All posts by Brodie Oldham

Experian has released the Summer 2022 Beyond the Trends report, our deep dive on the small business economy based on our commercial small business insights.

How are small businesses being impacted by inflation? Experian Beyond the Trends report contains useful insight on small business performance.

Experian's latest commercial insights on small business delivered in an easy to

Brodie Oldham shares perspectives on the emerging business threat from the COVID-19 Delta Variant and Experian's Delta Variant Index dashboard.

The Experian Beyond the Trends report takes a closer look at challenges pertinent to small businesses. The Winter 2021 edition is available now for download

Getting ahead of the economic downturn by performing stress tests and forecasts.

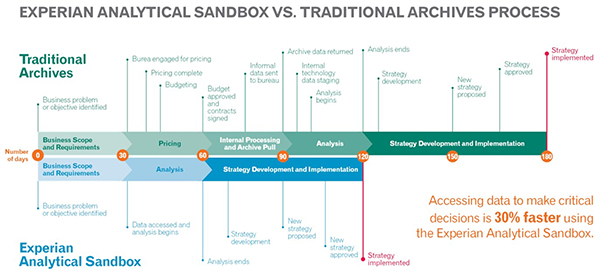

To make the most accurate business credit decisions possible, many companies are turning to data-driven decisioning models powered by artificial intelligence (AI) within machine learning engines.

The appetite for businesses incorporating big data is growing significantly as the data universe continues to expand at an astronomical rate. In fact, according to a recent Accenture study, 79% of enterprise executives agree that companies that do not embrace big data will lose their competitive position and could face extinction.

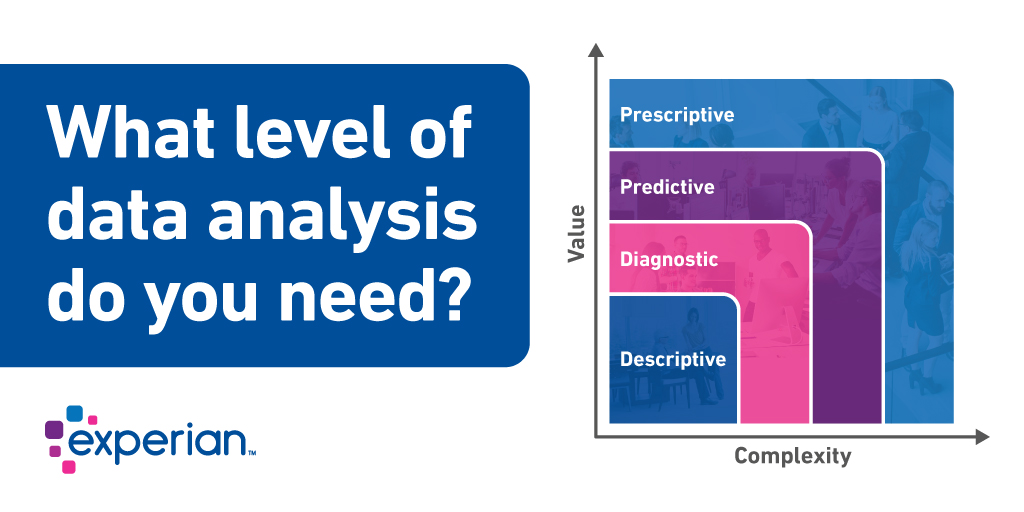

Data analysis surrounding lending practices for commercial lenders falls into 4 distinct buckets that define scope, usability, and purpose. In this post we will discuss how they differ in terms of value and complexity.