Small business optimism is rising to a historic high, but economic uncertainty continues to present risks. With unemployment down and rate cuts in a holding pattern, the Experian Commercial Pulse Report (Feb 11, 2025) provides a comprehensive snapshot of the macroeconomic environment and small business credit trends—essential insights for lenders, risk officers, and businesses balancing growth and risk.

Watch Our Commercial Pulse Update

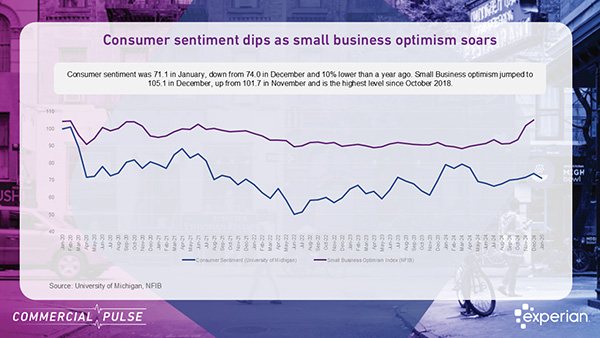

Consumer confidence slips while small businesses are more hopeful

When we think about sentiment in the economy, we see a divergence. Consumer sentiment fell to 71.1 in January, down from 74.0 in December and 10% lower than a year ago. This suggests that consumers may be more cautious about spending. Small business optimism, however, surged to 105.1 in December, up from 101.7 in November. This is the highest level since October 2018, signaling that despite economic uncertainty, small businesses remain hopeful about future conditions.

Introducing the Experian Small Business Index

With an economy as dynamic as this one, small business risk can shift in an instant. To help risk professionals, lenders, and business leaders stay ahead, we have launched the Experian Small Business Index™—a comprehensive, data-driven tool that tracks the financial health of small business owners and their businesses across the U.S. on a monthly basis. Experian trained the model for the index on data dating back to 2006. In this week’s Commercial Pulse report, we talk about how the index has evolved since the pandemic and what opportunities it reveals.

Related Posts

Experian Commercial Pulse explores how AI is changing credit risk with a fascinating study of high-impact AI industries.

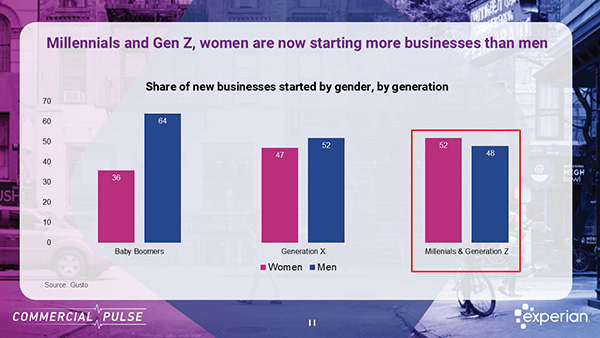

Understand the credit dynamics of women-owned small businesses and their critical role in the growth of the U.S. economy.

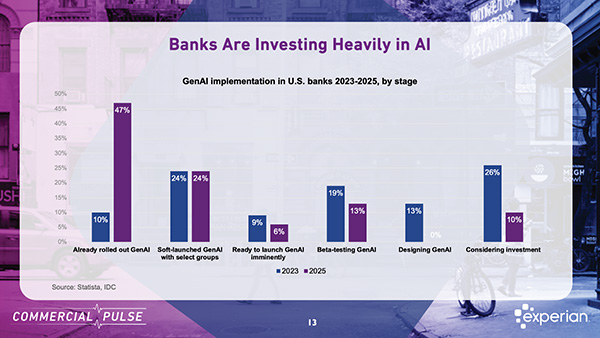

Banking transformation is accelerating through consolidation, digital adoption, and AI innovation. What must CROs prepare for next?