Credit Management

This weeks guest post is by Katie Keitch, VP of Commercial Services at InsideARM. InsideARM is a media company that specializes in training for credit management professionals. To receive future articles sign up to the InsideARM newsletter. Oftentimes organizations miss out on higher bad debt recoveries. The number one reason this happens is that they hold on to the debt for too long. It’s important in the onboarding process to start with the end in mind: setting yourself up for success by having mutually agreed payment terms, billing cycle, right party contact information, etc. However, even if you have done that all correctly from the start, some customers, unfortunately, aren’t able to pay for one reason or another. Here’s how to know when to cut bait and enlist the help of a 3rd party collections agency. Don’t ignore the warning signs Your customer isn’t paying within the agreed payment terms. Or maybe they were paying on time, but lately they have been pushing farther and farther out. Your customer is showing past due more often and/or farther past due than historically Your customer hasn’t paid you in the last 45+ days Your customer is 60+ day’s past due to their mutually agreed payment terms Your customer made broken promises to pay Your customer stopped taking your phone calls Your customer’s emails are suddenly not going through or the physical mailing address is returning mail to sender Be proactive in your communication Don’t be afraid to ask how things are going, especially if you noticed they are outside their normal payment cycle. Immediately offer alternative options instead of having to pay you the full past-due amount today. Set the expectation that it’s vitally important that they keep the communication lines open. If they have something come up, they need to call you. And always answer your calls. You have to be blunt and purposeful in your approach here so that they understand the commitment to you. Offer some alternative options While it’s so important that your customer takes your calls, it’s equally important to give them attainable goals. If they feel that they have options, they are more likely to keep the lines of communication open. Alternative options might include things like offering the ability to make a small weekly payment towards the balance. Offer your customer the ability to continue doing business with you while making payments. The best way to accomplish this is to set the expectation they must remain current on the new invoices. Make the weekly payments smaller so they are able to keep to the commitment. Your customer can always call you and make additional payments. However, it's important that they stick to their original commitment. Ask your customer what is the dollar amount they can afford to pay weekly (hopefully automatically)? If the dollar amount is less than their normal spend, this is a sign that they can’t stay active as a customer. Give them the option to use alternative vendors until they can cover their average invoices plus the delinquent amount. Your stakeholders in Sales may not be immediately supportive. but they will thank you in the long run. Especially if they have chargebacks or are commissioned on collected revenue. Last, in my experience, customers appreciate that you recognize and don’t want to see them get to a place of debt they can't repay. The snowball effect of continuing to let a customer who can’t pay continue billing can be detrimental. No one wins, if your customer files for bankruptcy or worse, go out of business. Recommended exercise, review customers that haven’t made a payment to you in the last 45 days. These should be a top priority for collections. Make your goal to be first in line not last Don’t miss out on collecting because you waited too long to send an account. If you are working with a 3rd party collections agency, do you have an easy process for your collector to recognize it’s time to cut bait? Are the collectors being trained to recognize the warning signs and make quicker decisions? Don’t let your customers get into the 90 and 120-day buckets. They should already be with your third-party agency at that point. That is if you want an opportunity to recover the debt and fast. If you are using the steps outlined above, you should be seeing higher recoveries.

The credit industry works very differently than it did even a few years ago. In recent years, new technology and the availability of analytics means that credit departments have much more information to make decisions. When both commercial and consumer data is used together, departments unlock a lot of powerful data that can be combined for more accurate decisions. However, some credit departments have not changed their processes and staffing structure. By using the traditional approaches even with new technology and data, credit departments are not able to see all of the possible benefits. I recently spoke on a panel of credit management executives at the High Radius Conference. During the talk, we touched on this topic and talked afterwards about what credit organizations need to do. Jan Minniti, Senior National Account Executive with the National Association of Credit Management mentioned that while many large organizations are using automation, even smaller shops can benefit as well. But her larger point was in order to transform, organizations must change the skill sets that they are recruiting, and expand training offered to current employees. Here are a few keys to help your organization transition to modern credit management: 1. Understand the recent evolution of credit models and technology As Minniti pointed out, we started out with general payment score models that were applied to everyone. However, today more specific models are available (for example, specific to an industry), so you can choose the best model depending on who you are selling to. These new models move us into a new generation where instead of making gut feel decisions or spreadsheets to track data, we can use statistics to not only assess risk, but also assign credit line increases. These scores and credit lines can then be fed to automated tools to manage the order-to-cash process. Even more importantly, we can use automated technology for account management strategies, which increase efficiency, maximize account potential and reduce fraud. In our experience at Experian, we have evidence that machine learning reduces manual reviews by as much as 74 percent. 2. Learn how credit managers can revise their role and processes Research recent changes in the financial services industry for inspiration on what is possible and how to help your department get to the next generation. Typically the FinTechs and large banks are on the leading edge of advances in risk management. By starting with analytics, the financial industry has driven a lot of innovation and change. They have also focused on data management to evolve to a frictionless environment. Think of how your company can incorporate these changes. But most importantly, how you as a credit manager can introduce and drive the change. 3. Revise the credit manager role to include more strategy Instead of shrinking from the change out of concern that technology will replace your role, credit managers need to lead the change. Start by learning what’s possible with regards to both technology and data. Share it with other credit managers and leadership to help your company be an early adopter. But, be careful not to fall into “shiny object syndrome”, where you use technology just because its available, even though it might not yet have the features you need. A solution in search of a problem is always a questionable approach. Minniti says that she knows changing the roles is challenging because it is a big shift and credit is not typically the shiny, new area of the company. However, to reduce risks and impact change, credit managers must seek greater visibility with the C-Suite. “Credit managers should educate management by using reports to show the importance to your company. Use data to show how much money you are saving the company,” says Minniti. “It’s also important to talk about automation, which actually helps credit managers stay relevant instead of replacing their jobs.” Having an automated credit strategy is also a great way to manage in times of turnover, or in trying to up level expertise. 4. Revising staffing and hiring guidelines Minniti says it starts by picking good analysts who can replace you. “If you staff with people who listen to what the machine learning is saying, but don't have the ability to think beyond that then who fills your shoes when you move on? What happens to the credit department?,” says Minniti. “We will always need people to tell the machine what to do, be able to adjust the model when the economy changes.” One of the biggest reasons that many managers and departments are resisting technology is fear of being replaced. This simply isn’t going to happen. Without the experience and background, credit models quickly decay. It is impossible to turn over all of the thinking behind credit decisions to machines. Someone needs to be there to manage the ongoing performance of the models, and make sure the analytics track with changes in the marketplace. Credit departments that take initiative to lead the change, to use the new technology and models, will demonstrate their value to their organization. By using automation and machine learning, the credit department becomes more valuable to the organization instead of less. By proactively managing the change and taking the lead, you can set your department on the right path to lead the transformation of your company as well as the credit industry.

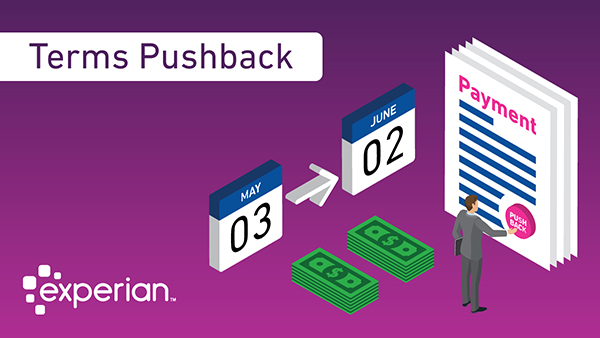

In this week's guest post, Scott Blakeley shares perspectives on a growing trend in business - Terms Pushback (TPB). Scott is the founder of Blakeley, LLP, a noted expert in the field of creditors’ rights, commercial law, e-commerce and bankruptcy law. Scott regularly speaks to industry groups around the country and via monthly webcasts on the topics of creditors rights and bankruptcy. After a slow sales quarter, a large retail clothing store needs to improve their working capital and cash flow. Before the 2008 recession, the retailer likely would have turned to traditional business credit options. However, after the downturn, lenders changed their qualifications and terms, making traditional credit options a much less desirable option. In some cases, retailers, especially midsize or new businesses, can no longer even qualify for traditional credit sources. Businesses are now increasingly renegotiating their payment terms with suppliers through a program called Terms Pushback (TPB). When a jewelry retailer reviews its payment terms, for example, it sees that the main vendor supplier for jewelry currently requires payment 15 days after delivery. As a deliberate strategy — which is different from a company not having the money to pay its bill — to give the retailer more working capital, they reach out to ask the supplier to change the terms to 30 days. This means they would have access to the money paid to the vendor for 15 days longer; this process is often referred to as trade credit. Credit Today found that the most common extension is for 16 to 30 days, with 45% reporting this range as the most common extension. Impact of Terms Pushback on Suppliers While TPB improves cash flow for customers, it causes issues for suppliers because they must wait longer for their payment. Many consultants are now actively recommending TPB as a best practice. Because international companies more commonly using this strategy, many U.S.-based companies are adopting it due to international influence. Companies operating as middlemen between retailers and manufacturers often face the biggest challenges. Longer terms mean that they have less capital to buy more products and have a higher number of outstanding receivables. Additionally, businesses have lower cash conversion metrics, which can hurt publicly traded companies and cause concern for shareholders. According to Credit Today Bench-marking, 19% of suppliers always or usually say no to requests for extended terms, and 3% usually agree. Interestingly, 4% report that their answer depends on customer size — yes to large customers and no to small customers. However, the majority (63%) of businesses review the requests on their individual merits. However, denying the request often has long-term ramifications. If the business denies the request, the customer must pay or suffer credit damage. Customers often get around this by paying late enough to improve their own cash flow but before credit damage occurs. Even more challenging, suppliers are often hesitant to report customers to credit bureaus because this often permanently damages or even ends the relationship. If a supplier denies the request, the majority of options to get the payment are punitive. For example, the supplier can charge a late fee for payment. However, the customer may still decide that the value of the money for the extra days is worth more than the late fee. Other avenues include implementing a credit hold, having two price lists, terminating credit, firing the customer and reporting the customer to industry groups. However, each of these options permanently damages and probably ends the customer relationship, which may result in loss of a high volume of sales. Effectively Managing Terms Pushback with Supply Chain Finance Programs Supply Chain Finance programs are asset-based lending programs structured to improve a customer’s payment terms, reduce costs and improve cash flow enabling financial institutions to pay suppliers for invoiced services. Suppliers can benefit from SCFP as it receives payment within normal terms or earlier which helps keep the credit team’s credit scoring and risk models consistent. The customers benefits as well as their capital is not tied up in day-to-day operational payments and creates more reinvestment opportunities. When a company receives a TPB request, the first step is evaluating the customer — their credit, the risk, the volume of business and the value of the relationship for the supplier. Often, larger companies have an advantage over smaller companies when negotiating term extensions because their business relationship is worth more to the customer than the monetary value of the shorter term. Here are three best practices to managing TPB requests: Offer incentives for shorter terms. Instead of punitive actions, consider giving customers who pay within shorter terms a discount or an annual volume discount for consistent payment with shorter terms. Actively monitor threshold for customers with extended terms. Suppliers must effectively manage their own cash flow to make payroll and other expenses. By extending too many customer terms, suppliers can jeopardize their own financial stability. Create a team to evaluate requests. By establishing a process to handle the requests and a team to formally evaluate requests, suppliers can more effectively evaluate all aspects of the decision, such as the risks of extending to its own financial health and the risk of losing the client relationship. With a team made representing stakeholders from different departments, all perspectives can be represented and considered. As TPB becomes more common as a strategy, suppliers must proactively create a process to manage requests. Often, extending the terms can improve the customer relationship and even increase the amount ultimately paid. By creating a team and strategy, suppliers can make the smartest decision and actively manage pushback requests. Scott Blakeley is a founder of Blakeley LLP, where he advises companies around the United States and Canada regarding creditors’ rights, commercial law, e-commerce and bankruptcy law. He was selected as one of the 50 most influential people in commercial credit by Credit Today. He is contributing editor for NACM’s Credit Manual of Commercial Law, contributing editor for American Bankruptcy Institute’s Manual of Reclamation Laws, and author of A History of Bankruptcy Preference Law, published by ABI. Credit Research Foundation has published his manuals entitled The Credit Professional’s Guide to Bankruptcy, Serving On A Creditors’ Committee and Commencing An Involuntary Bankruptcy Petition. Scott has published dozens of articles and manuals in the area of creditors’ rights, commercial law, e-commerce and bankruptcy in such publications as Business Credit, Managing Credit, Receivables & Collections, Norton’s Bankruptcy Review and the Practicing Law Institute, and speaks frequently to credit industry groups regarding these topics throughout the country. He is a member on the board of editors for the California Bankruptcy Journal, and is co-chair of the sub-committee of unsecured creditors’ Committee of the ABI. Scott holds an B.S. from Pepperdine University, an M.B.A. from Loyola University and a law degree from Southwestern University. He served as law clerk to Bankruptcy Judge John J. Wilson. He is admitted to the Bar of California.

Today we are very proud to be taking the wrapper off the next generation of our flagship commercial credit management application, BusinessIQSM 2.0. To meet the ever-changing needs of our clients, we continue to grow and modernize with them. This innovative and powerful analytical web-based application is designed for commercial enterprise and small-business risk management. From the new interface and side bar navigation to enhanced search and match technology, to judgmental and rules-based scorecards, all the way to custom model scores, Experian’s BusinessIQ 2.0 has something for everyone. Let Experian meet you where you are and take you to where you want to be. BusinessIQ 2.0 Overview In this video we highlight some of the key features of BusinessIQ 2.0. Learn more by going to:

As a Senior Consultant with Experian Advisory Services, Gavin Harding works closely with many of Experian's FinTech and Financial Institution clients to find solutions to complex problems. We sat down recently to talk about bank partnerships, how they come about, what makes them successful, and how Experian supports them. Do you see a lot of collaboration between banks and FinTechs? The latest statistics show that 67 percent of banks and FinTech’s are either currently cooperating, or in discussions about cooperating, or exploring collaboration. So, yes a very significant proportion are considering collaborations. Why collaborate at all? You know it's interesting, they have different skill sets, different assets, different backgrounds. So for example; banks have really deep, broad customer relationships. You know think about your Mom or Dad bringing you to your local bank to open up your first account. Think about your student loan. Think about your mortgage. What kinds of relationships exist? So banks have really deep and broad relationships. But traditionally the experience with banks has not necessarily been great in terms of turnaround, in terms of the friction or pain involved in getting a loan or opening an account. On the other side, FinTech’s are really good at that customer experience. They describe it as either low or no friction. So very quick turnaround times. But they're very much transactional-focused, meaning single products. So FinTech has the technology and the experience, and banks have the depth of relationships with customers. You bring those two parts together and you've got a pretty amazing potential opportunity. There are as many relationship types shapes and sizes as there are people on the planet. Everything from cooperation on basic operations, meaning, a FinTech takes applications for a bank and then passes them on. All the way over to full-fledged integration of systems, personnel, capabilities, skill sets, and so on. So pretty much the broad spectrum. What works well? So it works really well when they are well-matched. So what I mean by that is, when the skill sets from one organization match the other. When one enhances the other, and it works really well when there are long and detailed discussions and preparations for the relationship. Meaning, they align and discuss goals, objectives, what each organization's role is, what each brings to the table, and very specifically how they are going to cooperate. What are the pitfalls? Well, the same pitfalls. So the pitfalls are that the relationship goals differ, or aren't aligned, or that one organization feels like they are bringing more to the relationship and that the partnership is equal, or when it feels as if each partner, each organization is not getting value from the relationship over time, and once again that reinforces the need for those detailed discussions before getting into that partnership or relationship. How does the process work? So it begins with a discussion. I've seen these partnerships start with a discussion over dinner at a conference. I've seen them start through a LinkedIn connection. I've seen them start over coffee. So it really starts with an exploration of who's out there? What organizations may be interested in even discussing some kind of collaboration? So it starts with the conversation at the very basic level, even when we see in the Wall Street Journal major strategic alliances between organizations, starts with people, and starts with that very simple conversation and connection. What are some key elements to be aware of? Well again it comes down to what each party brings to the relationship and what the goals are. So a good alignment of the capacity of skill sets, an alignment of investment in terms of time and resources, and very specifically a definition of who does what, what the accountabilities are, and what everybody's expectations are. They are fundamental to the success of any type of business arrangement or partnership. How does Experian support these partnerships? So the interesting thing is we have very deep relationships with both sides. So we bring data, solutions, consulting expertise to FinTech’s and to banks. So, it's really interesting we find ourselves in the middle of a lot of these conversations, and how we help is by understanding systems, technology, data, the best of both organizations involved in the conversations, and how to bring all of that together for a good focused efficient successful outcome. A couple of years ago this was new meaning that banks saw FinTech’s growing, and kind of looked at them a little bit maybe as competition, as potentially the enemy, FinTech’s saw themselves as disrupting the world and completely innovative and new. What's starting to happen is both sides are coming together, realizing that they are both part of the same financial industry, serving the same customers, maybe in different or new ways with different products. But in the same industry. So there is very much a coming together, an alignment a co-mingling, consolidation of all these various aspects of the industry. And I think it's really positive for consumers. More products, more quickly, and a better experience overall. Do you think a FinTech's ability to create more dynamic mobile experiences is a key element Certainly and so the big question we help banks answer in this space is, do we build it? Do we buy it? Do we partner? and build and buy or partner refers to the technology the infrastructure and the experience. So if you have a pretty big bank and they've got a old website, old process, lots of paper, lots of regulations, lots of pain in the process. Well they can look at one of the more advanced sophisticated mature FinTech’s and essentially use their platform, their engagement, their data, connect that to the bank's customers and in a very very short time transform that experience in a very positive way for their banking customers. Learn about FinTech Lending Solutions

When you’re launching a new product, business line, or starting up a business, you’ve got to move fast and break things. This means taking a minimum viable product (MVP) approach, where you’ve got to sacrifice scalability by implementing manual processes to support the early-stage business. Commonly, a manual process will be in place for credit applications and approvals – pulling the credit report, reviewing the data against a scorecard or policy, and then making the decision. Since this likely takes a day — or often longer — the process decreases your customer’s experience, and can hurt your ability to scale and grow revenue the longer you wait to automate. To grow the business and take it to the next level, you need to migrate away from the paper-pushing approach. The next step is to move toward an automated solution that integrates credit decisions with the back office, such as an ERP, CRM, or another custom system, employing APIs. Using an Application Programming Interface (API) to Connect to Your Decision Engine An API, or Application Programming Interface, is many things. It’s a set of instructions and technical documentation for developers. It’s a collection of services that allow you to interact with a product or service. And it’s a way for businesses to open up and allow for new kinds of innovation – allowing for new business models and application development that wouldn’t be possible without APIs. In the last decade, APIs have become system agnostic, meaning they plug-and-play into nearly any system because they are standardized and popular amongst the development community. Because of this popularity, APIs make it easier for the business to get buy-in from the IT department, which is essential to automating the credit decisioning process. Without an API, the IT department must devote significant resources to the project because more infrastructure to host large database will be required. APIs allow you to pull data in real-time only when you need it, reducing system complexity and decreasing application development costs. Reduced complexity also means less risk because you are more assured that your IT department will be successful with the integration. Often, when IT departments are presented with information about the API, their response is “No problem, this is standard. We have integrated with a very similar API before. We can do this.” How does your decision engine interact with APIs? You can use APIs to get the raw data elements your credit policy or model needs to render a decision, no matter if the data is internal to your business or provided by third parties. Taking Decisions to the Next Level with Machine Learning According to a recent Harvard Business Review project, the key to successfully utilizing machine learning isn’t to get caught up in new and exotic algorithms but to make the deployment of machine learning easier. There are many use cases where machine learning can be employed, but use cases where data-driven decisions are being made, as in the credit approval process, are archetypical. During the early stages of the machine learning process, you train the model by feeding it data from past applications. Then, as you use the engine for real-time processing, the engine learns from past decisions. If the engine was originally approving applications with a borderline credit score but found that these applications often ended up being poor risks, the model would then begin turning down these applications. The key ingredient in making machine learning start to work for your credit department is to have domain experts, credit managers, help the IT department focus on the key variables that can help the machine learning model to predict key outcomes – credit losses, bankruptcies, and business failures, and to put the models through many rounds of testing and validation before putting them into real-life practice. Now is the time to move your manual processes online using an API and machine learning. According to Mary Meeker’s Annual Internet Trend Report, 60 percent of customers pay digitally compared to 40 percent in the store. And it’s likely that the gap will continue to grow. The longer you wait, the further ahead your competitors will be in digitizing the customer experience — and the harder it will be to regain your footing and catch up.

For credit and risk managers, how effectively you manage your book of business can sometimes be the difference between tirelessly chasing after accounts for collections or proactively growing your portfolio. Though there may be many factors that affect your specific credit risk management process, the underlying goal to reduce and manage your exposure to risk does not change. To help you successfully manage your portfolio, we address 4 common mistakes you need to avoid: 1. Not automating your processes By not having an automated, standardized method of assessing your current accounts, overall portfolio exposure to risk increases substantially. The manual review process relies too much on shrinking human capital, requires more time to complete, and can cause inconsistencies across the board. Automating processes where you can will help you focus your resources to the applications and accounts that need attention or manual review. 2. Not setting up triggers that alert you of key events When you know problems are coming, you can take steps to protect yourself and your business. The sooner you know about something, the faster you can act on it. Setting up triggers that notify you of key changes within your customers’ accounts like a rise in late payments, increased number of collection filings, or bankruptcy filings, allows you to keep a close eye on your customers and take immediate action, if necessary. Especially when your portfolio outgrows your resources to manage it, setting up automated triggers can give credit and risk managers the foresight to manage proactively, rather than reactively. 3. Not monitoring for risk (or growth) Managing a large portfolio can be extremely labor-intensive if you don’t apply risk scoring. A traditional risk score, in this case, usually considers the credit, public record and demographic attributes of the account, and applies a value to the results as a means of quantifying risk. This helps you prioritize your time and efforts on the minority of customers with scores that signify increased credit risk, rather than all your customers at the same time. On the flip side, you can target accounts with positive scores for growth opportunities. 4. Not segmenting your portfolio Another common mistake that many portfolio managers make is not segmenting their portfolios to identify insights at a macro level. For instance, leveraging data to segment your customers and accounts by industry, business type, business size, etc., can help you uncover hidden trends not obvious otherwise. This then allows you to apply appropriate treatment strategies to mitigate risk within the accounts. Additionally, you can identify market opportunities for growth using SIC/NAICS codes and other marketing data sources to grow your footprint. Want to talk to an Experian expert regarding your portfolio management strategies? Contact us today.

When a new customer wants to establish credit terms with you, the first thing they’re asked to do is fill out your credit application. When you hand over a paper application, did you know you could be negatively impacting your revenue or creating a poor customer experience? Some companies don’t. More than likely, your customer has filled out at least one digital application in the past. The initial perception your application says about your company is that you’re out of step with technology — which may lead them to wonder where else you may be lagging behind. Digital applications provide a simplicity factor, and by not offering one, your credit approval process is perceived to be more difficult, leaving the customer with more work to do —spending extra time writing their information by hand and returning the application — either by email, fax, or in person. Because many companies have already moved to a digital application, your pen-and-paper process sticks out to the customer — and not in a good way. Not to mention, manually processing a paper application takes longer — often much longer — than a digital application. This means customers leave without a credit approval, giving them time to change their mind about their purchase or find a better deal — meaning you just lost a new sale. And even if they still choose to work with you, their relationship with your company starts out with a less-than-amazing customer experience. After the paper application is completed, the workflow process is often time-consuming, error-prone, and cumbersome. The time involved also means that your company waits longer to receive revenue from the sale. By using a manual process, your team spends hours on processing and decisions that could be better spent directly servicing customers or working on other initiatives to grow business. DecisionIQ from Experian automates consistent real-time decisions, streamlining your entire process from applications to onboarding.

All business customers are not created equal. Even companies that look solid at first glance can hide festering problems that eventually can impact your bottom line. Successful credit management requires you to carefully evaluate the financial health of every business that asks for credit terms. Here are 5 questions you should be able to answer before extending business credit: 1. Is the business what it claims to be? Sometimes, companies needing credit will provide inaccurate information to win approval. Before opening an account, you need to confirm the applicant‘s bona fides, including its location, size, number of employees, annual revenue, years of operation and similar financial indicators. 2. What is its payment history? Although past performance does not guarantee future results, a company’s payment history is often a strong indicator of how it is likely to behave in the future. Pulling a business' credit report can easily provide you a snapshot of a company's payment history as well as other risk measures. 3. Are there hidden factors that could affect its ability to pay? Are there pending judgments, lawsuits, bankruptcies, regulatory citations or other “red flags” that could make it difficult for the applicant to meet its obligations in the future? This is another area where a business' credit report will be a key factor in helping you uncover a potentially risky business. 4. How much credit should you extend? All credit contains an element of risk, but you can mitigate that risk by limiting the amount of credit you extend based on factors such as the customer’s sales volume, debt to-asset ratio and similar aspects. 5. Under what terms should you extend credit to this customer? You can mitigate risk further by carefully calibrating the combination of interest rates, minimum payments and other contract terms based on each customer’s individual financial metrics.