Identity Fraud in Commercial Applications

We recently sat down with two Experian experts to talk about commercial fraud trends and gain an understanding of why commercial fraud is on the rise, and what organizations can do to combat the problem while at the same time grant credit to growing businesses. What follows is a lightly edited transcript of our interview.

Watch Our Business Chat Interview

What follows is a lightly edited transcript of our conversation.

[Gary]: Hello and welcome to Business Chat I’m Gary Stockton with Experian Business Information Services, and today we’re going to talk about Commercial Entity Fraud with two of our experts.

[Gary]: Patricio HernandezBarron is a Product Marketing Manager here in Business Information Services, and he covers the commercial fraud space. Chris Gerding is a Consultant and he also focuses on commercial fraud. Welcome to business chat guys.

[Gary]: The two of you recently collaborated on a perspective paper called Identity Fraud in Commercial Applications, and the piece asserts that there’s been rapid growth in commercial fraud in the past few years. So, Patricio, if I could ask you, how are B2B companies affected compared to business to consumer companies in battling fraud?

[Patricio]: Let me start by saying that both commercial and consumer or B2B or B2C companies are both affected by fraud, whether this is first-party fraud, third-party fraud, or synthetic fraud. They’re both affected. Now, where it becomes different is the type of solutions that are out there in the market for them to solve it. There have been a lot more advancements on the consumer front, and it makes sense, consumer trends move a lot quicker compared to the commercial side of things.

[Patricio]: But, in 2020, it’s been considerably harder for fraudsters to get through the filters on the consumer side. So (fraudsters) being smart, they’ve started to focus on the commercial lines of business, which they already know that they’re a little behind in terms of the sophistication of consumer lines. So, it’s opened a potential opportunity gap for fraudsters to get through and businesses can’t wait any longer. They need to raise their game and make that parity between consumer and commercial lines of business in terms of the fraud mitigation strategies.

[Gary]: What’s the scale and size of the problem of commercial fraud?

[Patricio]: It’s a big problem. A recent report published by the Association of Certified Fraud Examiners stated that 5% of business revenue was lost to fraud. 55% of respondents we asked said that as of 2019 fraud attacks have increased. So there’s a clear problem right now, whether these businesses are recognizing these losses as bad credit or as fraud losses, that is the first thing that they need to focus on.

[Patricio]: And the thing is, many of our customers would tell us, “we don’t have a fraud problem”, but it was because they weren’t recognizing and discerning between credit losses and fraud attacks. So that is the first thing that they need to focus on, start differentiating and categorizing those losses differently so they can start looking into it. The other thing that I’m sharing around this topic is many times businesses tighten their credit decisioning in hopes to reduce those losses. But that was counter-intuitive because they were making it harder for potentially genuine customers to make it through the application process. And yes, the fraudsters were passing this filter or no filters but were passing this credit scoring with no problem because they knew the data that would be required, and there were again, no fraud filters in place to stop them.

[Gary]: So, Chris, can you talk about some typical scenarios in which businesses, especially small businesses are typically attacked by fraudsters?

[Chris]: Small businesses and any business have a lot in common with consumers. There are modes and fraud scenarios where both are vulnerable. And businesses typically have both financial assets and competitive information at risk. They could be phished; they could be socially engineered, and this is exactly what we read on a consumer basis when we hear about how to avoid fraud.

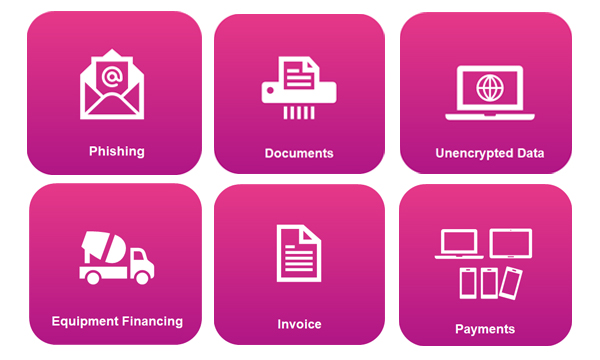

[Chris]: Second, leakage of sensitive information over the other channels can result in direct fraud, like account numbers, pins, obvious targets. However, they need to misrepresent their identity in many cases. And the contact information such as the firm name, the address, the owners, or officer’s personal details, this kind of information when compromised leads to potentially bigger and harder to detect, harder to stop fraud schemes. Consumers can be defrauded like businesses, but these are the more big-ticket business-specific categories that you’re seeing here on this slide.

[Chris]: These three represent a good slice of the many ways businesses are defrauded and small businesses with some vulnerabilities associated with not having millions and millions to spend on fraud defenses would be vulnerable to some extent. The equipment financing and leasing firms can be defrauded either out of funds or especially vehicles and heavy equipment. We see cases not many in the news, but you do hear about these, where, if you pass the finance companies fraud screen, fraudsters can successfully apply for financing and potentially come away with, I mean, a car would be on the low end of this, construction equipment for or combined for major capital items. Then they disappear.

[Chris]: Number two, fake invoices are a very easy way comparably to collect perhaps smaller amounts, but these can be forged documents sent in under the wire and they are paid sometimes by very busy accounts payable people with very few defenses in place, and something that we’re going to talk about later, fraud payments figure very largely in commercial fraud. Payments that are not backed up by good funds and intentionally sent it to cover a balance on an account are a very big part of commercial fraud. Fraudsters may actually make multiple payments, playing the timing game so they keep the account and the account balance alive and growing, or the credit balance on the account so that they can perhaps get more from the fraudulent credit relationship that they’ve built than the intended credit line by this timing and submission of payments. They can do this for several industries. They can do this for all different kinds of payment items themselves. They could be done with forged paper checks, electronic payments, and sometimes counterfeit payments themselves.

[Gary]: Patricio, turning to you, would profit be impacted by implementing fraud prevention filters? I would imagine that would hinder some profitable growth?

[Patricio]: It’s a tricky one because, you know, there’s this big misconception that by applying fraud filters, that’s going to affect your profit or affect your number of applications going through. And it is true to an extent by applying fraud filters, you will see fewer applications going through. But affecting your profit, it’s the complete opposite. It’s actually going to reduce the losses that you’ll be incurring, and I briefly touched upon this in your previous question, but what many companies do when they’re not able to differentiate between credit losses and fraud losses, they tighten their decisioning in their credit applications. Those potentially good customers don’t make it through, but fraudsters make it through with no problem at all. Because the decisioning system that they have for credit purposes does not do much for mitigating the fraudsters.

[Patricio]: Many times, these companies don’t invest in fraud solutions until they’ve gotten this big hit from a fraud attack, at that point, it’s already too late. So, I would say that the best thing to do to help your profit is to be proactive because fraud can affect your profit if you get impacted. If you’re proactive about it, you can protect or reduce those fraud losses that you’re currently seeing as overall fraud, or losses that could be a fraud and not just credit losses.

[Gary]: What’s the number one step that commercial business, especially a small business can take to combat this wave of commercial fraud?

[Chris]: Awareness must be built into the culture and it must be built into the solution and how the firm deals with the solution because there’s no way to solve the fraud problem with a turnkey black box, turn it on, and forget it, we don’t have that. And we may not have that for many, many years.

[Gary]: Can you tell me more about the first payment defaults and how lenders are addressing that problem?

[Chris]: We spoke a bit about payments in general as a fraud channel, but this is a particularly aggressive form of fraud or credit abuse. And it happens when the borrowing party just never ever makes one payment on the account. They may utilize the entire credit line and they just don’t ever pay. So when the first payment is in default, there’s a high suspicion that this could be a fraudster. There’s a little ambiguity, as I said, but the credit and the fraud dimensions are rather close. They’re rather parallel, in terms of how they are dealt with.

[Chris]: What are we doing about accounts that are very brazen and do this on the first payment due? We evaluate the risk at the time of enrollment. This is very important, we don’t know, who’s not going to pay us the first time. So we need a tool that evaluates, in this case, we offer a score, a commercial first payment default score, which is very high performance and very friendly to the combined mix of consumer and commercial data that a firm might have. Second, it pays to look at the risk of the entire portfolio for first payment default periodically. Again, is done with a score, it could be the same score I mentioned. In the third category, if it’s necessary, the host firm may wish to use scoring the individual payment item, the check, the online payment as a fraud evaluation, which is done by a different set of scores to manually perform systemic checks.

[Gary]: So Patricio what are some of the most common misunderstandings in fraud prevention products?

[Patricio]: Fraud filters will affect the number of applications that you are able to approve. As we mentioned before, it does affect the number of applications that you’ll see come through, but it will help increase your profit by incurring fewer losses. Again, fewer fraudsters make it through equals fewer losses coming into your system. The second one would be that most fraud can be solved by verifying the identity of the user. And sure, it’s because third-party fraud solutions are very popular, but that’s not going to help you with all types of fraud. That’s why you do need a layered approach for mitigating what’s going to come through the door because, at the end of the day, you don’t know what type of fraud you’re going to be seeing.

[Patricio]: By implementing a solution that will verify the identity of the user, that’s not going to help you fight all types of fraud. In fact, stand-alone, you will do very little to mitigate first-party fraud and likewise with synthetic fraud. So again, if the way to solve fraud is not with a one size fits all approach, it’s layered whether you have the resources and the capacity to implement a geolocation verification, or verify the validity of the data or verify the identity of the business owner. These are all things that are just going to prevent and help you weed out the different types of application fraud that you could see (coming) through the door.

[Gary]: Chris, what can small businesses do to engage with Experian and minimize their fraud exposure?

[Chris]: We love to talk, especially to small businesses on a very global scale in terms of their business operations and where it is that we might be able to help them. They may come to us with a great deal of awareness that they have a fraud problem and they kind of know where it is, but they look for a specific solution. Other small businesses may come to us with general concern. And in those, and in other cases, we are happy to sit down with them and do what I would call a free consultation and look at their information and make some suggestions.

[Chris]: What we do is we offer solutions, but we like to add to that the knowledge of the particular client’s situation, so that they become wiser and they become enabled by the kind of services that we provide, and they become enabled by the information we can bring to them upfront so they can make a wise consumer solution as it were.

[Gary]: Well fraud in the payment protection program or the PPP program is all over the news. What do you make of that? Are these fraudulent applications affecting lenders, even though the losses would be absorbed by the government?

[Patricio]: While many of these lenders know and think that the loss of the potential losses would be absorbed by the government, the reality is that it’s uncovering many gaps for these lenders. First, we understand there’s a greater volume of applications going through their systems. So what many of these lenders have done is either turn off, completely turn off their fraud mitigation systems, or they’ve reduced the amount of vetting that they do, because they’re not too worried because they know that the government is going to absorb those losses because of the volume of applications that they see. Now, the problem with that is that if they completely turned off the system, now they have potential fraudsters within their portfolio, or on the other hand, if they lessened the amount of filtering that they do, and yet still some fraudsters make it through, it’s going to be very hard to weed out those fraudsters down the line. It’s just putting more risk to your overall portfolio, and, people, once they’re in there, they’ve already uncovered some gaps in your underwriting process. So again, just down the line is going to be very hard to weed out these fraudsters that made it through your portfolio,

[Gary]: Chris, anything to add?

[Chris]: That was a good summary. I would add only that the other side of the coin is when you put many, many tens of millions of good Government money into the hands of fraudsters, you’re sort of inflating the entire credit system. You’re allowing bad people to get what appears to be credit for good loans until they’re discovered. Many of these will probably not be discovered. So you’re kind of adding bads to the system and calling them goods. And that’s never good for all of us.

[Gary]: Well, this has been very helpful guys. I want to say thank you very much for coming on Business Chat and sharing your insights.

Related Posts

Experian chats with Giggle Finance Co-Founder about funding gig workers while managing risk and how AI is helping them to scale quickly.

Experian experts discuss effective marketing strategies for insurance agents and brokers to boost ROI and client engagement.

Experian discusses record business creation and fraud strategy with Credibly Founder and Co-CEO Ryan Rosett.