiries, a maxed-out credit card or a number of small loans that could be paid off all cost credit points. Reviewing a credit report is a great way to help clients see the real impact their habits have on their financial life, and they could realize a significant rise in their credit score with little effort. Stand Out in the Crowd Even if a person has an exceptional credit report, a financial or tax advisor will gain credibility by reviewing their information with them. Doing so demonstrates out-of-the-box thinking and concern for a person’s financial health. Let's see a robo-advisor do this. Financial professionals can easily and securely review their clients’ credit reports online. Ready to understand your client’s complete financial situation? Try out our online solution at no cost to you. Interested in integrating with your existing financial or tax planning software? Learn more about integration options with Experian’s API.