Commercial Pulse Highlights | 10.29.2024

Welcome to our October 29th, 2024Commercial Pulse Reportpreview! 📊 In addition to current macroeconomic indicators, in this week’s report we take a closer look at Fintechs and the credit profiles of the businesses that utilize them. Since 2018, the fintech industry has experienced extraordinary growth, fundamentally changing how businesses access and manage financial services. According to our latest Commercial Pulse Report, fintech has grown by over 140% in just a few short years, with the number of fintech companies increasing by 70% between 2019 and 2020 alone. Today, North America dominates the global fintech market, accounting for 34% of its total share.

Watch Our Commercial Pulse Update

Key Takeaways:

- Explosive Growth: The fintech industry has grown by over 140% since 2018, with a 70% increase in the number of fintech companies from 2019 to 2020.

- North American Dominance: North America accounts for over 34% of the global fintech market, making it a key player in the industry’s expansion.

- Innovative Solutions: Fintech companies have transformed traditional financial services with digital solutions in areas like payments, lending, personal finance, and investment management—led by apps like Venmo, Cash App, and Apple Pay.

- Increased Credit Activity: Businesses using fintech financing are 270% more credit-active than those relying on traditional financing, with higher inquiries, trades, credit lines, and balances.

- Higher Risk: Despite increased access to capital, fintech-financed businesses exhibit higher delinquency rates and lower credit scores, presenting added risks for lenders.

Looking for more detailedcommercial insights? Visit ourCommercial Insights Hubfor the latest trends and data on small business performance and credit. Stay informed and ready for what’s ahead!

Related Posts

Learn how to use business credit scores to analyze portfolio risk, track migration, and make smarter commercial lending and risk decisions.

Experian Commercial Pulse explores how AI is changing credit risk with a fascinating study of high-impact AI industries.

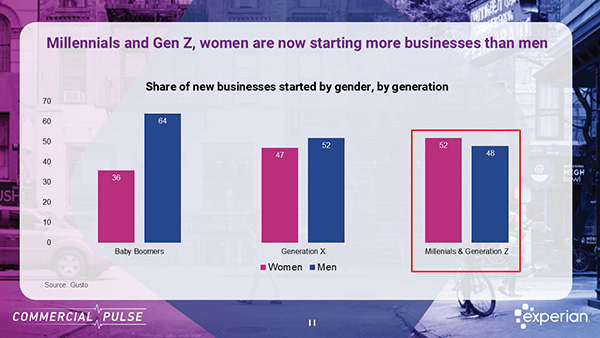

Understand the credit dynamics of women-owned small businesses and their critical role in the growth of the U.S. economy.