World

News about Experian from all over the globe:

Trust is foundational to everything we do at Experian. It’s how we build products people rely on, how we serve clients and consumers, and how we work together every day. That focus makes this year’s recognition from Fortune’s 100 Best Companies to Work For List even more meaningful. For 2026, Experian soared to ranking No. 38—our highest placement ever and a more than 20‑spot jump from last year. This marks our seventh consecutive year on the list. What makes this honor especially significant is how it’s earned. The ranking is based entirely on employee feedback from the Great Place to Work survey. Our people told us they feel welcomed, trusted to do their jobs, respected for who they are, and valued for the impact they make. They shared that Experian is a place where people can be themselves and count on one another. That internal trust matters externally. When employees trust their workplace, they do their best work. That translates directly into the trust our consumers and clients place in us—to handle data responsibly, deliver insights with integrity, and help people and businesses move forward with confidence. Our way of working has earned Experian the 2026 BIG Innovation Award for its AI-powered Experian-Assistant for Model Risk management, Top Score in the 2026 Equality 100, Best Place to Work for Disability Inclusion, and as one of the 25 World’s Best Workplaces™ 2025. This recognition reflects the culture our teams continue to build across North America—one grounded in trust, accountability, and purpose. We’re proud of the progress we’ve made, and we know there’s always room to go further. Thank you to everyone who places their trust in Experian. We don’t take it lightly. Learn more in the Experian 2025 Power of YOU Reports: English | Portuguese | Spanish

Identity is the cornerstone of trust. Trust allows businesses to grow and consumers to transact with confidence. It also enables digital ecosystems to function at scale. As AI becomes an active participant in every digital interaction, earning and protecting that trust has never been more critical. To build trust, companies need to recognize the people they’re interacting with online and distinguish good customers from fraudsters. Businesses look to Experian for our extensive consumer data, analytics, and decisioning solutions so they can more confidently identify, authenticate, and engage customers across digital channels. This week, we are accelerating that mission with the acquisition of AtData, a global leader in email-based identity intelligence. Email remains one of the most enduring and widely used digital identifiers. AtData brings real-time intelligence on more than 10 billion email addresses worldwide, adding a powerful and highly predictive signal to Experian’s identity and fraud platform. In a landscape shaped by automation and generative AI, the ability to assess email risk in real time can be a key asset in underwriting trust. Identity Powered by Real‑Time Email Intelligence AtData’s email intelligence provides signals such as domain reputation, account tenure, and behavioral risk to help distinguish legitimate customers from synthetic or manipulated identities. These signals can provide a better experience for good consumers, while supporting earlier detection of first-party fraud, third-party fraud, and synthetic identity schemes before losses occur. Going forward, email intelligence will play an important role in the next generation of Experian solutions, including agentic AI systems that can reason, adapt, and act on trusted identity signals in real time. When combined with Experian’s device intelligence, behavioral analytics, and advanced decisioning capabilities, these insights enable organizations to: Identify and authenticate consumers with greater confidence Detect fraud earlier with improved precision and speed Enhance engagement through richer, more connected identity profiles With AtData, we are not only expanding our data assets, we are also advancing a future where identity is more trusted. I’m excited to build upon our world-class identity and fraud solutions together.

We believe financial decisions should feel empowering, not overwhelming. Choosing how to protect your family, planning your next move, building your future, these are personal milestones. Yet too often, the tools meant to help consumers navigate them create friction instead of clarity. We are changing that. Our Consumer-First AI strategy starts with a simple belief: technology should make life easier for people. We’re building AI-powered experiences that meet consumers where they are, cut through complexity, and provide guidance that feels intuitive, supportive, and genuinely helpful. Reimagining Insurance Shopping Through Conversation One example is the launch of our Experian Insurance Marketplace, a leading platform to find and compare auto insurance rates[i], within ChatGPT. Shopping for insurance has long been a frustrating process. Consumers jump from site to site, repeatedly entering information and trying to decode policy differences, often still unsure if they found the right coverage at the right price. Now the experience can begin with a simple question inside ChatGPT. Consumers now can start their journey with Experian and compare estimated rates from more than 35 leading insurance carriers in our network, receive clear coverage explanations, ask follow-up questions in real time, and seamlessly transition into the Experian experience to explore personalized savings and switch carriers. What once took hours across multiple websites can now begin in one guided interaction. Powered by Experian’s Innovation Engine This experience is powered by Experian’s Insurance Marketplace platform and built on years of data expertise, advanced analytics, and strong carrier relationships. It reflects our ability to combine trusted data with emerging AI to create entirely new consumer experiences. For example, consumers can start with a ZIP code to explore price comparisons and, if they choose transition securely to Experian’s website for a personalized quote. This is Consumer-First AI in action. It is not technology for its own sake, but innovation designed to make life easier, build confidence, and give people greater control over their financial journey. Just the Beginning Experian has long helped people build credit, protect their identity, and improve their financial health. Bringing other capabilities, we offer like insurance into conversational AI is a natural extension of that mission. Insurance is only the start in seeing Experian via other platforms. As AI becomes a bigger part of our financial lives, we will continue expanding solutions both within our ecosystem and in other properties like ChatGPT that simplify complex moments and deliver smarter, more personalized guidance wherever consumers are or prefer to engage. Because at Experian, we are committed to being your BFF, your Big Financial Friend, showing up with trusted guidance, practical tools, and support exactly when it matters most. To explore the Experian Insurance Marketplace within ChatGPT or learn more, visit www.experian.com/insurance Insurance products are offered through Gabi Personal Insurance Agency, Inc., d/b/a Experian Insurance Services, a licensed insurance agency. Availability and savings vary by state. Savings are not guaranteed. For license information, visit https://www.experian.com/help/insurance-licenses-disclosure/ [i] Results will vary and some may not see savings.

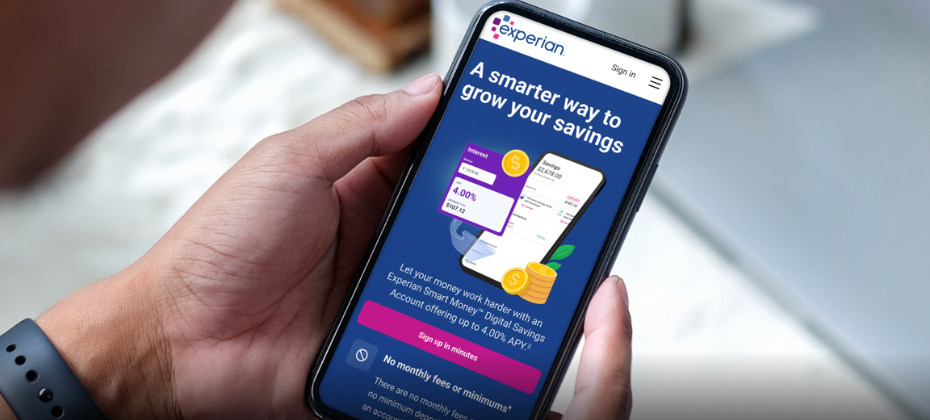

We’re starting the year strong by reaffirming our promise to empower consumers on their financial journeys. At Experian, everything we do is driven by our mission to bring Financial Power to All™—helping people not only understand where they stand but confidently move forward. That’s why I’m pleased to introduce the new high-yield Experian Smart Money™ Digital Savings Account[1], designed to make saving effortless, accessible, and more meaningful than ever before. This new offering is more than just a savings account—it represents an important evolution in how Experian supports financial progress. For years, we’ve helped tens of millions of consumers monitor their credit, improve their credit scores, and protect their identities. Now, by adding a high-yield digital savings account to our existing suite of financial health tools, we’re able to anchor that progress to something tangible: real balances and real momentum. With the ability to save built directly into the Experian ecosystem, members can track their savings growth alongside credit improvements, creating a clearer picture of their overall financial health. Positive financial behaviors—like paying down debt, making on-time payments, or improving utilization—can now be experienced in parallel with cash accumulation and stronger financial resilience, all in one trusted place. The Experian Smart Money™ Digital Savings Account offers up to 4.00% variable Annual Percentage Yield[2] (APY), which is nearly 10 times the national average savings rate[3], with no minimum balance or direct deposit requirement. It’s seamlessly integrated into the Experian membership experience, making it easier for consumers to take action the moment insight appears. This launch builds on the success of our Experian Smart Money™ Digital Checking Account & Debit Card introduced in 2023 and reflects our continued commitment to creating products that meet consumers wherever they are on their financial journey. We believe saving is a foundational financial behavior—and one that plays a powerful, often underappreciated role in credit outcomes. Strong credit health isn’t just about borrowing; it’s closely tied to liquidity, cash flow stability, and financial resilience. Having accessible savings can help consumers stay current on bills during income disruptions, build buffers that reduce reliance on higher-cost credit, and create flexibility that can support long-term credit improvement. In this way, a high-yield digital savings account becomes more than a place to store money—it becomes a practical tool for building healthier financial habits. Whether it’s emergency savings, goal-based saving, or smoothing cash flow, an Experian Smart Money Digital Savings Account enables consumers to turn good intentions into consistent action. This launch also reflects our broader evolution beyond a traditional credit bureau. Today, Experian membership provides access to credit monitoring and improvement tools, identity protection, a credit card marketplace, auto insurance comparison shopping, and personalized guidance through our AI-powered virtual assistant, EVA. Adding a high-yield digital savings account allows us to take the next step with our members—bridging the gap between insight and action. Instead of stopping at “here’s where you stand,” Experian can now help consumers actively build positive financial momentum. We’re extending our role as consumers’ BFF—Big Financial Friend—by making it easier to save, plan, and grow within the same ecosystem they already trust. By innovating and delivering products that truly make a difference in people’s everyday financial lives, we’re continuing to advance our mission and help consumers turn knowledge into progress. Learn more at experian.com/smartmoney. [1] The Experian Smart Money™ Debit Card is issued by Community Federal Savings Bank (CFSB), pursuant to a license from Mastercard International. Banking services provided by CFSB, Member FDIC. Experian is a Program Manager, not a bank. See Experian.com/legal. [2] The Annual Percentage Yield (APY) is 2.00%, 3.00% or 4.00% as of today’s date based on the Experian membership status. The APY may change at any time before or after your account is opened. Changes to the Experian membership can impact the APY, interest rate, and features. The interest rate and APY may be lower during membership trial periods. No minimum deposit to open account. Balance must be at least $0.01 to earn APY. Learn more. [3] As of Dec. 15, 2025, the national average rate for savings accounts was 0.39%, according to the FDIC.

Editor's Note (February 2026): Since the publication of this post, Experian communicated to its mortgage partners a new strategic pricing structure designed to bring more value to the industry. Our commitment to transparency in mortgage credit reporting pricing remains unchanged. Recent developments in the pricing of credit solutions for the mortgage industry have raised concerns about rising costs negatively impacting financial institutions and ultimately home buyers. We understand why lenders and trade groups are frustrated and we share in the concern. The system is complex yet there are also blatant attempts by some to take advantage of that complexity by spreading misinformation that makes it difficult to understand the drivers of cost and their implications. Here are the facts: Fact #1: Experian is not increasing the price of its credit reports for mortgage. In fact, the price of an Experian credit report for mortgage in 2026 will be exactly the same compared to 2025. Any accusations that we are raising the price of our credit reports by 50% are simply false. Fact #2: We made a marginal adjustment to the price of our data being used for processing scores in 2026. This reflects increasing complexity in consumer support, continued investments in data security, data accuracy, and regulatory compliance. This includes efforts to include more modern data sources, such as rent, utilities, buy now, pay later, short-term loans and cashflow advancements, among other sources, to more accurately reflect a consumer’s history and use of emerging financial utilities. Fact #3: National credit bureaus do not determine the price of tri-merge credit reports. The cost of these reports are based on a combination of inputs priced independently by multiple parties. Credit bureaus – Experian being one – make up only a portion of that equation. Tri-merge providers contract directly with originators, that pricing reflects our data usage/services, score algorithm costs and fees for services the reseller themselves provide. Sometimes those combined costs are reflected as “credit reports”, which is at best an oversimplification, at worst a misrepresentation. Experian is committed to transparency in our pricing. Fact #4: In October, FICO increased its royalty fees for its credit score from $4.95 to $10, an increase of approximately $5 per borrower, essentially doubling the cost of the FICO credit score in tri-merge credit reports. FICO also introduced their direct license program, which introduces unnecessary technological, operational and regulatory complexity for lenders and other market participants (including Experian), placing an even greater financial burden on the industry and inevitably, consumers. Mortgage decisions and credit scores are only as impactful and informed as the data that powers them. And simply put, scores do not exist without credit data powered by the credit bureaus. Credit reporting agencies like Experian operate under rigorous regulatory oversight, unlike score providers like FICO, because the accuracy, security, and fairness of the data we power is critical to the health of the U.S. financial system. Our costs reflect that responsibility, and the continued investments we are making to ensure data accuracy, security, and regulatory compliance to drive value for lenders and consumers alike. We share in the overall goal of making homeownership more accessible and affordable, but that can only happen through pricing transparency and collaboration, not deception and rhetoric. I’ve been in this industry for more than two decades, and I believe our industry only moves forward when it moves together. It’s time we focus on fairness and innovation to make meaningful progress toward a more efficient, inclusive, and sustainable mortgage ecosystem that brings financial power to all.

As COP30—the world’s largest UN climate summit—wraps up in Belém, Brazil, the global community is focused on turning commitments into action. At Experian, climate action is not just about reducing emissions. It’s about creating a fair and inclusive opportunities that benefit everyone. We’re using data and innovation to make that vision a reality, and this global summit is an important platform to share and accelerate this work. An area we’re particularly excited about is inclusive economic growth, in other words, creating opportunities for everyone to prosper while protecting the planet. For example, we’re seeing great progress in our agribusiness sector, where Experian is helping small producers access affordable credit through responsible, tech-enabled financial inclusion. This is sustainability in action, where climate resilience and social impact go hand in hand. Experian has also officially launched our Net Zero Transition Plan, detailing how we’re reducing emissions across our operations and supply chain while supporting a fair and inclusive transition. Here’s how we’re tracking: Operations: Progressing toward our target to cut Scope 1 and 2 emissions, meaning, those we generate directly such as fuel we burn on-site or in company vehicles, and energy we purchase to power our operations, by 50% by 2030 (a baseline we set in 2019), reaching 84% reduction in the first half of our 2026 fiscal year. Supply Chain: Advancing our Scope 3 goal to have 78% of suppliers adopt science-based targets by 2029, with coverage in the first half of our 2026 fiscal year, reaching 38%. These milestones reflect our award winning commitment to climate leadership and transparency. COP30 is about implementation, emphasizing collaboration and action. Experian’s participation reinforces our commitment to harness the power of data as a catalyst for climate solutions. From enabling businesses to measure and manage emissions to unlocking financial inclusion for communities most vulnerable to climate impacts, Experian is creating pathways for growth that are future-ready.

At Experian, we often say our people are our biggest superpower - and today, I’m thrilled to share that this belief has been recognised once again. Experian has been named one of the 2025 World’s Best Workplaces™ by Fortune and Great Place to Work® for the second year in a row. This achievement reflects the culture we’ve built together – one that’s welcoming, inclusive, and rooted belonging. It’s a celebration of every colleague who brings their whole self to work, who lifts others up, and who powers opportunities for our clients, consumers, and communities. We’ve made it our mission to create a workplace where everyone feels included, respected, and empowered. That’s why we’re proud to have earned top scores on the Corporate Equality Index and the Disability Equality Index, and to be recognised with the Outie Award for Workplace Excellence and Belonging. These recognitions matter. But what matters most is how our people experience life at Experian. Whether it’s collaborating, innovating, or growing through world-class development of products, services and contributing to our communities, our culture is designed to help everyone thrive. We’ve also made bold commitments to career development. Initiatives like Global Careers Week, the AI-driven performance coach Nadia, and the NextGen Forum – a global leadership development programme for emerging talent from across our regions – give our people the resources to take charge of their growth and build a “One Experian” mindset. Being named one of the World’s Best Workplaces is a moment to celebrate but also a reminder to keep aiming higher. The world of work is evolving fast, and so are we. From embracing AI to enhancing our digital workplace experience, we’ll continue to push forward and listen to our people every step of the way.

Trust begins with knowing who you’re doing business with. In financial services, trust depends on identity verification, protecting people and institutions from fraud while enabling seamless digital experiences. Experian has been named a Leader in the IDC MarketScape: Worldwide Identity Verification in Financial Services 2025 Vendor Assessment (doc #US52985325, September 2025). We believe this recognition reflects years of innovation in data, analytics, and AI to make digital trust simpler and more secure. Rethinking Verification for a Digital World Identity verification has evolved beyond static data checks. Today, it means interpreting signals across systems in real time. Financial institutions must prevent fraud without slowing legitimate customers, and Experian’s Ascend Platform™ helps strike that balance. It unites diverse data sources with intelligent analytics and decisioning tools so organizations can confidently verify identities. “We’re constantly listening to clients and evolving our capabilities, integrating AI, behavioral analytics, and new approaches like ‘know your agent’ to stay ahead of emerging risks,” said Keith Little, President of Experian Software Solutions. From Data to Confidence Experian was recognized for the following strengths: Access to a broad and diverse range of proprietary identity and credit data sources enables multilayered verification across different financial services use cases. The platform incorporates risk-based authentication, progressive onboarding, and behavioral analytics that enable fraud detection with reduced friction. NeuroID integration expands capabilities in behavioral monitoring, including detection of fraud rings and bot behavior during digital onboarding. “Experian demonstrates strength in identity verification by combining broad data assets with scalable workflows,” said Sam Abadir, Research Director for IDC Financial Insights. “This offers financial institutions both the consistency required for compliance and fraud prevention, and the dynamism needed to adapt to evolving customer expectations.” Building the Future of Digital Trust The landscape of identity verification is constantly shifting as regulations tighten and fraud tactics evolve. We lead by transforming vast data into actionable intelligence that protects people, strengthens businesses, and fosters trust. Experian’s identity verification offering is tackling the challenges of today, but equally important is our commitment to staying ahead of what’s next. To learn more. click here: Financial Services 2025 Vendor Assessment.

Experian is a cornerstone of the U.S. housing finance system, empowering millions of consumers to achieve the dream of homeownership and enabling lenders to make safe, sound, and inclusive credit decisions. At the heart of every credit score is data - and there is no FICO score without credit bureau data. Our information powers the accuracy, reliability, and fairness of scores across the market. FICO is now proposing an aggressive strategy to restructure distribution in order to push through an unprecedented price increase for its own benefit. The new direct licensing model introduces unnecessary technological, operational, and regulatory complexity for lenders and other market participants - complexity that ultimately increases costs and risks for the housing ecosystem. On pricing, the math speaks for itself. FICO has now more than doubled its fee from $4.95 to $10, and it’s an even worse increase under the proposal for a $33 closing fee. Make no mistake, this will place an even greater financial burden on the industry, that will inevitably be passed to consumers. Experian has long supported the industry’s evolution toward more modern, inclusive, and efficient credit solutions. We have a track record of partnering with lenders, agencies, and regulators to ensure innovation strengthens - not hinders - the system. FICO’s actions only underscore the need for alternatives that deliver value, not additional burden. As a result, we are committed to accelerating the adoption of VantageScore - an innovative, proven, and cost-effective solution that better serves both lenders and consumers. We remain confident in our position, our client partnerships, and our ability to deliver solutions that balance affordability, fairness, and accuracy. Experian will continue to work with the industry to drive innovation, empower consumers, and strengthen the housing finance system for the future.