Experian Commercial Pulse Report | 4/8/2025

Experian has released our April 8th Commercial Pulse Report. As the U.S. economy moves through a phase of recalibration, this week’s Experian Commercial Pulse Report highlights one area in particular that’s undergoing notable change—the labor market.

Watch Our Commercial Pulse Update

Macroeconomic Highlights

Inflation eased to 2.8% in February, while job growth remained solid with 228,000 new jobs added in March. Unemployment rose slightly to 4.2%, and consumer sentiment dropped to 57.0—the lowest since late 2022. Despite rising wages, economic uncertainty is growing, reflected in cautious optimism among small businesses.

The U.S. Labor Market Presents a Paradox for Business Owners

While macroeconomic indicators show some signs of resilience—such as moderate job growth and easing inflation—recent research zeroes in on the evolving dynamics between workers and employers. For small businesses navigating talent shortages, shifting workforce expectations, and rising labor costs, understanding these trends is critical.

High Satisfaction, But Growing Uncertainty

Despite concerns about a slowing job market, job satisfaction among American workers remains high. According to a recent Pew survey featured in the report, only 12 percent of workers report dissatisfaction with their current jobs. However, 25 percent say they’re likely to look for a new role in the coming months. This disconnect suggests that workers, while content, are watching the labor market closely and weighing their options—especially as job openings become harder to come by and hiring slows across several sectors.

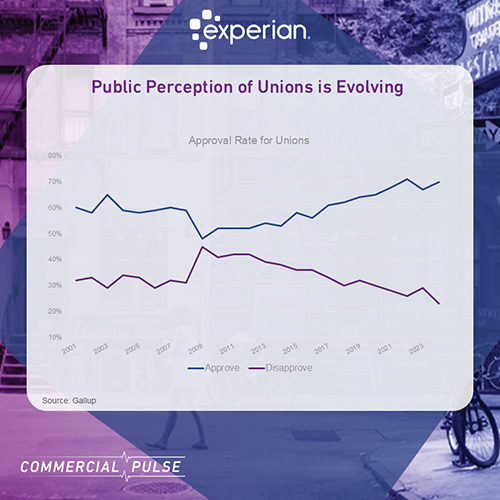

Unionization: Fading Membership, Rising Support

Union membership has steadily declined for decades, now representing just 9.9% of the U.S. workforce or about 14.3 million workers. Yet paradoxically, public support for unions is rising, particularly among younger employees. A Gallup survey cited in the report found that over 70% of Americans now approve of unions. While many remain undecided about joining, younger workers are increasingly labeled as “union curious”—interested in collective action but unsure of the long-term implications. At the same time, older employees are dominating union rolls, with workers aged 55 and over now making up 24.3% of union members—a nearly 80% increase from 2000.

The Business Impact of Unionization

For employers, particularly small businesses, these shifting sentiments present new challenges. Unionization can drive up payroll and benefits costs, slow down decision-making, and foster adversarial dynamics between leadership and employees. The report also highlights that union-heavy environments often experience higher operating costs and reduced managerial flexibility—factors that can be especially burdensome for resource-strapped small businesses.

However, the rise in union interest can’t be ignored. In today’s competitive labor landscape, addressing employee concerns proactively—particularly around compensation, benefits, and workplace culture—may help business owners retain talent and avoid labor disputes.

Why This Matters Now

These labor market dynamics are unfolding at a time when small business optimism, while slightly improving, remains cautious. The Experian Small Business Index rose to 45.4 in February—its second monthly increase—suggesting that while owners are willing to invest in their businesses, they remain watchful of economic uncertainty and evolving workforce demands. Download this week’s report for more insights on the evolving labor market and more.

To stay ahead of the latest trends:

✔ Visit our Commercial Insights Hub for in-depth reports and expert analysis.

✔ Subscribe to our YouTube channel for regular updates on small business trends.

✔ Connect with your Experian account team to explore how data-driven insights can help your business grow.

Want to learn more? Download the full Commercial Pulse Report for April 8th, 2025.

Related Posts

Experian takes a snapshot of the Construction Industry before the effects of the 21st Century ROAD to Housing Act take hold.

Small business lending is evolving. Experian uncovers who’s being left out and where the biggest commercial credit opportunities are hiding.

Discover key Leisure & Hospitality trends, including 181% growth in credit inquiries, record travel demand, and insights for risk leaders.