Experian and Moody’s Analytics have just released the Q2 2020 Main Street Report. The report brings deep insight into the overall financial well-being of the small-business landscape, as well as offer commentary on business credit trends, and what they mean for lenders and small-businesses.

Small businesses have turned to borrowing to survive periods of prolonged slumping sales, in many cases from government programs offering loan forgiveness. This increased borrowing has masked rising delinquent balances, but such a solution is a short-term fix. To keep their credit current, small businesses will need to find ways to generate revenue. Defaults are expected to rise in coming quarters as forbearance programs expire and as customers are likely to change their priorities in the wake of COVID-19.

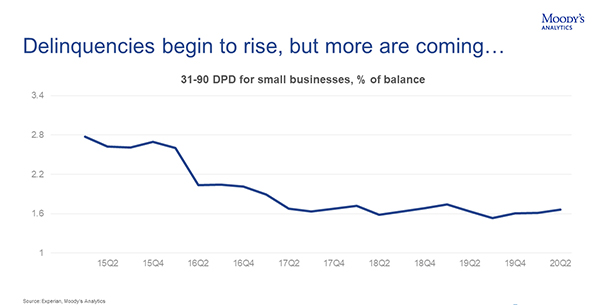

In Q2, moderate delinquency, defined as 31-90 days past due, rose to 1.66 percent from 1.61 percent, marking the fourth consecutive quarter of increasing delinquency, and the first year-over-year increase since this time last year.

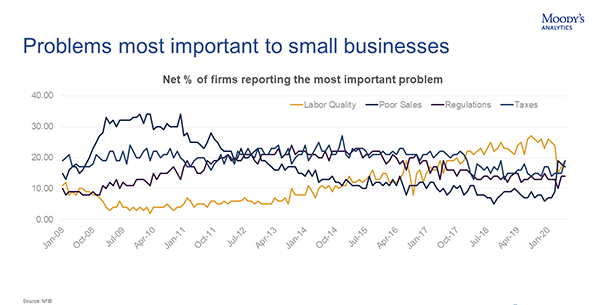

The closure of many state and local economies in April and the first half of May left many businesses facing severe revenue shortfalls in the second quarter. This environment has resulted in businesses listing poor sales as the second most important problem facing small businesses, according to the NFIB.

If you would like to get the full analysis of the data behind the latest Main Street Report, presented by leading economists from Moody’s Analytics and Experian, watch the Quarterly Business Credit Review webinar.