NA – North America

News about Experian North America:

During a year of the pivot, Experian North America remained focused on our purpose: Creating a Better Tomorrow. It’s not just a marketing tag line. It’s the lens through which we care for our employees, and how they in turn fuel innovations to serve our communities when they need help the most. That’s why this year’s 31 ranking in the Fortune "100 Best Companies to Work For" is so incredibly meaningful. For this year’s national award, two elements were considered: confidential employee feedback and the programs companies created to support people and communities in response to COVID-19. The employee surveys were distributed last summer, in the thick of pandemic restrictions and lockdowns. All around, we saw improvement: 50 percent of employees responded to the surveys (compared to 43 percent the year before), and 92 percent of employees attest that Experian is a Great Company to Work For (compared to 86 percent the year before). We’ve worked hard to build an employee culture over the past several years that continuously strives for inclusion and equity. This foundation became instrumental to how we navigated the past twelve months. Our employee resource groups took the lead to support our colleagues with the creation of a dynamic mental health and well-being guide, producing programs that brought awareness and support during social unrest and the rise in racism, and arranging annual celebrations to provide a touch of “normalcy.” Through a year that also included natural disasters such as the arctic blast, wildfires, storms and flooding, we have been there for each other. From free credit reports for consumers and small businesses, to products and services that enable governments, healthcare providers and nonprofits to prepare for and serve populations in crisis, Experian North America’s workforce leveraged diversity of perspectives, backgrounds and experiences to help vulnerable populations in crisis from COVID-19. Even through lockdowns and restrictions, employees logged 18,000 volunteer hours to increase financial inclusivity, support frontline healthcare workers, honor the nation’s military and veterans, and fight hunger. The Human Rights Campaign Foundation gave Experian North America a perfect score in its Corporate Equality Index for the third year in a row, and the company earned its recertification as a Great Place to Work. It has been named one of the top 10 Fortune’s Best Workplaces in Financial Services and Insurance, and a Comparably Top 50 company for Best Outlook 2021. Experian Costa Rica, part of our North America region, also earned Great Place to Work honors for the third year in a row. Our purpose runs deep. We put our people at the heart of how we run our business and it guides how we serve our consumers, clients and each other. We will continue this momentum of the 2021 Fortune 100 Best Companies to Work For by helping to drive financial inclusion and equity, growing our business through innovation, and creating opportunities for our coworkers to thrive and build meaningful careers.

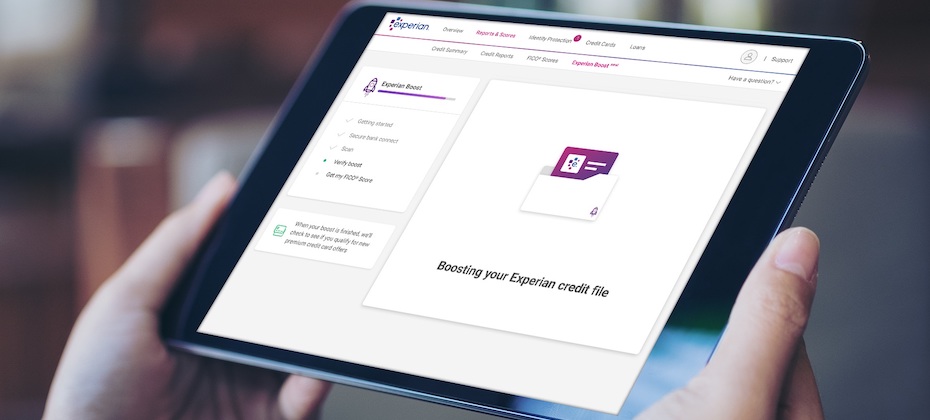

After launching Experian Boost, the first-of-its-kind tool that allows consumers to instantly increase their credit scores, in March 2019 we recently reached a significant milestone. Millions of consumers have boosted their credit scores to the tune of 50 million total points. This means many consumers have improved score bands, saved money with better interest rates, and maybe reached some of their financial goals such as gaining access to credit for a home. In fact, we know our Boost users have gained access to more than 1.7 billion total dollars in credit as a result of improving their credit score. The idea behind Experian Boost is to give consumers control over their credit – to enable them to make real, substantial progress in their financial health journey by getting “credit” for paying bills on time. Our ability to help consumers in a challenging economic climate is what drives us to continue to innovate. For example, we recently expanded Experian Boost to add positive payment history for video streaming services such as Netflix in addition to telecom and utility payments. The benefits to having control and using tools like Experian Boost do not end there. Consumers receive a boosted FICO® Score, which is used by a majority of lenders giving them a great opportunity for credit with better terms. In the first year after launching, we saw one million consumers add a credit card and nearly 250,000 consumers acquired an auto loan. Also, some consumers earned a credit score for the first time. What is also significant about Experian Boost is that this type of financial control and opportunity gives consumers a sense of empowerment, motivation and satisfaction that they can take a positive step in their financial journey. We’ve heard this firsthand from consumers through focus groups, and we even featured some consumers in our commercials who shared their positive experiences in front of the camera. This sentiment of empowerment among consumers is especially important right now as many are struggling financially due to the pandemic. We have many exciting new tools launching in 2021 and will continue to focus on empowering consumers to reach their financial goals. To learn more about Experian Boost, visit www.experian.com/boost.

Does checking my credit report hurt my credit score? How can I improve my credit score? What’s the difference between a credit score and a credit report? These are a few of the questions I most often hear about credit, and the answers to these fundamental questions are essential to financial well-being. Understanding credit scores and the factors that influence overall credit health is important any time, but this is especially true in our current environment. As part of our ongoing commitment to consumer education on the road to recovery, I recently had the pleasure of partnering with Akbar Gbajabiamila, host of American Ninja Warrior, former football pro and financial fitness expert, for an Instagram Live event. Akbar is passionate about helping people develop a financial game plan and he understands having a good credit history is a key component of good financial health. During the Instagram Live event, I answered questions from Akbar’s fans and shared ways to improve your credit score through tools like Experian Boost. In case you missed it, you can watch the video recap on Akbar’s Instagram account (@akbar_gbaja) or at the following link: https://www.instagram.com/tv/CLpbdDJlaQ6/ View this post on Instagram A post shared by 🇳🇬Akbar Gbajabiamila🇺🇸 (@akbar_gbaja) A positive credit history can be the gatekeeper to many of the things we all want in life, and we’re committed to helping facilitate fair and affordable access to credit for all consumers, including those in marginalized communities. This is one of the many reasons I’m passionate about my role at Experian. Educating consumers about credit is an important part of getting the economy as a whole humming again and helping those most in need. If you have additional questions about credit, feel free to check out the free resources below. Additional credit education resources and tools Join Experian’s weekly#CreditChat hosted by @Experian on Twitter with financial experts every Wednesday at 3 p.m. Eastern time. Visit the Ask Experian blog for answers to common questions, advice and education about credit. Add positive telecom, utility and streaming service payments to your Experian credit report for an opportunity to improve your credit scores by visiting experian.com/boost. You can request a free copy of your credit report from each of the three credit bureaus once a week through April 20, 2022 by visiting annualcreditreport.com For additional resources, visit https://www.experian.com/consumereducationor experian.com/coronavirus.

We recognize that COVID-19 has challenged Americans across the country, and nearly a year later, people are still struggling to recover. Among the more pressing issues for people has been navigating the financial landscape and hardships brought on by illness and high unemployment rates. At Experian, we empathize with consumers and are committed to helping them manage their financial lives. As part of this commitment, Experian, along with the other U.S. credit reporting agencies, is continuing to offer free weekly credit reports to all Americans for an additional year via AnnualCreditReport.com. At Experian, we view ourselves as the consumers’ bureau, and aim to help people better position themselves as they recover from COVID-related hardships. We’re proud of our ongoing efforts to assist consumers, particularly during these difficult times. Financial and credit information is constantly updated, and we believe providing consumers with increased access to their credit reports will help them improve their financial health, monitor for lender updates and ensure there is no fraudulent or unfamiliar activity on their credit profiles. We are committed to helping facilitate access to fair and affordable access to credit for all consumers. Our goal is not only to help consumers build credit, but also to effectively manage it. Beyond our continued offering of free credit reports, consumers can access resources and educational materials to help learn about credit and other important personal finance topics. In fact, we recently launched our United for Financial Health project to empower vulnerable populations to improve their financial health through education and action. We’re continually exploring new ways to use our data and resources to empower consumers and to improve their financial health and recover from COVID-19; extending access to free weekly credit reports is just another step in that process.

A year ago, we shifted our business to remote working as the global pandemic took hold. Like the rest of the world, we had no idea how long we’d be away, but we didn’t really imagine we’d still be operating our business with a remote workforce a year later. What a year it has been. It is incredible to look back and reflect on how our lives have changed, how we were able to adapt to this new way of living and working, and really importantly, how we were able to keep innovating to help communities and businesses during this difficult time. We have captured highlights of our work and efforts in our North America annual diversity and inclusion report, 2020 Power of YOU. At Experian, the safety and well-being of our colleagues has consistently been a top priority. As such, we have been able to focus on serving consumers and clients when and where they need help the most. As a company, we expanded our benefits to take care of our employees. Coworkers jumped in to take care of each other. Our employee resource group dedicated to mental health and caregiving partnered with colleagues to create a dynamic set of tools and guides tackling different topics every week through webinars, articles and personal, candid videos from leaders. We supported each other during times of social unrest. We celebrated progress in growing our business. We logged 18,000 volunteer hours to increase financial inclusion, support frontline healthcare workers, honor active duty military and veterans, and fight hunger in underprivileged communities. We leveraged our diversity of perspectives, backgrounds and experiences to help vulnerable populations in crisis from COVID-19, including launching our United for Financial Health program. We remain steadfast and committed to equity for all. We are proud to start the new year with this wonderful look back at last year, propelling us forward to more opportunities to innovate and serve. We invite you to check out the 2020 Power of YOU Report here.

Here’s what we expect in 2021: Putting a Face to Frankenstein IDs: Synthetic identity fraud – when a fraudster uses a combination of real and fake information to create an entirely new identity – is currently the fastest growing type of financial crime. The progressive uptick in synthetic identity fraud is likely due to multiple factors, including data breaches, dark web data access and the competitive lending landscape. As methods for fraud detection continue to mature, Experian expects fraudsters to use fake faces for biometric verification. These “Frankenstein faces” will use AI to combine facial characteristics from different people to form a new identity, creating a challenge for businesses relying on facial recognition technology as a significant part of their fraud prevention strategy. “Too Good to Be True” COVID Solutions: With the distribution of vaccines underway and wider availability of rapid COVID-19 testing, Experian expects that fraudsters will continue to find opportunities to capitalize on anxious and vulnerable consumers and businesses. Everyone needs to be vigilant against fraudsters using the promise of at-home test kits, vaccines and treatments as means for sophisticated phishing attacks, telemarketing fraud and social engineering schemes. Stimulus Fraud Activity, Round Two: For Americans suddenly out of work or struggling with the financial fallout from the pandemic, 2020’s government-issued stimulus funds were a welcome relief, but also an easy target for fraudsters to commit scams. Experian predicts fraudsters will take advantage of additional stimulus funding by using stolen data from consumers to intercept stimulus or unemployment payments. Say ‘Hello’ to Constant Automated Attacks: Once the stimulus fraud attacks run their course, Experian predicts hackers will increasingly turn to automated methods, including script creation (using fraudulent information to automate account creation) and credential stuffing (using stolen data from a breach to take over a user’s other accounts) to make cyberattacks and account takeovers easier and more scalable than ever before. With billions of records exposed in the U.S. due to data breaches annually, this type of fraud will prosper in 2021 and beyond until the industry moves away from its reliance on usernames and passwords. Survival of the Fittest for Small Businesses: As a result of COVID-19, businesses were left with no choice but to quickly shift to digital to meet the needs of consumers, and some were more prepared than others. In 2020, consumers may have been willing to give businesses time to adjust to the new normal, but in 2021 their expectations will be higher. Experian predicts businesses with lackluster fraud prevention tools and insufficient online security technology will suffer large financial losses in 2021 and beyond. While fraudsters will iterate on new and old methods of attack in 2021, Experian is always innovating to help businesses stay one step ahead. As a leader in fraud prevention, Experian offers a full suite of automated fraud prevention and detection tools that harness data and analytics to make businesses more secure. To learn more, check out Experian’s fraud prevention solutions and download the Future of Fraud Forecast.

As our world becomes increasingly data-driven, the demand for automation will continue to grow. At Experian, we believe that harnessing the power of data can create opportunities for businesses to succeed and society to thrive. We’re proud to have a culture dedicated to continuous innovation and it’s one of the reasons we were selected as the winner of Cloudera’s 2020 Data Impact Awards in the Data for Enterprise AI Category. The award honors organizations that have built and deployed systems for enterprise-scale machine learning and have harnessed AI to automate, secure, and standardize decision making. Cloudera’s annual Data Impact Awards recognizes organizations whose data projects deliver significant benefits to their business and the broader community. Experian was granted the award for the work our Business Information Services’ Data Enrichment Team did to build and launch six different data maintenance applications, which allowed us to more quickly identify data inconsistencies through automation and machine learning. An example of this is Experian’s Velcro application, which is powered by machine learning. In real-time, it can help prevent and resolve duplicate records while also improving the customer experience. This is just one example of how Experian is investing in data-driven solutions to create a better tomorrow on the road to recovery ahead of us. As we head into the new year, we will continue to innovate using the most cutting-edge technologies to make an impact in the business communities we serve. The winners, which each represent innovation and leadership in their respective industry, were selected by a panel of distinguished thought-leaders and expert industry analysts. To learn more about this award win, visit https://blog.cloudera.com/2020-data-impact-award-winner-spotlight-experian/. You can view the full list of 2020 Data Impact Award winners here.

While there is no question the pandemic continues to create a challenging financial situation for millions of consumers, this is not the case for everyone. Because Americans are finding themselves in unique financial situations, there is not a one size fits all solution for maintaining access to the credit economy. As 2020 comes to a close and U.S. consumers and businesses grapple with another surge in COVID-19 cases, it is critical for the credit services industry to continually recognize and assess the impact the pandemic is having on consumer’s financial health. At Experian, our role is to help lenders understand consumer’s unique circumstances, so they know who they are talking to and what risk an applicant represents at any given time. We use the power of data, including traditional credit data, alternative data and consumer permissioned data, to accomplish this objective. I was recently invited to speak with Cheddar’s Nora Ali to share my views on the Road to Recovery from the pandemic, how we can maintain access to the credit economy and ways consumers can protect their credit standing and financial health during this time. You can watch the full interview here. I believe data is key to maintaining access to the credit economy and protecting consumer financial health, especially in environments like the one we currently find ourselves in.

For the eighth consecutive year, the Orange County Register has named Experian as one of the Top Workplaces, with the company securing the #1 ranking for the second time in three years. The award, which is based on employee feedback in a survey of hundreds of leading companies in Orange County, recognizes our company’s culture of innovation and inclusion, and our commitment to employees and communities during the pandemic. For more than 40 years, Orange County has been at the heart of our North America operations, and as we persevere through these challenging times, we are especially honored to be recognized for our dedication to maintaining a healthy, collaborative work environment and achieving higher performance while giving back. This award demonstrates the resilience, talent and compassion of all the people who work here at Experian. Since the start of the pandemic, we have further expanded our dedication to social good by creating new opportunities to support employees and the broader community. Because we are founded on a culture of innovating through bringing together technology and data, we were able to quickly respond to COVID-19 and honor our commitment to using data for good. Maintaining company culture All our decisions are driven by our desire to lead with empathy, and ensuring our employees feel valued and protected, while simultaneously mobilizing our resources to positively impact society, creating greater levels of financial and social inclusion. Although we had technology in place to easily initiate working remotely, we supported the transition to remote working by launching initiatives dedicated to mental and physical well-being, including a COVID-19 Resource Center, enhanced sick-leave policies, increased opportunities to ensure continuity of professional development, as well as an ASPIRE to be Well guide, in partnership with our Employee Resource Groups (ERGs). Giving back Throughout the pandemic, our employees have felt compelled to help clients who were facing unprecedented and unforeseen challenges. Different groups and employees of all levels began working together to develop new products and services to help clients, customers and communities persevere. This included free credit reports for small business, adding video streaming service payments to Experian Boost, hosting #CreditChat on social media, the Experian CORE heatmap, COVID-19 U.S. Business Risk Index , Experian® Health Payer Policy Alerts and updated fraud protections through the Business Resources Website. As part of our United for Financial Health initiative, we also launched two new partnerships with non-profit organizations to empower vulnerable consumers and those marginalized by the pandemic. In collaboration with Operation HOPE, we are helping vulnerable communities improve financial health with its data, analytics, products and services. Most recently, we partnered with NAACP Empowerment Programs to offer Home Preservation Grants to African Americans at risk of losing their homes. Although COVID-19 has been a source of stress and anxiety for businesses and individuals alike, we remain committed to helping employees reach their full potential and demonstrating that values and purpose do not change in a crisis. We are honored that the Orange County Register is recognizing our tireless efforts to make a difference in the communities in which we live and work.