At A Glance

Psympl explains how psychographic data improves financial marketing by revealing consumer motivations. This Q&A covers how tools like the Consumer Console™ and Psymplifier™ help financial institutions target, engage, and retain customers during the Great Wealth Transfer. The interview ends with practical steps for starting psychographic segmentation.In our Ask the Expert series, we interview leaders from our partner organizations who are helping lead their brands to new heights in AdTech. Today’s interview is with Brent Walker, Co-Founder and Chief Strategy Officer at Psympl.

What value does psychographic data add to financial marketing?

Demographic data tells financial marketers WHO a consumer is (like age, gender, or income), but it doesn’t predict decisions. Behavioral data shows WHAT a consumer does, but people can take the same action for different reasons. Understanding these reasons helps marketers engage consumers more effectively.

Psychographics reveal people’s attitudes, values, lifestyles, and personalities, the core of their motivations. This layer helps marketers understand WHY people act, anticipate needs, and connect in more meaningful ways.

This matters now as the “Great Wealth Transfer” unfolds: $124 trillion will be transferred from older to younger generations by the 2040s. Psychographics vary widely across generations, and up to 80% of heirs may switch financial institutions.

Using psychographic insights gives financial marketers a competitive edge during this historic wealth shift.

How can marketers apply Psympl Financial Segmentation?

Psympl Financial Segmentation groups households into five psychographic profiles, each with distinct approaches to money, investing, and engagement with financial advisors.

Psympl’s platform, the Consumer ConsoleTM, offers reference materials for understanding and engaging each Financial Segment, as well as access to extensive market research data conducted with Ipsos on the Segments to inform marketing strategy and campaign planning.

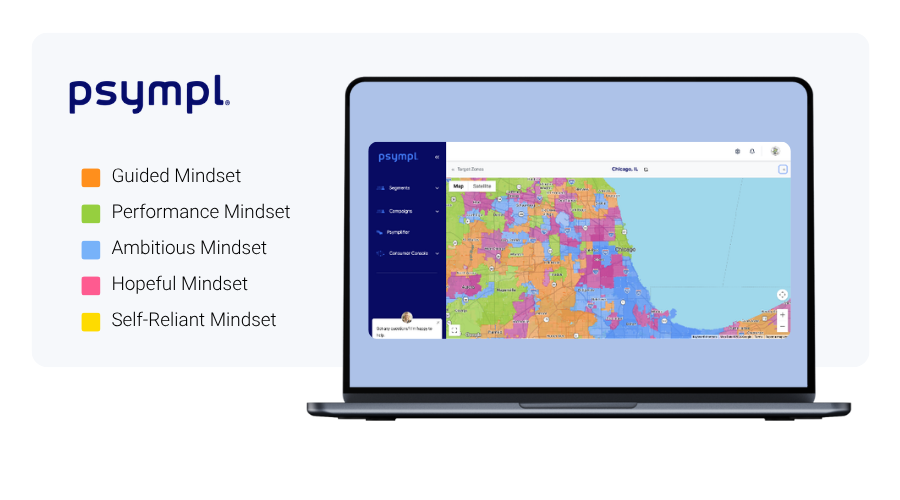

Psympl collaborates with Experian to map psychographic segments for all U.S. adults over 18. This allows financial services brands to enrich their consumer databases and find target customers based on psychographic, demographic, and socioeconomic profiles.

Experian Marketing Data also powers Psympl’s Geo-Targeting tool, which heatmaps the U.S. by psychographic segments down to the zip code, with filters for demographics, socioeconomic factors, and household counts.

Psympl’s platform also includes the PsymplifierTM, which uses Psychographic AITM to create, analyze, and rewrite marketing content tailored to specific segments or generate new content from simple prompts.

How do Psympl and Experian aid targeting strategies?

Psympl and Experian support targeting strategies by connecting psychographic insight with consumer data, geography, and channel preferences. That combination gives financial institutions a more actionable view of who to target, where to reach them, and what message is likely to resonate.

By connecting psychographic insights with consumer data, geography, and channel preferences, Psympl and Experian show financial institutions who to target, where to reach them, and what message will resonate, forming the foundation for effective targeting.

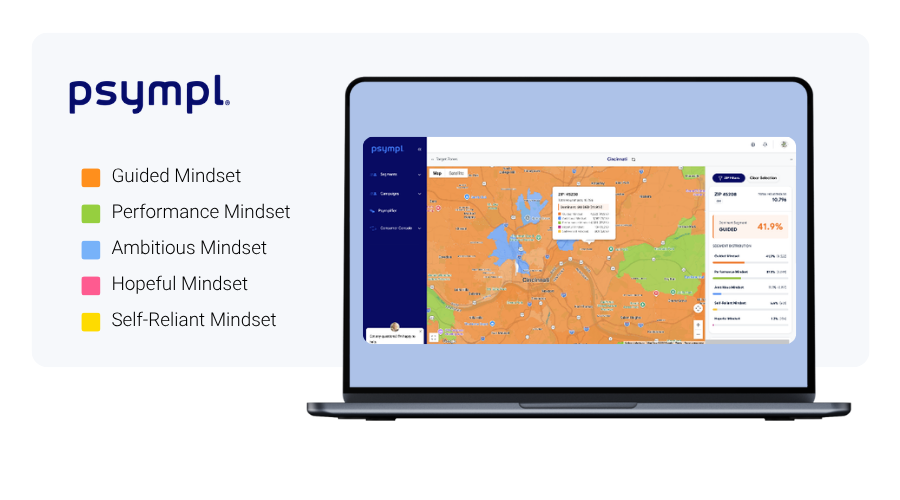

For example, a bank can pinpoint areas with consumers who prefer in-person service. Psympl’s Consumer Console™ highlights the Guided Mindset segment, those seeking expert financial help with $250,000+ in assets, as prime prospects. Psympl’s Geo-Targeting feature, powered by Experian Marketing Data, heat-maps where Guided Mindset households with $250,000+ in assets are concentrated.

In this example, one location stands out with a high representation (41.9%) and concentration (10,796 households) of the targeted Guided Mindset segment with $250,000+ in investable assets, shown in orange on the heat map. While nearby areas are dominated by Ambitious Mindset (blue) or Performance Mindset (green), the data suggests that ZIP code 45208 is an excellent candidate for a new branch, supported by targeted print, outdoor, or digital marketing.

Beyond location, Psympl’s research and Experian TrueTouch help firms choose the best channels for each segment and predict responses to direct mail, email, digital, and broadcast channels. Enriching customer databases with Psympl segments lets firms tailor messages—like notifying Guided Mindset customers about new locations, and use the Psymplifier™ to quickly generate targeted marketing content.

What are the top use cases for psychographic profiles?

By addressing customer motivations and priorities at every stage, organizations drive consistency, align communications, and deliver on customer expectations, whether acquiring, retaining, or upselling clients.

Relationships with Baby Boomer clients often do not carry over to younger heirs, who typically have Ambitious and Hopeful Mindsets instead of the Guided, Performance, and Self-Reliant Mindsets more common among older generations. Psychographics reveal these generational differences, distinct needs, values, and engagement preferences, so firms can anticipate, address, and communicate more effectively across generations.

Tools like Psympl’s Consumer Console and Psymplifier, combined with Experian TrueTouch Engagement data, equip financial professionals to tailor interactions and marketing content to each segment’s unique preferences, maximizing impact and receptivity.

Firms that fail to adapt to the needs and preferences of younger generations will inevitably lose AUM. The Psympl platform, enhanced by Experian data, positions organizations to turn The Great Wealth Transfer into an opportunity rather than a threat.

How can banks, credit unions, and wealth marketers start using psychographic segmentation?

Building a psychographic segmentation model is resource-intensive and challenging to scale, but Psympl’s collaboration with Experian addresses these challenges. After 20 years leading psychographic initiatives at Procter & Gamble, I wish I’d had Experian’s data and capabilities; they make planning and measurement much easier.

To start, enrich your CRM with Psympl psychographic Financial Segments from Experian. Analyze your customers to see which segments are over- or under-represented, revealing strengths and growth opportunities. Identify which segments most use specific products to target Prime Prospects. Then set a campaign goal and test psychographic messaging against a control group or with pre- and post-measures. Start small, earn, and adapt as you go.

Once you see results with relevant, psychographic-based content, expand this approach to prospecting, customer experience, and other applications.

Where can readers learn more?

I appreciate this opportunity! To learn more, readers can visit the psympl.com website, and more specifically, the Resources Page on the website, which includes videos, whitepapers, and guides for utilizing the Psympl psychographic Financial Segments for customer acquisition, retention, and enhanced engagement.

Contact us

About our expert

Brent Walker, Co-Founder and Chief Strategy Officer, Psympl

Brent Walker is Co-Founder and Chief Strategy Officer for Psympl, helping wealth management firms, banks, credit unions, and financial services enhance customer acquisition, retention, and cross-sell initiatives. Brent started his career in Brand Management at Procter & Gamble, and over 20 years he led teams in product management, customer marketing, and psychographic segmentation initiatives. In 2012, he cofounded his first company focused on psychographics in healthcare, which saw a series of multiple acquisitions. Brent has delivered a variety of publications covering critical marketing topics, featured in Forbes, The Ohio Bankers League, The Commonwealth Fund, and Healthcare Finance.

Latest posts

Discover how Experian pairs DASH data with Experian Marketing Data to help marketers develop better TV audience buying strategies.

Advertisers continue to increase their spending across addressable TV, connected TV (CTV), and digital. According to IAB’s “2021 Video Ad Spend and 2022 Outlook” report, digital video ad spending is expected to increase by 26% to $49.2 billion in 2022. Understanding who consumers are and how to best reach them in their preferred channel is becoming more complex. Damian Amitin and Colleen Dawe discuss how a seamless identity strategy can address the complexity of the emerging TV space. The evolution of identity resolution Around ten years ago, the idea of digital “identity resolution” or “Device Graphs” was born. This idea connected cookies and MAIDs to understand when many IDs were the same person or household. In more recent years, our industry began to connect that initial understanding to the CTV ecosystem. But, a large part of the TV ecosystem existed in silos, like first and third-party audience data, and the growing advanced TV market. The goal of identity resolution has always been to understand the consumer better. To achieve more accurate targeting and measurement in the CTV ecosystem, we must incorporate the following: What we know about the household and consumer from an ID perspective Who the consumer is as it relates to audience data, as well as the wealth of first-party data in the advanced TV space We know the cookie is a flawed way to collect data. While Google delayed the deprecation of third-party cookies, there are other challenges that we face right now. Such as the glaring gap in Safari traffic and the Identifier for Advertisers (IDFA) turning to “opt-in.” Understanding consumer behavior across devices and platforms continues to challenge marketers and publishers. These challenges are creating the need to find more stable identifiers. Though the cookie remains valuable, it has an uncertain future. This has led advertisers to place bigger bets on the combination of addressable and CTV. The overlap in addressable and CTV data leads to fragmentation Personally identifiable information (PII) makes up the majority of addressable TV households’ data. Part of the attraction to CTV is that their IDs remain universal, persistent, and stable. Analysts project that CTV ad spending will hit $23B in 2023. Consumers now have an average of 4.7 streaming subscriptions per household. It’s no surprise then, that Disney+, HBO, and Netflix released or announced ad-supported tiers. Addressable TV and CTV are often thought of as distinct markets across the industry. But, in the context of identity, we should look at them through the same lens. Millions of households still consume TV and video content via a set-top box or through apps on CTVs. This is in addition to what they consume on their laptops, tablets, and phones. Of the top 11 cable and satellite providers, 65 million U.S. households still have a box in their homes. On the other hand, approximately 96 million U.S. households have at least one or more Smart TVs and streaming services. With about 126 million total U.S. TV households, that’s a lot of overlap. There are still significant numbers of both addressable and CTV homes. How can we address fragmented TV consumption? Through a holistic and comprehensive approach to identity. An approach that captures addressable TV, CTV, and digital identifiers. An approach that captures all audience attributes inside of a single identity graph. This is the ideal approach for publishers, AdTech vendors, and brands. Discover how to unlock holistic identity How can we achieve a holistic identity? Through a three-pillared approach: First-party data onboarding Digital identifiers Consumer data First-party data onboarding Bringing offline data from a brand’s consumers is very valuable due to the quality of the data. Because the data is being collected right from the source, you know it’s accurate. It provides the foundation you can build your identity strategy from. Digital identifiers Once you create a foundation with first-party data, you need to connect it. Either with an internal or licensed digital ID graph. Then you can understand the connections between all devices within the household. Consumer data After you know which devices tie to a single consumer, you’ll want to act on that knowledge. The next step is to partner with a data provider that can help you understand your consumers. Establishing this partnership will help improve targeting, measurement, and the customer experience. To achieve a well-rounded customer view tomorrow, we need to start today The three-pillared approach bridges the gap between the offline and online worlds. This provides a well-rounded view of customers and audiences. However, the ability to tie these aspects of identity together still presents several challenges. To achieve the three-pillared approach today, you need to use many vendors and fragmented data sources. Often with conflicting data. As we look forward, the tools to do this are becoming more advanced and unified. The players in our ecosystem should adopt a seamless identity strategy. One that provides a privacy-safe yet full-picture solution. That means capturing and unifying all devices within a household. While also understanding the consumer behaviors and profiles behind those devices. Keep up with your customers and their data Once we create an informed identity strategy, we can begin to understand the makeup of each household and the individuals within. In this new world, personalizing the experience for an audience is key. Where do they prefer to spend their time? What type of content are they most engaged in? Only then can we as an industry provide an optimal experience for each consumer. All while driving greater ROI for advertisers and publishers. Are you ready to know more about your customers than ever before? Let’s get to work together to achieve your marketing goals. Contact us to learn how we can connect the complex dots of identity resolution. About our experts Damian Amitin, VP of Enterprise Partnerships, Experian Marketing Services Damian Amitin is the VP of Enterprise Partnerships and joined Experian during the Tapad acquisition in November 2020. Damian is a senior sales and partnerships executive, specializing in the identity resolution and marketing data ecosystem. Damian helps brands, publishers, and technology vendors enable enhanced ID resolution through The Experian/Tapad platform to attain a 360 view of the customer across targeting analytics, attribution, and personalization. Colleen Dawe, Senior Account Executive, Experian Marketing Services Colleen Dawe is a Senior Account Executive on the Advanced TV Team within Experian Marketing Services. With 15 years of experience working within the television ecosystem, Colleen works with clients to bring the value and expertise of Experian to support their objectives in the areas of data, identity, activation, and measurement. Get in touch

Brands can leverage non-clinical factors, like the social determinants of health, to gain a holistic view of their patients and increase access to care.