All posts by Gary Stockton

Navigating Credit and Policy Crosswinds Experian is very pleased to announce the release of the Q1 2025 Main Street Report. Watch Brodie Oldham present the latest insights on small business from the Q1 Main Street Report. Watch Q1 Quarterly Business Credit Review Webinar Small business performance strong in the face of significant challenges: As economic crosswinds continue into 2025, Experian’s Q1 Main Street Report offers a sharp lens into the evolving risk landscape for U.S. small businesses. With stable credit utilization, modest delinquency trends, and over 449,000 new business applications in April alone, the data points to a cautiously optimistic outlook. For risk leaders, this report provides critical insights into regional and sectoral credit behavior, the growing role of alternative data in underwriting, and emerging areas of exposure and opportunity, equipping you to recalibrate strategies in real time. Download the latest report for more insight. Download Q1 Main Street Report Related Posts

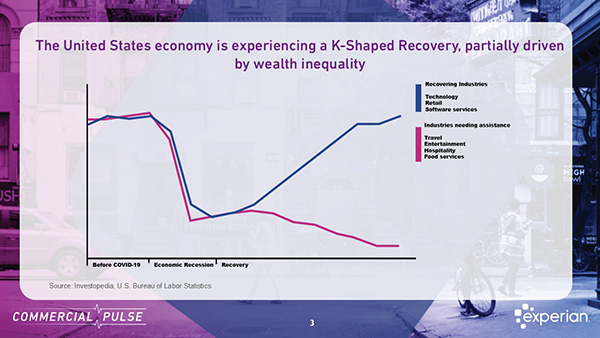

Discover highlights from Experian’s March 2025 Commercial Pulse Report: GDP dip, small business growth, and rising income inequality.

Get the latest insights on small business credit performance. During this webinar, Experian discussed small business credit conditions and presented key findings from the latest Main Street Report for Q1 2025 during the Quarterly Business Credit Review. Originally Presented:Date: Wednesday, May 28th, 2025Time: 10:00 a.m. (Pacific) / 1:00 p.m. (Eastern) Our lead presenter, Brodie Oldham, shared his insights on the macroeconomic environment and delved into the latest Main Street Report and the most recent small business credit data to examine what it revealed about small businesses' performance. We concluded the session by taking questions from attendees. Why Attendees Found Value in This Webinar: Leading Experts on Commercial and Macro-Economic Trends Credit insights and trends on 30+ Million active businesses Industry Hot Topics Covered (Inclusive of Business Owner and Small Business Data) Commercial Insights you cannot get anywhere else Peer Insights with Interactive Polls (Participate) Discover and understand small business trends to make informed decisions Actionable takeaways based on recent credit performance Get Notified About Future Webinars

Small Business Resilience Being Tested in Changing Tariff Conditions The Experian Small Business Index™ rose by 1.8 points in March, reaching 47.2, marking the third month of modest gains. Index is down 9.3 from the same period one year ago. March 2025 Index Value (Mar): 47.2 Previous Month: 45.4 MoM: +1.8 YoY: -9.3 (Mar 2024 = 56.5) March reading points to continued resilience in economy Positive indicators for the overall economy persist: unemployment remained low at 4.2% in March, core inflation decreased to 2.8%, rent inflation dropped to 4.0%, and March retail sales were up 1.4% from February. Consumer and business owner optimism continues to decline, signaling uncertainty about the economy's sustained strength. Fed Chair Jerome Powell has highlighted the country’s solid economic position while also expressing concerns about the effects of tariffs, suggesting they will proceed with caution when determining changes to rates for now. Despite some economic headwinds and uncertainty among consumers and small business owners, small business owner optimism remains above the historical average. The rate of new business starts has remained very high since the pandemic, and in March the 452,255 new business starts represents a 6.4% increase from February. The three-month increase in the index suggests that the environment for small business owners is strong, indicating their likely continued investment in their companies. Explore Experian Small Business Index

April 2025 Pulse Report reveals trade disruption uncertainty, small business sentiment shifts, and a surge in manufacturing entrepreneurship.

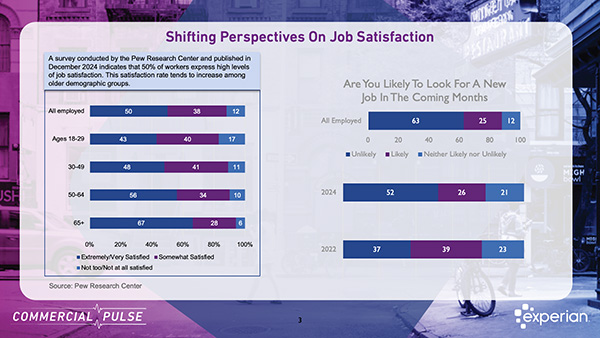

Despite concerns about a slowing job market, job satisfaction among American workers remains high.

The Experian Small Business Index™ rose by 3.9 points in February, reaching 45.4, marking the second consecutive month of modest gains.

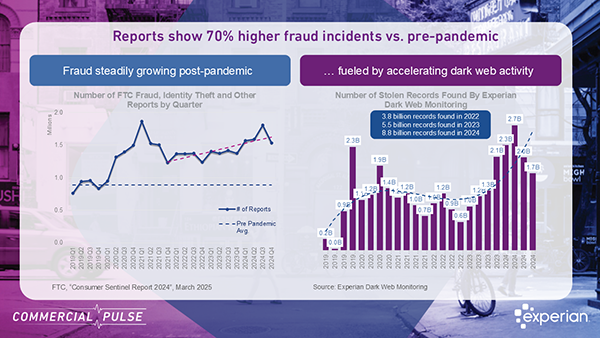

This week we focus on 2025 small business financial fraud, why it has increased, key stats, and strategies to protect your business.

The Experian Small Business Index increased by 1.0 pt in January signaling a modest improvement after December’s decline.