All posts by Editor

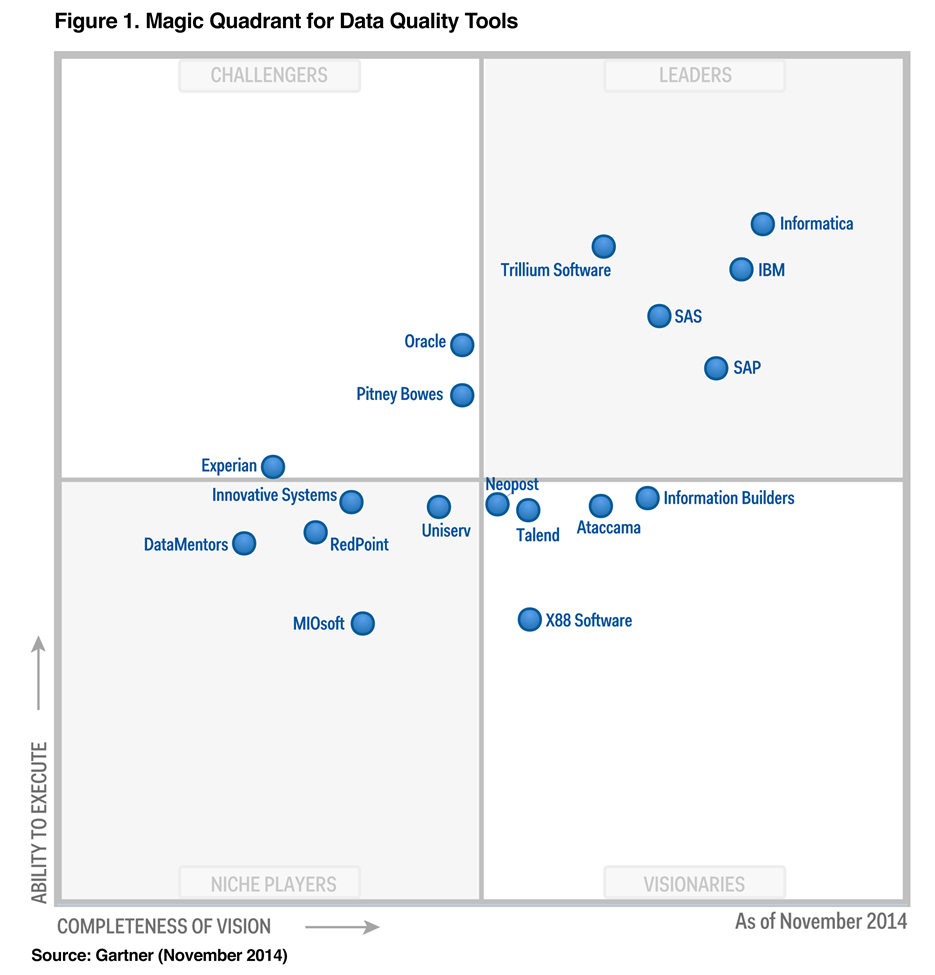

Today, we are excited to announce that Experian has made it onto the Gartner Magic Quadrant for Data Quality Tools.

Black Friday has come and gone, and the holiday shopping season is in full swing. This year, retailers and economic experts alike have high hopes for robust spending and a needed economic boost. And so far the results look promising. On Cyber Monday, alone, the top online retail sites registered 242 million visits, followed closely by Black Friday’s 228 million visits. And according to a new survey from Experian Consumer Services, 36 percent of consumers plan to spend more on gifts this year than they did in 2013.

At Experian, everything we do is about putting insights into action. This entails formulating and analyzing insights that can help both consumers and businesses alike. We sat down with two of Experian’s leading experts, one from the consumer side of the business and another from our marketing services business, to find out more about the key trends that will define this holiday shopping season.

Guy Abramo, President, Experian Consumer Services and Matt Seeley, President, North America, Experian Marketing Services share their thoughts and insights below:

Black Friday has come and gone, and the holiday shopping season is in full swing. This year, retailers and economic experts alike have high hopes for robust spending and a needed economic boost. And so far the results look promising. On Cyber Monday, alone, the top online retail sites registered 242 million visits, followed closely by Black Friday’s 228 million visits. And according to a new survey from Experian Consumer Services, 36 percent of consumers plan to spend more on gifts this year than they did in 2013.

At Experian, everything we do is about putting insights into action. This entails formulating and analyzing insights that can help both consumers and businesses alike. We sat down with two of Experian’s leading experts, one from the consumer side of the business and another from our marketing services business, to find out more about the key trends that will define this holiday shopping season.

Guy Abramo, President, Experian Consumer Services and Matt Seeley, President, North America, Experian Marketing Services share their thoughts and insights below:

Balancing holiday marketing efforts with fraud prevention requires a coordinated approach according to survey findings from 41st Parameter, a part of Experian. The survey results from 250 marketers released today, looks at the relationship between omnichannel retailing, fraud prevention and the holiday shopping season. The findings show that few marketers understand the full benefit of fraud-prevention systems on their activities as 60 percent of marketers were unsure of the cost of fraud to their organization. The survey also indicated that 40 percent of marketers said their organization had been targeted by hackers or cybercriminals. Download the Holiday Marketing Fraud Survey: http://snip.ly/JoyF With holiday shopping in full stride, 35 percent of businesses said they planned to increase their digital spend for the 2014 holiday season. Furthermore, Experian Marketing Services reported that during 2014, 80 percent of marketers planned on running cross-channel marketing campaigns. As marketers integrate more channels into their campaigns, new challenges emerge for fraud-risk managers who face continuous pressure to adopt new approaches. Here are three steps to help marketers and risk managers maintain a frictionless experience for customers: Marketers should communicate their plans early to the fraud-risk team, especially if they are planning to target a new or unexpected audience. Making this part of the process will reduce the chances that risk management will stop or inhibit customers. Ensure that marketers understand what the risk-management department is doing with respect to fraud detection. Chances are risk managers are waiting to tell you. Marketers shouldn’t assume that fraud won’t affect their business and talk to their risk-management division to learn how much fraud truly costs their company. Then they can understand what they need to do to make sure that their marketing efforts are not thwarted. “Marketers spend a great deal of time and money bringing in new customers and increasing sales, especially this time of year, and in too many cases, those efforts are negated in the name of fraud prevention,” said David Britton, vice president of industry solutions, 41st Parameter. “Marketers can help an organization’s bottom line by working with their fraud-risk department to prevent bad transactions from occurring while maintaining a seamless customer experience. Reducing fraud is important and protecting the customer experience is a necessity.” Few marketers understand the resulting impact of declined transactions because of suspected fraud and this is even more pronounced among small businesses, with 70 percent saying they were unsure of fraud’s impact. Fifty percent of mid-sized business marketers and 67 percent of large-enterprise marketers were unsure of the impact of fraud as well. An uncoordinated approach to new customer acquisition can result in lost revenue affecting the entire organization. For example, the industry average for card-not-present declines is 15 percent. However, one to three percent of those declined transactions turn out to be valid transactions, equating to $1.2 billion in lost revenue annually. Wrongfully declined transactions can be costly as the growth of cross-channel marketing increases and a push towards omnichannel retailing pressures marketers to find new customers. “Many businesses loosen their fraud detection measures during high peak time because they don’t have the tools to review potentially risky orders manually during the higher-volume holiday shopping period,” said Britton. “Criminals look to capitalize on this and exploit these gaps in any way possible, taking an omnifraud approach to maximizing their chances of success. Striking the right balance between sales enablement and fraud prevention is the key to maximizing growth for any business at all times of the year.” Download Experian’s fraud prevention report to learn more about how businesses can address these new marketing challenges.

The world of mobile devices is constantly changing—everything is faster, bigger and better, and consumers have become more savvy and discerning about the features and benefits that make their lives more convenient, and in many cases, more manageable.

I use my phone to do everything from simple tasks like checking email or Facebook, to downloading coupons, buying movie and concert tickets, to checking my bank balance and making deposits on the fly (which is such a great feature).

The world of mobile devices is constantly changing—everything is faster, bigger and better, and consumers have become more savvy and discerning about the features and benefits that make their lives more convenient, and in many cases, more manageable.

I use my phone to do everything from simple tasks like checking email or Facebook, to downloading coupons, buying movie and concert tickets, to checking my bank balance and making deposits on the fly (which is such a great feature).

Do you already have a plan for your holiday shopping game this year? A recent study commissioned by Experian Consumer Services shows that spending confidence continues to recover, with 11 percent of those surveyed saying they anticipate spending more than they did last year on holiday gifts. Respondents plan to spend an average of $757.57 this year, up from $721.96 in 2013.

Bankcard lending is trending upward, according to the 2014 Experian “State of Credit” report. One in 17 consumers obtained at least one bankcard this year, compared with one in 21 people back in 2013. Consumers now carry an average of 2.18 bankcards apiece (an increase of 4.2 percent), and an average of 1.54 retail cards (a jump of 6.7 percent). In other words, credit availability is on the rise. Can we do it smarter this time?

Experian unveiled its fifth annual State of Credit report today, which provides a snapshot of consumers’ credit scores broken out nationally and by local market. This year’s findings show that the nation’s average VantageScore has improved by two points since last year, coming in at 666. In the city listings, Mankato, MN takes the top spot with a VantageScore of 706 and Greenwood, MS residents have the lowest score of 609 in the study. While the report gives residents of certain cities reason to celebrate their higher scores, the study isn’t meant make the lower cities sing the blues. These types of data-driven insights are meant to help consumers — to give them a reason to be interested in credit, to want to understand and improve their financial well-being, and to become a more savvy credit user and manager.

With all the discussions around the risks of big data, the fact that it can be used as a powerful enabler of good seems to be missed. The benefits of big data can be seen throughout our day to day lives from simple things like traffic alerts to more impactful purposes like those seen in today’s healthcare environment.

At Experian we serve more than 2,800 hospitals and 9,000 physician practices and use big data to help serve their patients as quickly and efficiently as possible. Our data and technology guides hospitals, physicians and patients step by step through an increasingly complex healthcare process.

With all the discussions around the risks of big data, the fact that it can be used as a powerful enabler of good seems to be missed. The benefits of big data can be seen throughout our day to day lives from simple things like traffic alerts to more impactful purposes like those seen in today’s healthcare environment.

With all the discussions around the risks of big data, the fact that it can be used as a powerful enabler of good seems to be missed. The benefits of big data can be seen throughout our day to day lives from simple things like traffic alerts to more impactful purposes like those seen in today’s healthcare environment.

At Experian we serve more than 2,800 hospitals and 9,000 physician practices and use big data to help serve their patients as quickly and efficiently as possible. Our data and technology guides hospitals, physicians and patients step by step through an increasingly complex healthcare process.

With all the discussions around the risks of big data, the fact that it can be used as a powerful enabler of good seems to be missed. The benefits of big data can be seen throughout our day to day lives from simple things like traffic alerts to more impactful purposes like those seen in today’s healthcare environment.

More than 10 years ago I spoke about a trend at the time towards an underutilization of the information being managed by companies. I referred to this trend as “data skepticism.” Companies weren’t investing the time and resources needed to harvest the most valuable asset they had – data.

Today the volume and variety of data is only increasing as is the necessity to successfully analyze any relevant information to unlock its significant value. Big data can mean big opportunities for businesses and consumers.

More than 10 years ago I spoke about a trend at the time towards an underutilization of the information being managed by companies. I referred to this trend as “data skepticism.” Companies weren’t investing the time and resources needed to harvest the most valuable asset they had – data.

Today the volume and variety of data is only increasing as is the necessity to successfully analyze any relevant information to unlock its significant value. Big data can mean big opportunities for businesses and consumers.