All posts by Gary.Stockton@experian.com

Small business credit performance resilient in Q3 as tariffs re-enter supply chains complicating an otherwise stable environment.

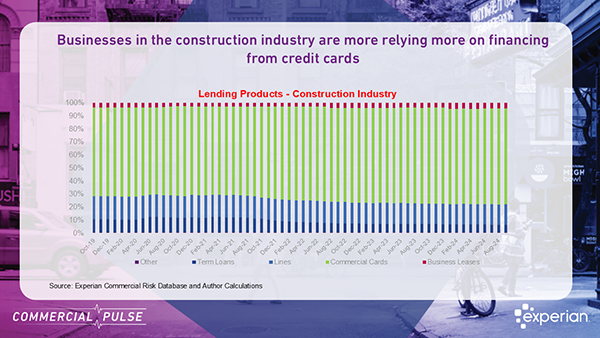

Experian's Commercial Pulse report focuses on the dynamics of the housing business and construction companies in our November 26th issue.

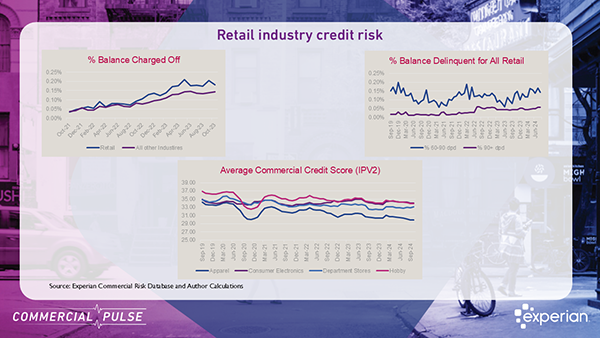

Explore the latest retail insights from Experian’s Commercial Pulse Report: credit demand surges, lending tightens, and retail growth slows.

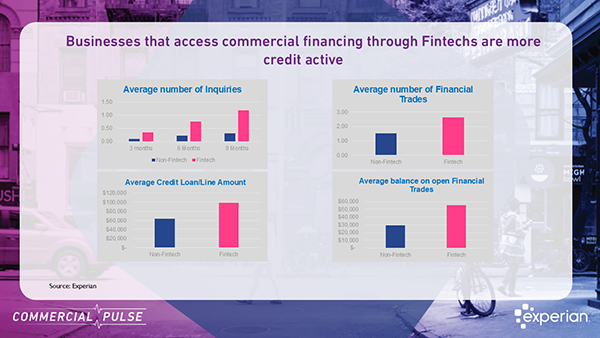

Fintech borrowers have increased credit activity, higher loan balances, but with greater delinquency risks in business financing decisions.

The Fall Beyond The Trends report offers a unique view into the challenges hitting small businesses, and how to navigate a cooling economy.

Experian’s Sentinel™ Commercial Entity Fraud Suite received a silver medal for "Best Know Your Customer/Business (KYC/KYB) Innovation.

Download the Main Street Report for in-depth analysis on recent small business credit performance.

Join the experts from Experian for a review of quarterly small business credit performance along with a macroeconomic outlook.