Federal policy just removed up to $12 billion in annual higher education financing from the federal system.1 The families of undergrad and graduate students will look to private lenders, and how those lenders underwrite the new population will determine who captures market share.

For decades, Parent PLUS and Grad PLUS loans served as a federal backstop for higher education. Parent PLUS allowed parents to bridge the gap between financial aid and the full cost of attendance, with no annual or aggregate borrowing limits, while Grad PLUS enabled graduate and professional students to finance education costs beyond standard federal loan limits. Starting July 1, 2026, that backstop changed.

The One Big Beautiful Bill Act (OBBBA) ends uncapped federal student borrowing.2 Parent PLUS is now capped at $20,000 per year per dependent student.3 Graduate PLUS is eliminated for new borrowers4 and replaced by annual limits of $20,500 for most graduate students and $50,000 for designated professional programs, as currently defined, with a combined federal lifetime ceiling of $257,500 across all federal loans.5

Against college costs that run from $30,000 annually at public in-state institutions to more than $62,000 at private nonprofit colleges6, that math leaves a substantial funding gap for families and individuals that did not exist before.

Private lenders will close that gap, Lenders who are ready now will define the market.

The families entering private markets

The first instinct among some lenders is to assume that families losing access to federal coverage are high-risk borrowers. The data says otherwise.7 Many of the families hitting the Parent PLUS cap are already engaged with the federal student loan process and have successfully navigated the Parent PLUS application process, including the program’s adverse credit history screening.8 Many are financing students at higher-cost institutions where the new annual and lifetime borrowing limits create funding gaps that previously did not exist.9 They are not uniformly subprime.10 Instead, they represent a newly displaced population that may increasingly seek private education loans as federal borrowing options narrow.

The graduate school gap is even more pronounced. Roughly 38 percent of graduate borrowers in recent cohorts exceeded the new federal borrowing limits.11 These are professional and graduate students who previously relied on Grad PLUS loans to cover tuition above the base unsubsidized loan limits. Students already enrolled in a program with a prior Direct Loan disbursement retain legacy access for up to three years. New borrowers, however, are limited to capped Direct Unsubsidized Loans rather than Grad PLUS financing. As a result, some students in high-cost graduate and professional programs will face potential funding gaps that private lenders will increasingly be asked to fill.

Sallie Mae projects 12 to 14 percent year-over-year growth in private loan originations in 2026.12 Online lenders are adding new products. Banks are largely staying out. The lenders who move first with the right underwriting infrastructure will have the advantage.

A parallel market is expanding simultaneously that lenders should be watching. Approximately fifteen states operate nonprofit student loan authorities funded through tax-exempt bond programs, meaning they are not subject to OBBBA borrowing caps and can lend up to the full cost of attendance. In direct response to the July 1 changes, Massachusetts (MEFA) expanded its graduate loan program to support students in law, medicine, dentistry, and nursing, offering undergraduate loans with no annual limit at rates that undercut the federal Parent PLUS interest rate.13 Rhode Island (RISLA) expanded its graduate programs to full cost of attendance coverage,14 and Pennsylvania (PHEAA) allows graduate and professional students to borrow up to $300,000 in aggregate.15 Other active programs include Iowa (ISL), Vermont (VSAC), Minnesota (SELF), Connecticut (CHESLA), New Jersey (NJCLASS), New Hampshire (NHHEAF), Maine (FAME), Kentucky, North Dakota (DEAL), Alaska (ACPE), Oklahoma, and Texas (Brazos).16 These programs are mission-driven rather than margin-driven, which means they face the same underwriting challenges as commercial lenders but with a mandate to expand access rather than simply filter risk.

As FAFSA season approaches and families research how to fill the gap, state programs will surface prominently alongside commercial lenders in every borrower search, making awareness of this landscape an important part of any private lending strategy.

OBBBA federal student loan borrowing caps

Final Confirmed Limits | Effective July 1, 2026 | One Big Beautiful Bill Act (Public Law 119-21, signed July 4, 2025)

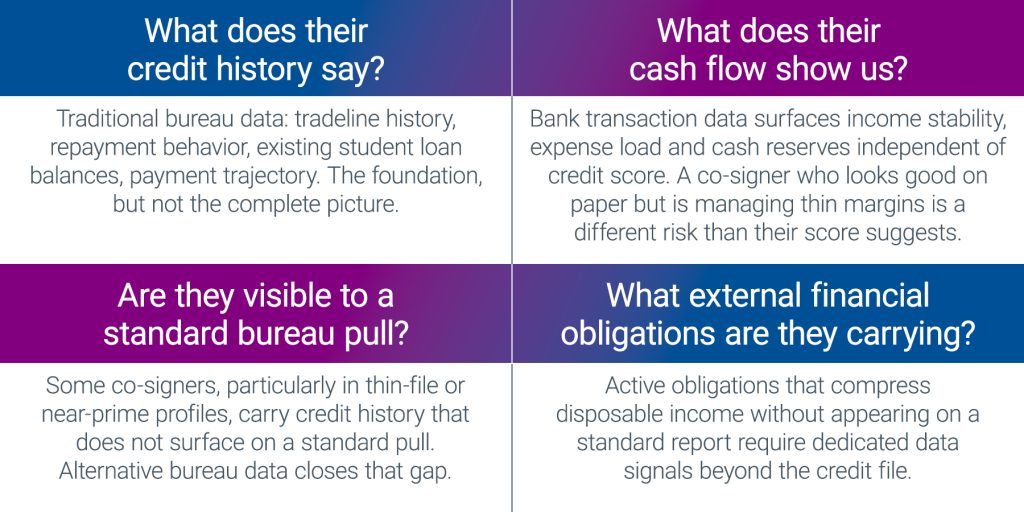

The underwriting challenge: Co-signers are the critical variable

More than 90 percent of private undergraduate loans are co-signed, because most student borrowers have thin or nonexistent credit histories.17 As this new population enters the private market, the co-signer is effectively the credit backbone of the loan. Approving more qualified borrowers in this market means approving more qualified co-signers, and that requires a fuller picture of co-signer financial health than a credit score alone provides.

Four questions should drive every co-signer underwriting conversation:

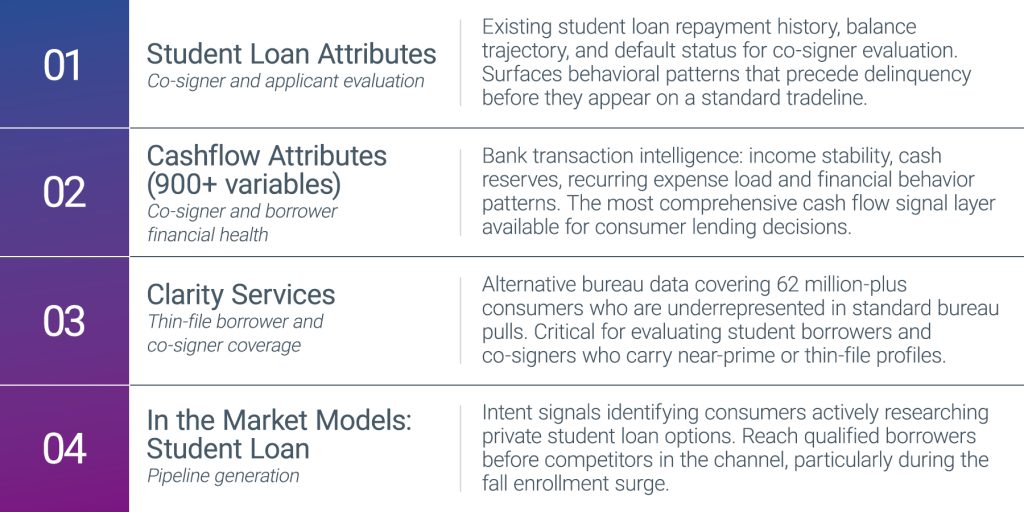

The signal layer that makes better decisions possible

Getting co-signer underwriting right in this environment requires combining three distinct data layers: traditional credit bureau data, alternative bureau coverage for consumers who are thin-file or near-prime and behavioral cash flow signals from bank transaction data. Together, they answer a question that no single data source can: is this co-signer able to take on this loan if the student borrower cannot?

ALSO WORTH KNOWING

For co-signers with existing federal student loan exposure: administrative wage garnishment on defaulted federal loans can redirect up to 15 percent of disposable income, without a court order or public record. This does not appear on a standard bureau pull. Student loan garnishment attributes surface this signal, giving lenders a more complete picture of a co-signer’s available cash flow before a credit decision is made.

Who captures this market

The private student lending opportunity created by the OBBBA is significant, but it is not self-selecting. Lenders who underwrite the new population using a single-bureau credit score may approve fewer qualified borrowers and reject some who should have been approved, potentially leaving volume on the table while competitors take it. Lenders who build a multi-signal view of borrower and co-signer financial health will say yes more often, more accurately, and at better risk-adjusted margins.

The enrollment cycle is already in motion. Families are comparing their federal aid packages against their actual costs and identifying the gap right now. The lenders positioned to reach and underwrite them through the fall cycle are the ones who will establish the origination relationships that carry through the full loan term.

Experian can help you underwrite the new population

From in-market student loan signals and co-signer cash flow assessment to alternative bureau data and model development on the Ascend Platform, Experian gives private lenders the data infrastructure to reach and approve the families entering private markets this fall.

Sources:

[1] Jobs for the Future, “What Do OBBBA’s Tighter Borrowing Limits Mean for Students?” August 27, 2025, jff.org

[2] U.S. Department of Education. Federal Student Loan Program Provisions Effective Upon Enactment Under the One Big Beautiful Bill Act. FSA Knowledge Center, 2025. studentaid.gov. Implementing Public Law 119-21, signed July 4, 2025.

[3] University of Maine Student Financial Services. Aid Changes Under OBBBA. umaine.edu, 2026.

[4] U.S. Department of Education. Reimagining and Improving Student Education — Federal Student Loan Program Final Regulations. 91 Fed. Reg. (May 1, 2026)

[5] U.S. Department of Education. U.S. Department of Education Concludes Negotiated Rulemaking Session. ed.gov, 2026.

[6] College Board. Trends in College Pricing and Student Aid 2025-26. collegeboard.org, 2025.

[7]Brookings Institution, Capping the Wrong Problem: Why Parent PLUS Loan Limits May Miss the Mark

[8]Federal Student Aid, Direct PLUS Loans for Parents

[9]Brookings Institution, Capping the Wrong Problem: Why Parent PLUS Loan Limits May Miss the Mark

[10]Brookings Institution, Capping the Wrong Problem: Why Parent PLUS Loan Limits May Miss the Mark

[11] Jobs for the Future, “What Do OBBBA’s Tighter Borrowing Limits Mean for Students?” August 27, 2025, jff.org

[12]SLM Corporation. Form 8-K: First Quarter 2026 Earnings Results.

[13] Massachusetts Educational Financing Authority (MEFA). MEFA Responds to Federal Student Loan Restrictions with Expanded, Competitive State-Based Options. BusinessWire, June 25, 2026. businesswire.com.

[14] Rhode Island Student Loan Authority (RISLA). Graduate Loans. risla.com, accessed July 2026.

[15] The Century Foundation. State Student Loan Programs: A Private Loan by Any Other Name? tcf.org, July 2026.

[16] Education Finance Council. Member Programs. efc.org.

[17] https://protectborrowers.org/wp-content/uploads/2026/03/Access-Denied-Private-Student-Loan-Report.pdf