All posts by Destiny White

Trust is foundational to everything we do at Experian. It’s how we build products people rely on, how we serve clients and consumers, and how we work together every day. That focus makes this year’s recognition from Fortune’s 100 Best Companies to Work For List even more meaningful. For 2026, Experian soared to ranking No. 38—our highest placement ever and a more than 20‑spot jump from last year. This marks our seventh consecutive year on the list. What makes this honor especially significant is how it’s earned. The ranking is based entirely on employee feedback from the Great Place to Work survey. Our people told us they feel welcomed, trusted to do their jobs, respected for who they are, and valued for the impact they make. They shared that Experian is a place where people can be themselves and count on one another. That internal trust matters externally. When employees trust their workplace, they do their best work. That translates directly into the trust our consumers and clients place in us—to handle data responsibly, deliver insights with integrity, and help people and businesses move forward with confidence. Our way of working has earned Experian the 2026 BIG Innovation Award for its AI-powered Experian-Assistant for Model Risk management, Top Score in the 2026 Equality 100, Best Place to Work for Disability Inclusion, and as one of the 25 World’s Best Workplaces™ 2025. This recognition reflects the culture our teams continue to build across North America—one grounded in trust, accountability, and purpose. We’re proud of the progress we’ve made, and we know there’s always room to go further. Thank you to everyone who places their trust in Experian. We don’t take it lightly. Learn more in the Experian 2025 Power of YOU Reports: English | Portuguese | Spanish

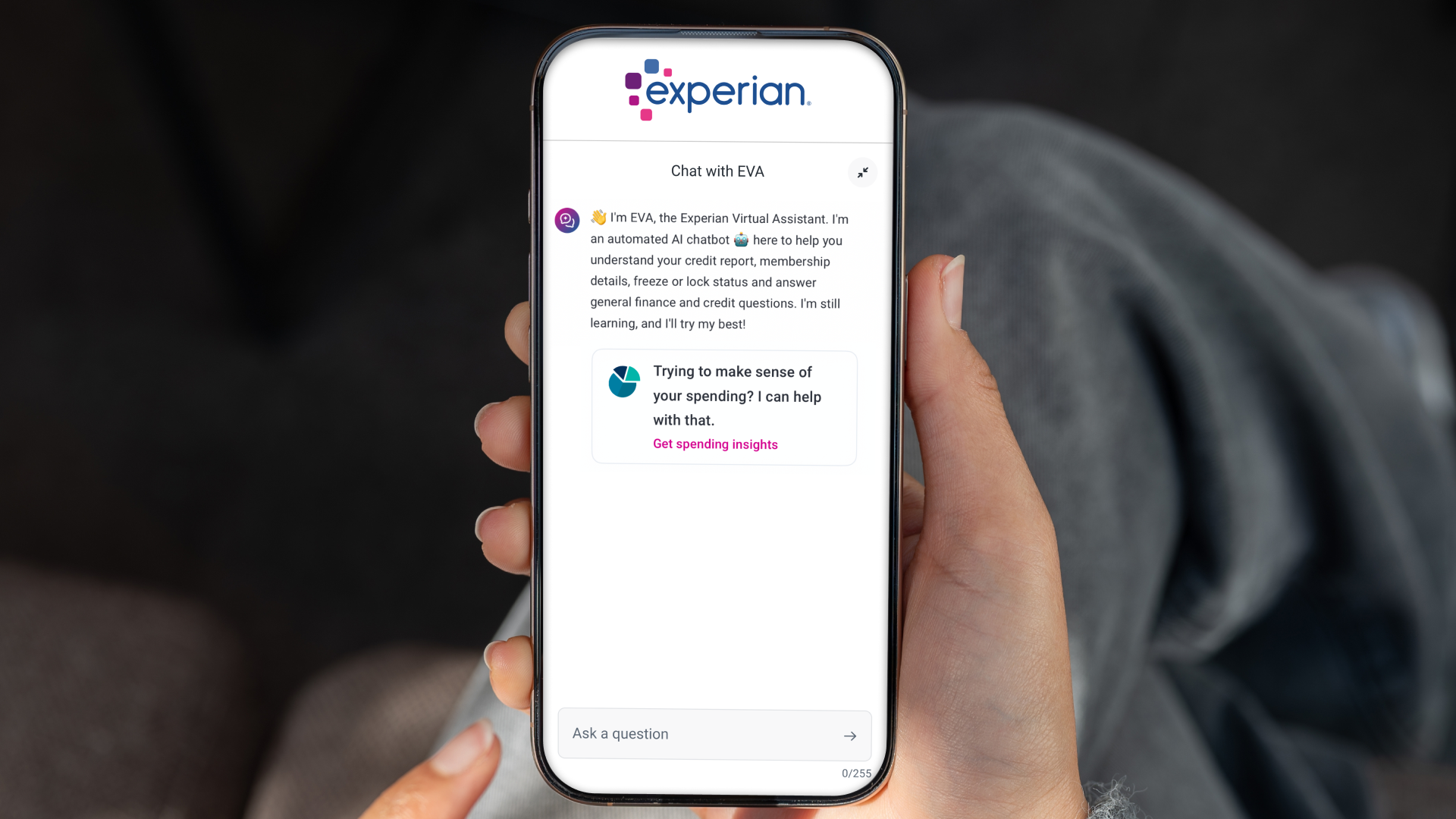

When I began my career as a software engineer, I was captivated by solving problems with code and creativity. Over time, I realized what energized me most was not just the technology, but the people it serves. I wanted to understand why I was building something and see its real-world impact. That perspective led me to product management, where I could combine technology, empathy, and innovation to solve meaningful problems for consumers. At Experian, that mindset shapes what we call our Consumer First AI strategy. Consumer First AI means meeting people where they are in their financial journey. Some are building credit for the first time. Others are recovering from setbacks. Many are exploring new opportunities, planning for major milestones, or working toward long-term goals. Each person’s path is different. Consumer First AI is about using technology not just to provide information, but to guide consumers with clarity and relevance based on what they are seeking in that moment. One of the most powerful examples of that work is the evolution of EVA, the Experian Virtual Assistant™, and how it brings Consumer First AI to life. EVA began as a simple tool to help consumers get quick answers about their credit. Today, it is far more adaptive and intelligent. Powered by advanced artificial intelligence and grounded in Experian’s trusted data expertise, consumer-permissioned financial information and built-in privacy and security guardrails, EVA is available to deliver personalized conversational financial guidance designed to help members make informed decisions. From Insights to Action At its core, EVA makes financial information accessible and actionable. Experian members can ask questions, receive personalized financial insights, and potentially take action in real time. Whether freezing or unfreezing their Experian credit file, managing membership features, or exploring tailored offers via third-party lenders in Experian Marketplace, they can do it within a seamless conversational experience designed to simplify decisions. Our latest evolution expands beyond credit insights to provide clearer visibility into spending and cash flow. Through connected permissioned financial accounts, members can track spending trends, recurring expenses, and changes over time. EVA also can deliver tailored recommendations to help reduce unnecessary spending, manage subscriptions, and better plan for monthly obligations. By translating complex financial data into practical next steps, EVA serves as an intelligent financial copilot. It helps people move from insight to action with confidence and supports smarter budgeting, saving, and borrowing decisions aligned with their goals and financial priorities. A Mission That Is Personal This mission is deeply personal to me. I was born in the United States but spent my formative years in Taiwan, where credit was not part of everyday life. When I returned to the United States for college, I realized that being financially responsible did not automatically translate into having a strong credit profile. I was fortunate that credit did not stand in my way, but that uncertainty stayed with me and shaped my perspective. That experience fuels my passion for building tools like EVA. Financial health shapes where we live, what we can plan for, and how secure we feel. Yet managing money and credit can still feel complex or intimidating. EVA helps cut through that complexity by meeting people where they are and adapting in real time to their needs with guidance that feels clear and relevant. Consumer First AI in Action At Experian, our mission is bringing Financial Power to All™. EVA represents Consumer First AI in action by combining advanced artificial intelligence, human centered design, and a trusted data foundation to expand access to personalized financial tools and support greater financial inclusion. This milestone builds on our broader strategy to embed intelligent, trusted AI across the consumer ecosystem. Through continued advancements in EVA’s adaptive financial guidance and the launch of Experian Insurance Marketplace integrate with the ChatGPT platform, we are meeting consumers wherever they are with personalized insights and relevant financial opportunities delivered through conversational experiences. EVA is more than technology. It is a Big Financial Friend, or BFF, and a meaningful step toward making personalized financial information accessible, intuitive, and empowering for millions of Experian members. EVA provides general information and educational insights only. It is not a financial advisor and does not provide personalized investment, legal, tax, or accounting advice, nor does it establish any advisor-client or fiduciary relationship. Any financial offers displayed are provided by third-party lenders and are subject to the lenders’ eligibility and approval processes. Users should consult a qualified, licensed professional for personalized advice. Experian’s AI tools operate under internal governance, testing, and privacy controls designed to promote accuracy, fairness, and consumer protection. ChatGPT is a trademark of OpenAI. The Experian Insurance Marketplace app is developed and operated by Experian and is not affiliated with or endorsed by OpenAI.

Identity is the cornerstone of trust. Trust allows businesses to grow and consumers to transact with confidence. It also enables digital ecosystems to function at scale. As AI becomes an active participant in every digital interaction, earning and protecting that trust has never been more critical. To build trust, companies need to recognize the people they’re interacting with online and distinguish good customers from fraudsters. Businesses look to Experian for our extensive consumer data, analytics, and decisioning solutions so they can more confidently identify, authenticate, and engage customers across digital channels. This week, we are accelerating that mission with the acquisition of AtData, a global leader in email-based identity intelligence. Email remains one of the most enduring and widely used digital identifiers. AtData brings real-time intelligence on more than 10 billion email addresses worldwide, adding a powerful and highly predictive signal to Experian’s identity and fraud platform. In a landscape shaped by automation and generative AI, the ability to assess email risk in real time can be a key asset in underwriting trust. Identity Powered by Real‑Time Email Intelligence AtData’s email intelligence provides signals such as domain reputation, account tenure, and behavioral risk to help distinguish legitimate customers from synthetic or manipulated identities. These signals can provide a better experience for good consumers, while supporting earlier detection of first-party fraud, third-party fraud, and synthetic identity schemes before losses occur. Going forward, email intelligence will play an important role in the next generation of Experian solutions, including agentic AI systems that can reason, adapt, and act on trusted identity signals in real time. When combined with Experian’s device intelligence, behavioral analytics, and advanced decisioning capabilities, these insights enable organizations to: Identify and authenticate consumers with greater confidence Detect fraud earlier with improved precision and speed Enhance engagement through richer, more connected identity profiles With AtData, we are not only expanding our data assets, we are also advancing a future where identity is more trusted. I’m excited to build upon our world-class identity and fraud solutions together.

For decades, Experian has invested in building one of the most trusted, differentiated data foundations in the world. Experian’s data helps businesses responsibly engage with consumers, manage risk, and grow with confidence. For consumers, these insights drive improved access to affordable credit solutions in some of the most significant moments of their lives. Our focus on building a durable data foundation and persistent identity signals puts Experian in a unique position, especially as technology continues to evolve, and AI reshapes how decisions are made. Incomplete or inconsistent data can lead to bad models and negative outcomes for both businesses and consumers. And, as data and identity signals continue to change, persistence becomes increasingly valuable. Businesses need confidence that the people they’re interacting with are real, reachable, and consistent over time. That’s why we’re excited to announce Experian’s acquisition of AtData – a leading data and intelligence company backed by the world’s most comprehensive email insights technology. AtData’s coverage of real-time email insights, including over 10 billion email addresses worldwide and 98% of active emails in North America, is trusted by thousands of businesses including many of America’s most notable brands and Fortune 500 companies. Our acquisition of AtData builds on our leading, durable identity infrastructure. By adding the most comprehensive email intelligence technology to Experian’s existing identity, data, analytics, and decisioning capabilities, we’re enabling our clients to make faster, more confident, signal-driven decisions. Smarter, more efficient marketing Email remains one of the most direct and effective channels for driving consumer response — and the intelligence behind it is what separates high-performing programs from inefficient ones. Real-time behavioral signals, including engagement, activity frequency, and responsiveness, tell businesses not just whether an address is deliverable, but whether a person is actively reachable and likely to act. Layering these signals across Experian's existing consumer intelligence enables smarter audience prioritization, reduced waste, and better results across the customer journey. Connecting identity across channels and touchpoints The email address has become the center point of modern, digital identity — an anchor linking the signals a person leaves across the digital and physical world, including postal addresses, phone numbers, devices, and more. Adding email-based identity linkages to Experian's robust identity infrastructure gives businesses a more complete, accurate, and durable view of who a person actually is, across channels in an increasingly fragmented identity ecosystem. Stronger fraud prevention and risk management Email behavior is a critical element in helping businesses detect and prevent fraud. Knowing whether an email is newly created, exhibiting bot-like patterns, or inconsistent with other points of identity associated with a person helps businesses identify synthetic identities and separate trusted from higher-risk activity — earlier in the process. These signals sharpen the decisioning capabilities businesses need to act with speed and confidence. Why this matters now AI is raising the bar for speed, personalization, and precision. But AI is only as effective as the data behind it. In this next phase, trusted, differentiated data is what creates real advantage. AtData strengthens our ability to help our clients navigate what comes next — with confidence and at scale. To learn more about AtData, please visit https://atdata.com/.

We believe financial decisions should feel empowering, not overwhelming. Choosing how to protect your family, planning your next move, building your future, these are personal milestones. Yet too often, the tools meant to help consumers navigate them create friction instead of clarity. We are changing that. Our Consumer-First AI strategy starts with a simple belief: technology should make life easier for people. We’re building AI-powered experiences that meet consumers where they are, cut through complexity, and provide guidance that feels intuitive, supportive, and genuinely helpful. Reimagining Insurance Shopping Through Conversation One example is the launch of our Experian Insurance Marketplace, a leading platform to find and compare auto insurance rates[i], within ChatGPT. Shopping for insurance has long been a frustrating process. Consumers jump from site to site, repeatedly entering information and trying to decode policy differences, often still unsure if they found the right coverage at the right price. Now the experience can begin with a simple question inside ChatGPT. Consumers now can start their journey with Experian and compare estimated rates from more than 35 leading insurance carriers in our network, receive clear coverage explanations, ask follow-up questions in real time, and seamlessly transition into the Experian experience to explore personalized savings and switch carriers. What once took hours across multiple websites can now begin in one guided interaction. Powered by Experian’s Innovation Engine This experience is powered by Experian’s Insurance Marketplace platform and built on years of data expertise, advanced analytics, and strong carrier relationships. It reflects our ability to combine trusted data with emerging AI to create entirely new consumer experiences. For example, consumers can start with a ZIP code to explore price comparisons and, if they choose transition securely to Experian’s website for a personalized quote. This is Consumer-First AI in action. It is not technology for its own sake, but innovation designed to make life easier, build confidence, and give people greater control over their financial journey. Just the Beginning Experian has long helped people build credit, protect their identity, and improve their financial health. Bringing other capabilities, we offer like insurance into conversational AI is a natural extension of that mission. Insurance is only the start in seeing Experian via other platforms. As AI becomes a bigger part of our financial lives, we will continue expanding solutions both within our ecosystem and in other properties like ChatGPT that simplify complex moments and deliver smarter, more personalized guidance wherever consumers are or prefer to engage. Because at Experian, we are committed to being your BFF, your Big Financial Friend, showing up with trusted guidance, practical tools, and support exactly when it matters most. To explore the Experian Insurance Marketplace within ChatGPT or learn more, visit www.experian.com/insurance Insurance products are offered through Gabi Personal Insurance Agency, Inc., d/b/a Experian Insurance Services, a licensed insurance agency. Availability and savings vary by state. Savings are not guaranteed. For license information, visit https://www.experian.com/help/insurance-licenses-disclosure/ [i] Results will vary and some may not see savings.

At Experian, we believe that every individual deserves to feel valued, respected, and supported to thrive. We are dedicated to fostering a workplace where people can bring their full identities to work. This commitment extends beyond any single initiative; it is embedded in how we show up for one another and in how we build a culture where all employees feel seen, heard, and supported. We are pleased that for the seventh consecutive year, our people-first approach has earned us a top score on the Human Rights Campaign Foundation’s Corporate Equality Index (CEI), securing our place on the Equality 100 list for LGBTQ+ workplace inclusion. This honor comes on the heels of winning Out & Equal’s 2025 Outie award for Workplace Excellence and Belonging, and reaffirms our efforts for a workplace that embraces inclusion. Ally is a verb, not just a noun, at Experian. Our Experian Pride Employee Resource Group created an allyship training for all employees and a Parents Group to provide resources to parents, caregivers and family members so they can better support LGBTQ+ youth and family. New this year is our updated bereavement leave policy that acknowledges chosen family, which honors the experiences of many individuals in the community. As Experian Chief Sustainability Officer Abigail Lovell says, “The world works best when everyone gets to live as they truly are.” At Experian, we remain dedicated to making that a reality. Learn more about Experian ‘s commitment to inclusion and belonging in its 2025 Power of YOU Reports: English | Portuguese | Spanish

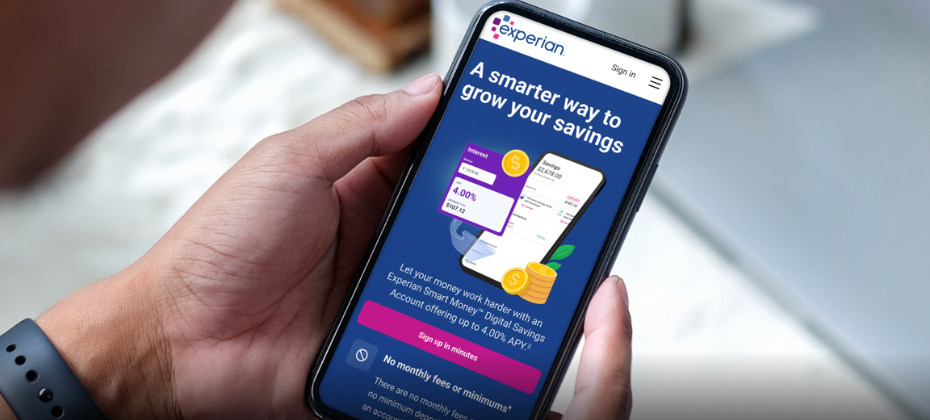

We’re starting the year strong by reaffirming our promise to empower consumers on their financial journeys. At Experian, everything we do is driven by our mission to bring Financial Power to All™—helping people not only understand where they stand but confidently move forward. That’s why I’m pleased to introduce the new high-yield Experian Smart Money™ Digital Savings Account[1], designed to make saving effortless, accessible, and more meaningful than ever before. This new offering is more than just a savings account—it represents an important evolution in how Experian supports financial progress. For years, we’ve helped tens of millions of consumers monitor their credit, improve their credit scores, and protect their identities. Now, by adding a high-yield digital savings account to our existing suite of financial health tools, we’re able to anchor that progress to something tangible: real balances and real momentum. With the ability to save built directly into the Experian ecosystem, members can track their savings growth alongside credit improvements, creating a clearer picture of their overall financial health. Positive financial behaviors—like paying down debt, making on-time payments, or improving utilization—can now be experienced in parallel with cash accumulation and stronger financial resilience, all in one trusted place. The Experian Smart Money™ Digital Savings Account offers up to 4.00% variable Annual Percentage Yield[2] (APY), which is nearly 10 times the national average savings rate[3], with no minimum balance or direct deposit requirement. It’s seamlessly integrated into the Experian membership experience, making it easier for consumers to take action the moment insight appears. This launch builds on the success of our Experian Smart Money™ Digital Checking Account & Debit Card introduced in 2023 and reflects our continued commitment to creating products that meet consumers wherever they are on their financial journey. We believe saving is a foundational financial behavior—and one that plays a powerful, often underappreciated role in credit outcomes. Strong credit health isn’t just about borrowing; it’s closely tied to liquidity, cash flow stability, and financial resilience. Having accessible savings can help consumers stay current on bills during income disruptions, build buffers that reduce reliance on higher-cost credit, and create flexibility that can support long-term credit improvement. In this way, a high-yield digital savings account becomes more than a place to store money—it becomes a practical tool for building healthier financial habits. Whether it’s emergency savings, goal-based saving, or smoothing cash flow, an Experian Smart Money Digital Savings Account enables consumers to turn good intentions into consistent action. This launch also reflects our broader evolution beyond a traditional credit bureau. Today, Experian membership provides access to credit monitoring and improvement tools, identity protection, a credit card marketplace, auto insurance comparison shopping, and personalized guidance through our AI-powered virtual assistant, EVA. Adding a high-yield digital savings account allows us to take the next step with our members—bridging the gap between insight and action. Instead of stopping at “here’s where you stand,” Experian can now help consumers actively build positive financial momentum. We’re extending our role as consumers’ BFF—Big Financial Friend—by making it easier to save, plan, and grow within the same ecosystem they already trust. By innovating and delivering products that truly make a difference in people’s everyday financial lives, we’re continuing to advance our mission and help consumers turn knowledge into progress. Learn more at experian.com/smartmoney. [1] The Experian Smart Money™ Debit Card is issued by Community Federal Savings Bank (CFSB), pursuant to a license from Mastercard International. Banking services provided by CFSB, Member FDIC. Experian is a Program Manager, not a bank. See Experian.com/legal. [2] The Annual Percentage Yield (APY) is 2.00%, 3.00% or 4.00% as of today’s date based on the Experian membership status. The APY may change at any time before or after your account is opened. Changes to the Experian membership can impact the APY, interest rate, and features. The interest rate and APY may be lower during membership trial periods. No minimum deposit to open account. Balance must be at least $0.01 to earn APY. Learn more. [3] As of Dec. 15, 2025, the national average rate for savings accounts was 0.39%, according to the FDIC.

As the AI-enabled speed of data analytics and model development continues to accelerate across financial services, financial institutions face a growing challenge: keeping regulatory documentation aligned with rapid model innovation. Experian Assistant for Model Risk Management was built to address this challenge, and we’re proud it has been named a 2026 BIG Innovation Award winner in the Innovative Products category. The BIG Innovation Awards recognize organizations that deliver exceptional innovation and measurable value to customers and stakeholders. This recognition underscores the impact our AI-powered solution is having in helping financial institutions modernize model risk management in today’s AI-driven environment. Accelerating model validation and reducing regulatory risk Fully integrated into the Experian Ascend Platform™ and powered by ValidMind technology, Experian Assistant for Model Risk Management helps accelerate model validation, improve auditability and reduce regulatory risk. By offering standardized templates, centralized documentation and streamlined workflow approvals, the solution supports regulatory alignment while enabling faster, more consistent model development. As AI-driven models evolve at unprecedented speed, regulatory expectations continue to require thorough, explainable and auditable documentation. Experian Assistant for Model Risk Management addresses this labor- and resource-intensive requirement through end-to-end model documentation automation, helping institutions maintain accountability without slowing innovation. Addressing a growing industry challenge According to a 2025 Experian study of more than 500 global financial institutions, 67% struggle to meet regulatory requirements, 79% report more frequent supervisory communications, and 60% still rely entirely on manual compliance processes. More than 70% of larger institutions say model documentation compliance involves over 50 people. Experian Assistant for Model Risk Management helps solve this challenge by modernizing model documentation and governance practices across the credit and risk lifecycle. The 2026 BIG Innovation Award reinforces Experian’s role as a trusted partner, helping financial institutions confidently adopt AI while improving transparency, auditability and regulatory alignment. Learn more about Experian Assistant for Model Risk Management here.

The last several months stand out as one of the most dynamic periods in my career. To say it’s been an exciting time would be an understatement. For more than 20 years, the mortgage industry has relied on a single way to measure creditworthiness. With the Federal Housing Finance Agency’s decision to approve VantageScore 4.0 for use in mortgage decisions, that long-standing approach is evolving. At Experian, we’ve advocated for score choice in mortgage from the very beginning. We believe in modern scores because they allow more of Experian’s rich, differentiated data to be used in lending decisions. Because this data provides a more complete picture of a consumer’s financial health, it creates new opportunities to expand access to homeownership. At the same time, significant change naturally brings questions and debate. New models. New data sources. New decisions to make. New ways of doing things. Across the industry, there’s been a lot of discussion about what these changes mean in practice, how they impact lenders and consumers, and how the industry moves forward from here. I recently had the opportunity to talk through many of these topics with Robbie Chrisman on the Chrisman Commentary Daily Mortgage News Podcast. Our conversation focused on bringing clarity to some of the most common questions I’m hearing today, while also looking ahead to the opportunity in front of us: modernizing mortgage decisions in a way that reflects how consumers actually live and manage money to help more consumers realize their dreams of homeownership. We discuss the fundamentals, including the difference between credit reports and scores (and why that distinction matters), how expanded data, including things like rental data, cash flow insights and buy now, pay later information, can help lenders make more informed decisions and how we can help turn today’s renters into tomorrow’s homeowners. We separate fact from fiction on credit report pricing and we take a forward look at where we can, collectively as an industry, go from here. The good news is: Consumers haven’t stopped believing in homeownership. Our systems just need to continue evolving to reflect the way people live and manage money today. With better data and more modern tools, we are moving in the right direction. To hear more, listen to my full conversation with Robbie Chrisman on the Chrisman Commentary Daily Mortgage News Podcast.