Small Business Credit Insights

Join the experts from Experian for an insightful discussion about small business performance and the greater economy.

Explore key Q1 2025 small business credit trends, risks, and growth signals with insights tailored for today’s data-driven risk leaders.

AI is reshaping work, driving small business growth. Discover how AI, corporate shifts, and Gen Z are fueling an entrepreneurial boom.

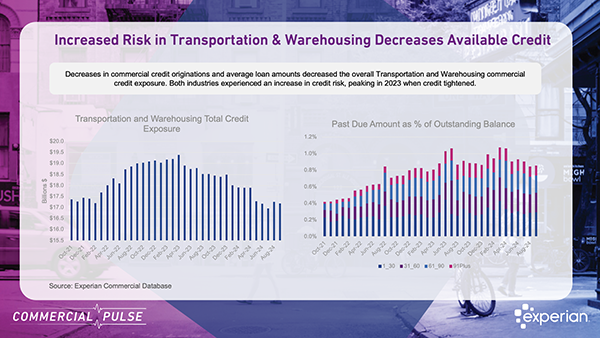

Fresh Insights from the latest Commercial Pulse Report, highlighting growth and credit challenges in U.S. transportation and warehousing.

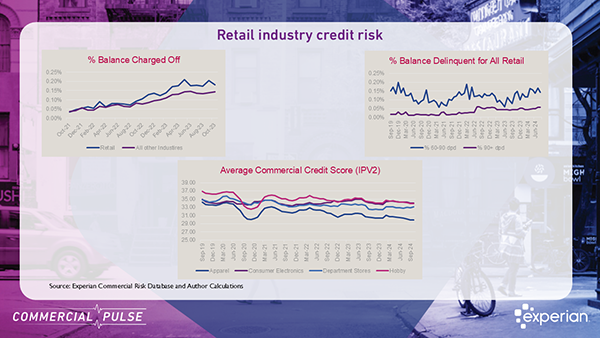

Explore the latest retail insights from Experian’s Commercial Pulse Report: credit demand surges, lending tightens, and retail growth slows.

The Fall Beyond The Trends report offers a unique view into the challenges hitting small businesses, and how to navigate a cooling economy.

Join the experts from Experian for a review of quarterly small business credit performance along with a macroeconomic outlook.

The Beyond the Trends report highlights indicators which offer insights on labor, prices, commercial credit and economic conditions.

Experian Main Street Report says strength in the economy pushes through inflation. Download for analysis on Q1 small business performance.