Topics

When a new customer wants to establish credit terms with you, the first thing they’re asked to do is fill out your credit application. When you hand over a paper application, did you know you could be negatively impacting your revenue or creating a poor customer experience? Some companies don’t. More than likely, your customer has filled out at least one digital application in the past. The initial perception your application says about your company is that you’re out of step with technology — which may lead them to wonder where else you may be lagging behind. Digital applications provide a simplicity factor, and by not offering one, your credit approval process is perceived to be more difficult, leaving the customer with more work to do —spending extra time writing their information by hand and returning the application — either by email, fax, or in person. Because many companies have already moved to a digital application, your pen-and-paper process sticks out to the customer — and not in a good way. Not to mention, manually processing a paper application takes longer — often much longer — than a digital application. This means customers leave without a credit approval, giving them time to change their mind about their purchase or find a better deal — meaning you just lost a new sale. And even if they still choose to work with you, their relationship with your company starts out with a less-than-amazing customer experience. After the paper application is completed, the workflow process is often time-consuming, error-prone, and cumbersome. The time involved also means that your company waits longer to receive revenue from the sale. By using a manual process, your team spends hours on processing and decisions that could be better spent directly servicing customers or working on other initiatives to grow business. DecisionIQ from Experian automates consistent real-time decisions, streamlining your entire process from applications to onboarding.

For lenders, alternative data can be the factor in edging out your competitors, especially when better decisions are needed to compete for emerging businesses and startups. Both startups and emerging businesses may represent a good growth opportunity, but they may also be high risk. The challenge? Businesses with thin credit profiles can be difficult to score. Social Media Insight TM provides lenders with another layer of data that can help you better assess the direction of these businesses, score them more accurately and open new growth opportunities. After all, nobody likes to leave money on the table. For emerging businesses who have a thin credit profile but have a strong social media reputation, Social Media Insight can be a factor in gaining access to credit and resources they deserve. Social Media Insight enables you to see the activity, trends and sentiment on a business, over time. In our Experian DataLab tests, we improved overall model performance by 12 percent and new and emerging businesses by 91 percent, boosting predictive performance over traditional data sets. Social Media Insight is directly sourced data providing you with over 70 attributes including trends and sentiment along with descriptive attributes. This powerful data enables you to more accurately score or assess new and emerging business as well as long established accounts. Want to learn more? Watch our on-demand webinar or contact your Experian representative today.

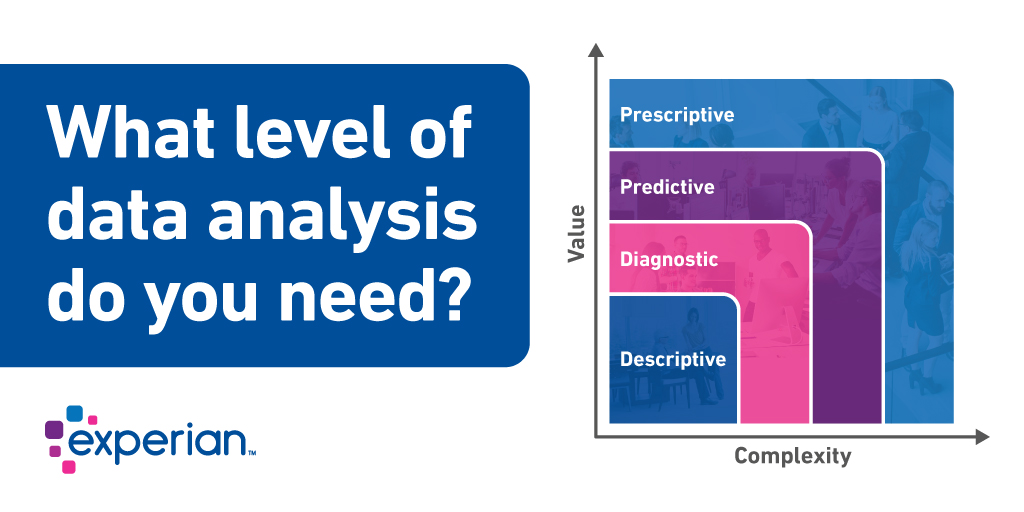

Data analysis surrounding lending practices for commercial lenders falls into 4 distinct buckets that define scope, usability, and purpose. In this post we will discuss how they differ in terms of value and complexity. Descriptive Analytics Descriptive analytics provide the current state of a commercial lender’s acquisitions, portfolio, or other parts of the lending lifecycle. This is “Reporting” in its simplest form. Defining and creating metrics can be as simple as a snapshot of the firmographic and performance elements of a portfolio to complex retro trends that define the effectiveness and success of a lender. Full coverage of the target market and accurate data play a big part in the success of this type of analysis. Selecting the wrong element, when creating a view, can lead the lender to a sub-optimal understanding of the state of their business. Looking at a competitor’s metrics can inform market share and pricing decisions. Experian commercial clients use Portfolio Benchmarking reports as an empirical view into the health of their business compared to their market peers. Adding data visualization on top of the descriptive-analytic reporting quickly closes the gap to a diagnosis. In the map below Texas, California, and Florida have higher rates of account opening and would be attractive target regions for acquisition. Diagnostic Analytics A Diagnostic view of lending performance will look at the portfolio health of a lender and its peers and determine what are the key success and opportunity drivers within comparable products. Larger financial institutions have been performing this type of analysis for years. Several years ago, fintech lending hit its stride challenging the large commercial lenders by providing targeted products in niche lending spaces with little or no traditional commercial credit data. Large commercial lenders used benchmarking and market analysis to understand where the fintechs were being successful. Large lenders use of alternative data sources and market intelligence helped them to recognize the gaps in identifying and evaluating the risk of those underserved businesses. Fintech use diagnostic analysis, to their advantage, to make fast decisions and pivot to market demand. In the chart above, you can see that ABC bank is able to identify where they are offering higher credit limits than their competitors. This client had similar bad rates to its peers causing the lender to have higher losses due to improperly assigned credit limits. Predictive Analytics Predictive analytics can help to scope the effectiveness of a strategic decision and plan for the long-term impacts of credit decisions. Financial institution use this type of analysis to forecast loan performance and plan for impacts to cash flow as economic and market conditions change. Machine learning is used in predictive analysis to be nimbler in the evaluation of vast amounts of data to provide more accurate prediction of future outcomes. Large financial institutions will use Machine Learning in predicting response to an offer through the lifecycle to the collection of outstanding debt. Prescriptive Analytics Predicting potential outcomes within a commercial lender’s strategies only gets them half way to a successful outcome. Providing insight on top of the analytic content is what drives the decisions to stay the course or pivot to an alternate course of action. Prescriptive analytics provides that direction. Machine learning can be used as a tool in prescriptive analytic engagements to develop models that can learn and pivot with changes to the market and behaviors of businesses within that market. Having the capability to adjust actions associated with outcomes allows the model to stay relevant and predictive over a longer period. As customer experience drives lending practices, commercial lenders look to use varying levels of analysis as stepping stones to better serve their small business clients. Got a question about analytics? We would be delighted to answer your questions. Commercial Data Science

All business customers are not created equal. Even companies that look solid at first glance can hide festering problems that eventually can impact your bottom line. Successful credit management requires you to carefully evaluate the financial health of every business that asks for credit terms. Here are 5 questions you should be able to answer before extending business credit: 1. Is the business what it claims to be? Sometimes, companies needing credit will provide inaccurate information to win approval. Before opening an account, you need to confirm the applicant‘s bona fides, including its location, size, number of employees, annual revenue, years of operation and similar financial indicators. 2. What is its payment history? Although past performance does not guarantee future results, a company’s payment history is often a strong indicator of how it is likely to behave in the future. Pulling a business' credit report can easily provide you a snapshot of a company's payment history as well as other risk measures. 3. Are there hidden factors that could affect its ability to pay? Are there pending judgments, lawsuits, bankruptcies, regulatory citations or other “red flags” that could make it difficult for the applicant to meet its obligations in the future? This is another area where a business' credit report will be a key factor in helping you uncover a potentially risky business. 4. How much credit should you extend? All credit contains an element of risk, but you can mitigate that risk by limiting the amount of credit you extend based on factors such as the customer’s sales volume, debt to-asset ratio and similar aspects. 5. Under what terms should you extend credit to this customer? You can mitigate risk further by carefully calibrating the combination of interest rates, minimum payments and other contract terms based on each customer’s individual financial metrics.

You likely go to great lengths to protect your own identity from fraud and theft. But are you actively protecting your business’s identity as well? Even more importantly, do you make sure you are not doing business with fraudulent companies that have been victims of identity theft themselves? In many ways it’s harder to protect your business identity than your consumer identity. Information about most businesses is publicly available – and as easy to find as a simple Google search. Because businesses self-report much of their own information, it’s easy for a thief to add their name or address to a company. To make it even easier, many businesses do not protect their EIN the same way as they secure their SSN – which they should. At first glance, you may think having your personal identity stolen to be more damaging than a business identity. But in fact, the opposite is often true. Business owners often personally guarantee loans, even if the loan turns out to be fraudulent. And then if a business must close its doors due to the losses from the theft, the business owner now has no income and must repay the loan. How Business Identity Theft Happens Some thieves steal business identities by purchasing a shell corporation. Others take over a company’s data. But regardless of how the left happens, the criminals often go to great lengths to mirror the company. Some even rent space in the same building as the original company and using the same suppliers. At this point, the fraudulent company can start physically intercepting deliveries as well as applying for loans and credit, posing as the original company. Criminals start with one piece of information that is real, such as an address or EIN number. And then start operating as if they are the company and changing the data. Criminals often wait patiently while building up their reputation and credit history, then “bust out” with a large amount of fraudulent activity in a short period of time, and then walk away before they are discovered. Protect Your Own Business Identity Business owners must constantly monitor their business information to spot red flags that criminals have taken over. The earlier the theft is discovered, the less damage that occurs. Here are three things to look for to spot business identity theft of your own business: Look for new addresses added. Check your credit reports and government filings to verify the address. One of the first signs of theft is often a new address added to your business information. Verify that new registered owners have not been added. Thieves will often add a new principal — CEO, owner or partner — to the list of owners. The criminals can then conduct business as if they are an owner. Check business accounts daily. Use online banking — which also reduces the risk of stolen paper statements — to look for any transactions that you or your employees did not make. Consider setting mobile alerts for suspicious transactions to spot issues even faster. Verify Your Customers are Not Fraudulent Companies Before doing business with a company, do a business verification by making sure the company is who they say they are and not a and not a fraudulent company. Since verifications cost time and money, take each customer on a case-by-case basis regarding how deep to dig. If a customer orders $100,000 worth of computer equipment, you should do a more thorough investigation than for a business ordering a single $500 laptop. However, anytime you are extending a line of credit to a company, you should deep dive into a companies' history and data because you are taking on a high risk. Stacking loans is a common tactic – meaning companies take loans from multiple companies at the same time. Because many companies often verify customers by looking at their relationship with the business, they are verifying in a vacuum instead of seeing the entire picture. By using databases and tools that provide a holistic view of all activity, it becomes much easier to find the fraud. Here are five things to look for when verifying a company: Verify the EIN number. One scheme is to use a different EIN number and have all other pieces of information the same. Make sure the company you are doing business with is using the same EIN number as the legitimate company. Consider the number of open lines of credit. Because fraudulent companies often open multiple lines of credit at the same time, determine the current amount of open credit. Multiple large lines opened around the same time can be a red flag. Look at the number of sub-companies and activity between the companies. Criminals often set up a fraud ring by operating as sub companies underneath a single company. The “companies” then loan money to each other to boost credit scores and credibility. Note for periods of dormancy. When a business identity is first stolen, the criminals set up the company and then go dormant to build credibility through age. The company will then “bust out” by making a lot of transactions very quickly with multiple companies. Look for additional addresses. Check to see if the address you have been given is the same as the company’s headquarters. Multiple similar addresses can be a red flag. As business identity theft continues to rise, you must keep your eyes open for signs of theft — both with customers and your own business. A single credit check or google search simply isn’t enough. You owe it to your business and your future.

Scottsdale, Ariz., May 22, 2018 — Experian®, at its 37th annual Vision Conference, today announced it has become a certified vendor of the Small Business Financial Exchange, Inc. (SBFE), a nonprofit trade association that gathers and aggregates small-business payment data in the United States to help organizations build a complete picture of small business. “We’re excited to work with SBFE, which shares our mission to bring further innovation to the small-business credit landscape,” said Hiq Lee, president, Experian Business Information Services. “By combining the SBFE’s data richness with Experian’s vast consumer and commercial data assets and leading data science capabilities, we will use the power of data to help our clients make the right decisions.” As a SBFE Certified Vendor, Experian can combine its rich data — including traditional and alternative business data and consumer data on business owners — with SBFE’s data to provide the most comprehensive view of a small business in the market today. For example, financial institutions looking for broad and deep insights on small and emerging businesses will be able to find that information in a way no one has offered previously. Also for the first time, Experian clients that are nonfinancial institutions, such as e-commerce, communications, insurers, and software and hardware vendors, can qualify to access this financial data to help them make confident credit decisions by gaining deep visibility into a small business’s capital use and credit history through Experian. “Experian becoming an SBFE Certified Vendor makes perfect sense in support of our ongoing mission to serve our Members and the small-business community,” said Carolyn Hardin-Levine, CEO, SBFE. “Experian demonstrated its ability to meet SBFE’s high data security and governance requirements, controls, and independent oversight requirements. Additionally, Experian’s ability to deliver blended solutions combined with SBFE data will provide our Members with more options and drive innovation as part of SBFE’s single-feed, multicertified vendor model.” New product pipeline Experian fosters a culture of continuous innovation, from the way it works to the solutions it creates. The company plans to deploy its data scientists to apply leading-edge techniques, including machine learning and artificial intelligence, to discover and provide predictive insights and analytical tools to support better decisioning for its clients. It is anticipated that the work of its data scientists on the combined data sets will result in new product launches over the next 24 months. Vision Conference Each year, Vision combines in-depth research, cutting-edge technology and expertise from industry leaders to help Experian’s clients strengthen their balance sheets and plan for sustained growth. The 2018 conference sold out and runs May 20–23 in Scottsdale, Ariz. Contact: Jackie Brenne Experian Public Relations 1 714 830 5126 Jackie.Brenne@experian.com About Experian Experian is the world’s leading global information services company. During life’s big moments – from buying a home or a car, to sending a child to college, to growing a business by connecting with new customers – we empower consumers and our clients to manage their data with confidence. We help individuals to take financial control and access financial services, businesses to make smarter decisions and thrive, lenders to lend more responsibly, and organisations to prevent identity fraud and crime. We have 16,500 people operating across 39 countries and every day we’re investing in new technologies, talented people and innovation to help all our clients maximise every opportunity. We are listed on the London Stock Exchange (EXPN) and are a constituent of the FTSE 100 Index. Learn more at www.experianplc.com or visit our global content hub at our global news blog for the latest news and insights from the Group. About SBFE The Small Business Financial Exchange, Inc., and SBFE, LLC (collectively known as SBFE) is the country’s leading source of small-business credit information. Established in 2001, this nonprofit association’s database houses information on more than 32 million businesses and enables information exchange among members who provide small-business financing. Through its resources and relationships, SBFE makes possible innovative risk management solutions by providing industry insight and analysis of aggregated small-business financial data to its Members. SBFE is the only Member-controlled organization of its type and is serving as the most trusted advocate for the safe and secure growth of small business. For more information, visit www.sbfe.org.

Last year the three primary credit bureaus; Experian, Equifax, and TransUnion announced and implemented enhanced standards for the collection and timely updating of public record data reported on consumer credit reports. This was done in accordance with the National Consumer Assistance Plan requirements. Part of this work involved the partial removal of tax lien data from our consumer credit reporting database. With the complete removal of remaining tax lien data scheduled for April 16th, some of our clients have asked how these changes might impact commercial credit reports. In this business Q&A I ask Brodie Oldham for some clarification. What is NCAP and how did it impact Experian's core credit data? Brodie Oldham: Gary the NCAP is the National Consumer Assistance Plan and it was put in place by the three U.S. credit reporting agencies Experian, Equifax and TransUnion in response to the U.S. attorney general's request for clarity and transparency in consumer credit data. The data that was the main focus was data that did not meet completeness or freshness requirements of data furnishers to the credit reporting agencies. The data that had the most impact from the study was public record data; judgments and liens for consumers that weren't updated or didn't have all of the personal identifying data necessary to meet the guidelines. This data is planned to be removed in April of 2018. Was there impact to Experian's commercial credit data? Brodie Oldham: No Gary not an impact to our commercial credit data collected at Experian. We continue to collect that public record information for use in evaluating small businesses through our commercial credit scores. The impact with the public record information is really when we're evaluating a business owner guarantor using the consumer credit information where public record data has been removed. What was the impact to commercial blended scores? Brodie Oldham: The impact is when we're evaluating small business owners or guarantors using their consumer credit information. When we look at segments where commercial-only data is used there is no impact there because we're not changing the way that we collect public record information on the commercial side of our business?With the blended scores you would expect that if we remove some of the consumer derogatory information in public records that the score would go up. And we saw a mean lift to about .03 percent, so very small. In the performance of the blended generic credit scores in their evaluation and capture of those delinquent accounts. We saw a very insignificant lift, so the scores are very stable and working well even with the change that we're having with public records. Additional Resources: Whitepaper - NCAP Impact on BIS Scores (June-2017) National Consumer Assistance Plan Is Extended as Experian, Equifax and TransUnion Settle with State Attorneys General

The lease for the $50,000 office equipment seemed like any other order at first glance. The customer passed the credit check without issues. But when the multinational corporation was unable to collect payment, it dug deeper and realized that the ship-to address was a residence. With more research, the business discovered that its “customer” had used stolen identity information to pass the credit check. Because the company did not use systems to check for fraudulent ship-to addresses, the fraudulent order was unnoticed and the company fell victim to ship-to fraud. Although only a handful of the company’s customer accounts were fraudulent, the company lost a significant amount of money last year because each account included large six-figure deals. What is ship-to fraud? In a ship-to fraud scheme, a criminal poses as a customer and presents a verifiable billing record, address and credit history. Companies often deem these criminals as credit worthy because their records are up to date and they have a good credit history. Often, the first few orders placed are for smaller items and the bills are paid on time, which increases the criminal’s credit limit. The criminal then places a significantly larger item and never pays the bill. Because the shipping address is a location unrelated to the actual business, the criminal can easily pick up the order and sell the goods. While ship-to fraud happens with consumer goods, the impact is typically more significant in the B2B world because the cost of the goods is higher. Also, most consumer goods are paid for before the items ship. However, B2B companies often extend lines of credit to customers or bill at set intervals, which means products are often shipped before payment. Keys to reducing risk Here are five ways you can help prevent B2B ship-to fraud at your company: Review your business application process. Most companies ask for headquarter information when determining the creditworthiness of a new business customer. However, many companies have products shipped to locations other than the headquarters. During the application process, capture all operating locations on the application. This makes it easier to determine which shipments are going to legitimate addresses and those that may be potentially fraudulent. Compare ship-to addresses with all operating location addresses. If a product is being sent to a location that was not listed on the business application as an operating address, there is a risk the purchase is fraudulent. The risk is even higher if there is large physical distance between the ship-to address and the customer’s operating and billing locations. Determine if the ship-to address is a freight forwarder or consolidator. If the ship-to address includes a container number, it is possible that the purchase is fraudulent. Criminals often use freight forwarders and consolidators to receive fraudulent purchases because it creates more anonymity for the fraudster. Check to see if the ship-to address is a P.O. box. Because most businesses don’t use a P.O box for product orders, a P.O. box used as a ship-to address should be a red flag for potential fraud. P.O. boxes are another way criminals anonymously receive purchases. Look up the address on Google. Put the address into Google and see if the business placing the order shows up in the search results. If not, look for these red flags: - A residence – Consider if a home-based business is likely to order the product. - A forwarding or consolidating business – Some of these types of businesses do not use container numbers in the address, which means physical verification is your best protection. - Property for sale – While shipments to properties on the market can be legitimate, this raises concerns because criminals often use vacant buildings as ship-to addresses. View the location on Google Maps. By viewing the photos online, you can get further verification that the address is an actual business. You can often get a feel for the area and see if there are a lot of vacant buildings or other red flags. Be sure to check the data on the photo to see if it was taken relatively recently. Empower employees to escalate potential fraud. Your employees are your first line of defense against ship-to fraud. They are the ones processing the orders, printing the shipping labels and packing the boxes. Train your employees on potential red flags and have a process to handle concerns. Encourage employees to pick up the phone and speak with customers to clarify any concerns about the address. If they aren’t convinced it’s a legitimate order, have a process for the employee to stop the shipment and escalate the issue up the chain of command. Many legitimate businesses and shipments may have a single red flag for ship-to fraud. However, when an order has multiple red flags, you should be especially cautious and delay the shipment until the shipment is proven legitimate. Because manually confirming all ship-to addresses can be time consuming, many businesses are now using automated solutions to flag suspicious orders. Your B2B company can save money and time by using a system to help eliminate ship-to fraud. By waiting to develop a process to prevent this type of fraud, your company risks becoming the next cautionary tale.

So you’ve created the perfect campaign with great creatives and an unbeatable offer. You deploy the campaign and sit on the edge of your seat waiting for all the leads to flood in. After a couple of days, you notice a couple of responses but nowhere near the volume of what you were hoping for, and you’re stuck asking yourself “why?” Here are a couple of hypotheses: 1.) the people you reached out to aren’t the right audience so they don’t care about your offer, or 2.) your target audience didn’t see your efforts because you used the wrong channel. The process of finding new business customers can be expensive and sometimes unpredictable, but it doesn’t have to be. Here are 3 tips to help improve your prospecting efforts: Tip #1: Define your ideal customer One of the most fundamental ways you can help grow your current customer base is to have a clear understanding of what they actually look like (or defining what they should look like). What’s their job title? What are their biggest business challenges? Are they web savvy? How do they prefer to get industry news? Addressing discovery questions like these allows you to better understand who you’re talking to and how to talk to them. Additionally, you’ll be able to use this profile to help you mimic your best customers and target look-a-likes. Tip #2: Target new businesses Get your products/services in front of new businesses before your competitors. Not surprisingly, many marketers overlook targeting new businesses because of the lack of data -- how do you know a new company is in business? How do you know if they’re the right business for you to even target? Fortunately, there are many services in today's market that can help fill in the gaps. Using something like Experian’s US Business Database, which is a database of more than 16 million active U.S. companies, can help you discover new businesses sooner and beat out your competitors to reach them first. Tip #3: Find the decision-makers Identifying the right businesses to target is important, but ensuring that your offer gets in front of the right person – the decision maker – is even better. By finding the decision maker and directing your marketing efforts towards them, you can rest assure that your message lands in the hands of the person that matters most. Want to take it one step further? Once you know who you’re talking to, you can tailor the message and offer to be more relevant for that specific audience, which ultimately helps increase your chances of getting a response. Finding and reaching new business customers can be a daunting and expensive tasks, especially if you don’t target your prospecting efforts. Be sure to keep these tips in mind when approaching your marketing strategy and don’t let today’s data challenges hold you back. Learn more about Experian's US Business Database or our other marketing capabilities.