Credit & Risk

More lenders are turning to VantageScore® to help achieve their goals and reduce risk

For members of the U.S. military, relocating often, returning home following a lengthy deployment and living with uncertainty isn’t easy. It can take an emotional and financial toll, and many are unprepared for their economic reality after they separate from the military. As we honor those who have served our country this Veterans Day, we are highlighting some of the special financial benefits and safeguards available to help veterans. Housing Help One of the best benefits offered to service members is the Veteran’s Administration (VA) home-loan program. Loan rates are competitive, and the VA guarantees up to 25 percent of the payment on the loan, making it one of the only ways available to buy a home with no down payment and no private mortgage insurance. Debt Relief Having a VA loan qualifies military members for a Military Debt Consolidation Loan (MDCL) that can help with overcoming financial difficulties. The MDCL is similar to a debt consolidation loan: take out one loan to pay off all unsecured debts, such as credit cards, medical bills and payday loans, and make a single payment to one lender. The advantage of a MDCL? Paying a lower interest rate and closing costs than civilians and far less interest than paying the same bills with credit cards. These refinancing loans can be spread out over 10, 15 and sometimes 30 years. Education Benefits The GI Bill is arguably the best benefit for veterans and members of the armed forces. It helps service members pay for higher education for themselves and their dependents, and is one of the top reasons people enlist. Eligible service members receive up to 36 months of education benefits, based on the type of training, length of service, college fund availability and whether he or she contributed to a buy-up program while on active duty. Benefits last up to 10 years, but the time limit may be extended. Saving & Investing Money According to the Department of Defense’s annual Demographics Report, 87 percent of military families contribute to a retirement account. Service members who participated in the Thrift Savings Plan, however, are often unaware of their options after they separate from service, and many don’t realize the advantages of rolling their plans into an IRA or retirement plan of a new employer. Safeguarding Identity Everyone is a potential identity theft target, but military personnel and veterans are particularly vulnerable. Routinely reviewing a credit report is one way to detect a breach. The Attorney General's Office provides general information about what steps to take to recover from identify theft or fraud. Today is a great time to consider ways to support your veteran and active military consumers. They are deserving of our support and recognition not just today but continuously. Learn more about services for veterans and active military to understand the varying protections, and how financial institutions can best support military credit consumers and their families.

Experian analysis shows that 2.5M consumers will have a foreclosure, short sale or bankruptcy fall off their credit report between June 2016 and June 2017

The mortgage meltdown and Great Recession have translated into big shifts as it relates to financial services regulations. What's to come with a new administration coming soon?

Experian announces partnership with U.S. Communities to help state and local public agencies prevent fraud, maximize revenue, strengthen security

$1.3 trillion. 41.1 million Americans. $31,590. These are the growing numbers associated with student loan debt in the United States: $1.3 trillion in outstanding student loans, spread across 41.1 million people, who are leaving college with an average balance of $31,590. The numbers are staggering, and for the first time student loan debt is playing a prominent role in a presidential election. For all of their differences, presidential nominees Hillary Clinton and Donald Trump seem to agree on one thing: student loan debt is a crushing burden. Both candidates have proposed solutions for student lending. Clinton’s “New College Compact” would allow borrowers to refinance their student loans at current rates available to students taking out new loans. She also wants to reduce interest rates on new student loans, and make it easier for borrowers to enroll in income-driven repayment programs that would cap monthly payments at 10 percent of discretionary income. Trump proposes giving more oversight to colleges to decide whether to grant loans to students based on their prospective major. The plan would also give private banks oversight over government-backed student loans—reversing a 2010 decision under President Obama to make the federal government the lender. Neither candidate, however, has outlined a solution for taming growing tuition costs. Tuition expenses are up 1,225 percent over the past 36 years, outpacing medical costs (634 percent rise) and the consumer price index (279 percent) over the same period, according to the Bureau of Labor Statistics. So it’s not surprising an Experian study shows the student loan rate has grown five percent in the past three years. What is surprising is the number of people and the average age of those people holding student loans. Experian found: 20 percent of people with a credit file hold a student loan that is being repaid or deferred. The average age of a consumer with a student loan is 37, with an average income of $47,200 compared to 53.8 and an average income is $44,500 for consumers without a student loan. The average age of a consumer with at least one deferred student loan is 32.7 with an average income of $32,900 compared to 38.7 and an average income of $53,200 for consumers with at least one non-deferred student loan. Candidate proposals aside, one thing is certain: student loan debt has a very real impact on the daily lives of people, many of whom have delayed buying homes, starting families, and saving for retirement. Until policymakers find a way to address bloated tuitions and student debt, it will take many longer to realize their dreams.

Will they still aspire to achieve the “American Dream” of education, homeownership and raising a family? Are Millennials ready for a mortgage?

In this new Telephone Consumer Protection Act (TCPA) era, calling your customers isn’t a thing of the past. It’s still okay to reach out to your clients by phone, whether to offer a new product or collect on an overdue bill. But strict compliance with TCPA rules is critical for any business that contacts customers by phone. Some of the very best ways you can protect yourself from TCPA exposure is to follow four steps when creating your dialing strategy: Customer consent: It’s important to maintain and update your customers’ contact preferences and consent to call them. Simply having a phone number on an application isn’t sufficient. Companies are required to have written permission, such as “I consent to calling my cell phone when there’s a problem …” Remember, permission may only be granted by the party who subscribes to the cellular service or who regularly uses that cell phone number. Landline or wireless?: Your database should also include the phone type for the telephone numbers you have for your customers. The dialing rules differ depending on the phone type, so it’s critical to know the type of phone you are calling or texting. Verify ownership: Ownership of cell phones should especially be validated to ensure the number hasn’t been reassigned and that the person who gave consent still owns the phone. One call can be made to a reassigned number with no liability, assuming you have no knowledge the number has changed. Repeating the action could lead to fines from $500 to $1,500 per infraction. Scrub Your Database: Have practices in place to remove any confirmed reassigned phone numbers from your database. This will help to improve your right-party contact rate and save you from potential TCPA headaches. No one disagrees that calling cell numbers is a risky business, but it can be done if you set the proper workflow in motion. Click here to learn more about Experian solutions that will help to reduce your TCPA compliance risk.

With the Oct. 3, 2016 compliance date upon us, many lenders continue to debate how they would like to solve for the Military Lending Act (MLA). With new enhancements, more protections have been granted to members of the military and their dependents when it comes to “consumer credit” products, specifically around the 36% cap on the MAPR. The key then becomes how to identify these individuals. At origination, how can the lender know if an individual is a member of the military, or a service member’s dependent? The answer, of course, lies in verification. Under the new Department of Defense (DOD) rule, lenders will have to check each credit applicant to confirm that they are not a service member, spouse, or the dependent of a service member. The final rule includes a “safe harbor” from liability for lenders who verify the MLA status of a consumer through a nationwide Credit Reporting Agency (CRA) or the DOD’s own database, known as the DMDC. Obviously, lenders will want to have this “safe harbor,” so the question becomes do you opt for the direct or indirect solution? The direct solution is to have the lender access the DMDC on their own. With this option, expected turnaround time is 24 hours for batch searches. The DMDC expects the volume of searches to their servers to increase from 220 million a week to 1.9 billion a week. For some, this feels like a more manual process, but it can be done. The indirect solution involves the CRA accessing the DMDC data on the lender’s behalf. In Experian’s case, this would translate into lenders seeing the MLA indicator on the credit report at point of origination or making a call out for just the MLA indicator. The process is integrated into the credit-pull cycle, so no manual effort is required on the lender’s end. MLA status is simply flagged. The rule also permits the consumer report to be obtained from a reseller that obtains such a report from a nationwide consumer reporting agency. Required data to perform a search includes full legal name, address, social security number and date of birth. This applies to both the credit report add-on and Experian’s standalone solutions. If any of this data is missing from the inquiry, Experian is unable to perform the MLA search. Credit card lenders have until Oct. 3, 2017 to adhere to the new standards, but all other applicable lenders must act now and build out their compliance standards and solutions. Direct or indirect? That is the question. To learn more about MLA or how Experian can help, visit our dedicated-MLA site.

Most businesses are familiar with credit bureaus today, but myths still exist around reporting credit data. Let's examine the top three and bust them.

The first six months of 2016 has shown that the total credit card limits among the subprime and deep subprime credit range totaled $6.4 billion, the highest amount reported for those groups in the last five years. Our Q2 2016 Experian-Oliver Wyman Market Intelligence Report webinar will analyze the trends impacting consumer credit decisions in the current economy. The data is from the latest Experian Market Intelligence Brief report.

With HELOC end of draw peaking, lenders must consider best practices and actions to take to manage and optimize their portfolios.

With a wave of HELOCs reaching the end-of-draw period, lenders are anxious to see how this will impact their portfolio. A new Experian study reveals likely consumer behaviors.

Bank executives don’t realize is they’re facing fraud because they’re literally inviting the fraudsters in bank branches.

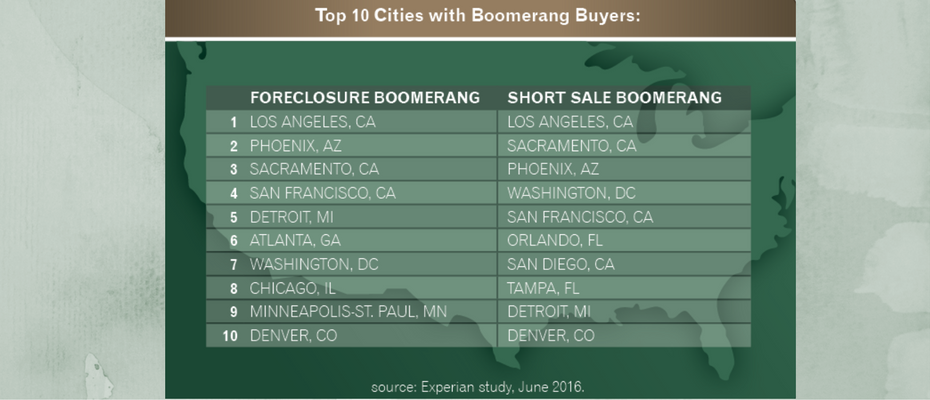

Time heals countless things, including credit scores. Many of the seven million people who saw their VantageScore® credit scores drop to sub-prime levels after suffering a foreclosure or short sale during the Great Recession have recovered and are back in the housing market. These Boomerang Buyers — people who foreclosed or short sold between 2007 and 2014 and have opened a new mortgage — will be an important segment of the real estate market in the coming years. According to Experian data, through June 2016 roughly 800,000 people had boomeranged, with Los Angeles, Phoenix, and Sacramento housing the most buyers. Some analysts believe more than three million Americans will become eligible for a home over the next three years. Are potential Boomerang Buyers a great opportunity to boost market share or a high risk for a portfolio? Early trends are positive. The majority of Boomerang Buyers who opened mortgages between 2011 and June 2016 are current on their debts. An Experian study revealed more than 29 percent of those who short sold have boomeranged, and just 1.5 percent are delinquent on their mortgage —falling below the national average of 2.8 percent. This group is also ahead of or even with the national average for delinquency on auto loans (1.2 percent vs. the national average of 2.2 percent), bankcards (3 percent vs. 4.3 percent) and retail (even at 2.7 percent). For those Boomerang Buyers who had foreclosed, the numbers are also strong. More than 12 percent have boomeranged, with just 3 percent delinquent on their mortgage. They also match or are below national average delinquency rates on auto loans (1.9 percent) and bankcards (4.1 percent), and have a slightly higher delinquency rate for retail (3.5 percent). Due to their positive credit behaviors, Boomerang Buyers also have higher VantageScore® credit scores than before. On average, the overall non-boomerang group’s credit score sunk during a foreclosure but went up 10 percent higher than before the foreclosure, and Boomerang Buyers rose by nearly 14 percent. For people who previously had a prime credit score, their number dropped by nearly 5 percent, while those who boomeranged returned to the score they had prior to the foreclosure. By comparison, the overall non-boomerang and boomerang group saw their credit score drop during a short sale and increase more than 11 percent from before the short sale. For people who previously had prime credit, they dropped 2 percent while those who boomeranged were almost flat to where they were before the short sale. Another part of the equation is the stabilized housing market and relatively low loan-to-value (LTV) limits that lenders have maintained. In the past, borrowers most often strategically defaulted on their mortgages when their LTV ratios were well over 100 percent. So as long as lenders maintain relatively low LTV limits and the housing market remains strong, strategic default is unlikely to re-emerge as a risk.