Commercial Pulse Report | 6/17/2025

Economic uncertainty is often seen as a deterrent to growth, but for many Americans, it’s become the fuel for a fresh start. As inflation wavers and traditional employment structures shift, more individuals are stepping out of corporate roles to pursue business ownership. In this week’s Commercial Pulse Report, we take a closer look at what’s driving this wave of entrepreneurial activity.

Gen X Leads the Charge Toward Self-Employment

According to Guidant Financial’s 2025 Small Business Trends report, Generation X is leading the charge. Many in this age group are opting out of traditional career paths, motivated by a desire for autonomy, flexibility, and a more purposeful work life. According to Guidant’s report, Gen X holds the largest share of U.S. small business ownership, with a significant portion of these entrepreneurs transitioning from established careers.

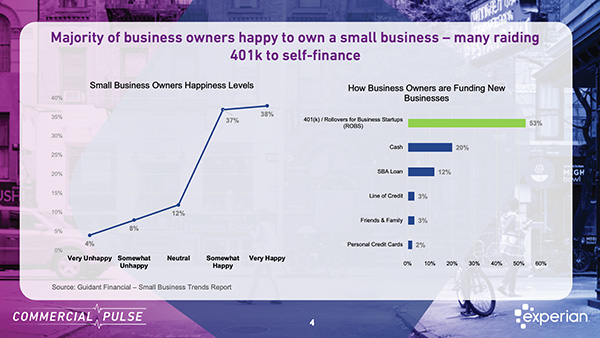

What’s driving this shift? Dissatisfaction with corporate life and a strong desire to be one’s own boss are leading motivators. It’s a story of experienced professionals reevaluating priorities and seeking more control over their financial future. And it appears to be a fulfilling decision—75% of small business owners report being happy with their choice to go independent.

Retirement Savings Power New Ventures

A surprising—but telling—statistic in ’s report: 53% of new business owners used 401(k) retirement funds to launch their ventures. This trend underscores a growing willingness to invest personal wealth into long-term entrepreneurial aspirations. Known as Rollovers as Business Startups (ROBS), this approach allows individuals to use retirement funds without early withdrawal penalties.

It’s a bold move, signaling high confidence among business owners—but also highlighting gaps in access to traditional funding channels. Entrepreneurs are taking on more personal risk, in part because institutional capital isn’t always accessible to young businesses.

Interestingly, 56% of all new businesses are either newly founded or existing independent ventures, showing a diverse range of entrepreneurial approaches—from solo startups to revitalized legacy brands.

The Credit Dillema for Young Businesses

Experian’s data shows that businesses under two years old account for more than 50% of new commercial card originations. These companies are opting for credit cards over term loans due to fewer barriers to entry, but this often means lower funding limits. Meanwhile, newer businesses face steeper challenges securing traditional loans. They now represent just 15% of term loan originations, down from 27% in 2022.

For lenders, policy makers, and service providers, these trends underscore the need to rethink how we support emerging businesses. From alternative funding tools to better credit-building pathways, there’s a growing opportunity to empower America’s newest entrepreneurs.

Stay Ahead with Experian

- ✔ Visit our Commercial Insights Hub for in-depth reports and expert analysis.

- ✔ Subscribe to our YouTube channel for regular updates on small business trends.

- ✔ Connect with your Experian account team to explore how data-driven insights can help your business grow.

Related Posts

Experian Commercial Pulse explores how AI is changing credit risk with a fascinating study of high-impact AI industries.

Understand the credit dynamics of women-owned small businesses and their critical role in the growth of the U.S. economy.

Banking transformation is accelerating through consolidation, digital adoption, and AI innovation. What must CROs prepare for next?