Small Business Credit Insights

Experts from Experian provide a quarterly business credit review on Q1 2024 credit performance, along with an economic outlook.

The Beyond the Trends report highlights indicators which offer insights on labor, prices, commercial credit and economic conditions.

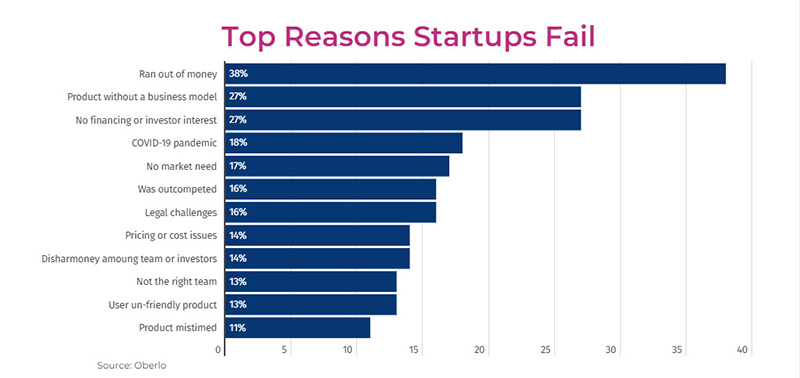

Download our latest Commercial Pulse Report for economic insights and a deep dive on reasons why so many startups fail in first 5 years.

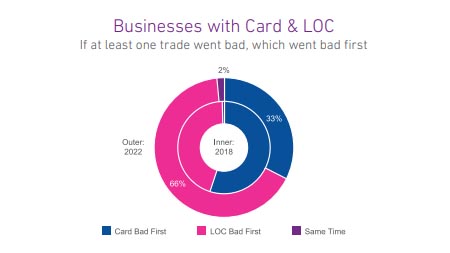

Since January 2021, a seasonally adjusted average of 444K new businesses opened each month, 52% higher than the pre-pandemic 2018-2019 monthly average. In light of the influx of new businesses, and in a higher-interest rate environment, the goal of this week’s analysis was to evaluate if commercial credit usage and payments by product shifted pre- and post-pandemic. Businesses with two different trade types were evaluated as of 2018 (prepandemic) and 2022 (post-pandemic). The two-trade-type combinations observed were Card + OECL (open ended credit line), Card +Term Loan, Card Lease, and Card + LOC (line of credit). Despite more younger businesses entering the market and lenders tightening credit policies over the past two years, businesses with two-trade types had higher lines/loans post-pandemic. Delinquencies also increased post-pandemic for all the two-trade type combinations except businesses with a Card & OECL. Commercial Cards are the most prevalent type of credit for businesses. As businesses grow, they seek additional credit for business needs such as expansion, new facilities, and acquisitions. When businesses seek additional credit, it is most often in the form of commercial loans, leases and credit lines which compared to cards, generally provide higher levels of funding, longer terms and higher monthly fixed payments. For businesses that had two types of accounts, including a commercial card with another commercial credit product, the commercial card stayed current longer and more often the non-card product went delinquent first. Businesses rely on commercial cards for day-to-day operating expenses and lower dollar financing needs. Furthermore, commercial card balances are significantly lower than any of the other commercial trade types allowing for a lower monthly minimum payment to keep the card in good standing. What I am watching: Federal Reserve Chairman Powell stated in last week’s Congressional hearings that the Fed will act slowly and cautiously in terms of cutting interest rates. With inflation declining but still persistent and the labor market still robust, rate cuts may not occur until the second half of the year. Download Report Download the latest version of the Commercial Pulse Report here. Better yet, subscribe so you'll get it in your inbox every time it releases, or once a month as you choose.

The Beyond the Trends report highlights indicators which offer insights on labor, prices, commercial credit and economic conditions.

Retail sales reached a 4-year high of over $615B in December 2023 with yearly retail sales growing 4.6%. At the same time, lenders are tightening credit and businesses within the retail sector are showing signs of stress with higher late-stage delinquency rates and falling commercial credit scores. We see retailers seeking commercial credit less often, new originations slowing and lower lines over the past several months. As retail sales continue to rise so does the proportion of online retail sales. Online sales peaked during the COVID-19 pandemic and fell slightly once the lockdowns were lifted. Online retail sales remain approximately 56% higher than pre-pandemic levels and are trending up and may soon exceed 2020 levels. Growth in online retail sales has led to growth in retail returns. Retail returns peaked in 2022 at over $800MM and over 16% of total retail sales. Prior to 2021, retail returns as a percentage of retail sales averaged 8.9%, since 2021 that rate has grown to 14.6%. As returns increase so do fraudulent returns. Retailers have implemented strategies and solutions to address retail returns which resulted in a decrease in return dollars between 2022 and 2023 yet the percentage of returns that were fraudulent increased from 10.2% to 13.7% or over $100B. Increases in both legitimate and fraudulent returns are prompting retailers to identity solutions and operational strategies to slow growth across all returns. What I am watching: The U.S. economy expanded 3.3% in Q4 2023, and 2023 real GDP increased 2.5% over 2022. Strong consumer spending fueled the economy. Multiple sources are expecting The Federal Reserve to cut interest rates up to six times in 2024 with the rate cuts beginning in Q2 2024 and continuing into 2025. Lower interest rates likely means that consumer spending will continue at an elevated rate. As spending continues to increase, specifically in the retail sector, the need for commercial credit could continue to slow as cash-flows satisfy operational capital requirements. Cash on hand should begin to satisfy outstanding delinquencies, improving commercial credit scores resulting in improved access to commercial credit.

New Report: Will the 2023 holiday season hinge on generosity? The latest Beyond the Trends report offers evidence it may.

Gain insight on small business credit conditions by attending our quarterly webinar.

Highlights from the latest Beyond the Trends report Are you curious about the trends affecting the small business economy? The just released Summer 2023 Beyond the Trends report is packed with valuable insights based on data from over 25 million active businesses and the expert opinions from Experian’s V.P. of Commercial Data Science. This post covers some of the report's highlights, download your copy for the full scoop. A word from the report’s author: Energy Prices and Consumer Relief One of the most crucial takeaways from the report is that consumers and small businesses can expect continued relief in fuel prices in the coming months. This relief is due to the increased production of fuel in the United States and other countries. This production, coupled with other global and domestic factors, will provide more affordability in fuel costs for consumers and small businesses. This will help them manage their expenses better and, in turn, help producer costs decline, leading to more positive economic developments. Small Business Delinquency Small businesses, especially those that were propped up by stimulus money, are beginning to feel the pinch of inflation that is eating into their margins. Due to this, their savings are running lean, and many businesses are experiencing a rise in delinquencies. Delinquency rates have now exceeded pre-pandemic levels. Still, the report suggests that this is where they would expect delinquencies to be as the economy begins to grow gradually. Optimism Amidst Challenges Despite the lingering challenges and uncertainties brought about by the pandemic, small business owners remain optimistic. The report shows that the overall sentiment among small business owners is still positive, and they continue to seek out opportunities and innovations that could lead to growth and success. This is a positive development, and it's critical for businesses to continue to be agile and open to new opportunities and ideas. In closing: Small businesses are facing challenges such as filling job openings, higher costs, delinquencies and rising debt, but they remain optimistic and focused on opportunities for growth. By staying true to their values and fundamentals, businesses can thrive even in uncertain times. Grab your copy of the Summer 2023 Beyond the Trends report for more interesting insights on small businesses and their challenges. Download Beyond The Trends Summer 2023 Report