Business Credit Education

articles and videos about business credit education

The experts at BBVA bank and Experian have teamed up to bring you an educational webinar on the power of building and maintaining business credit.

Experian spoke with women small business owners about how they use business credit for their business. Learn more about the Women in Business Study.

Here are some business credit answers on establishing and building a strong credit profile for your small business. Learn more at http://bit.ly/2ZNyRnV

What is business credit? See how a good business credit score can help strengthen and protect your business.

The commitment required to apply for a business loan may have you on the fence, unsure of whether or not to move forward. You’re not wrong to be cautious

In this post we outline best practices for establishing business credit. Just because you have a business, don't assume you have a business credit score.

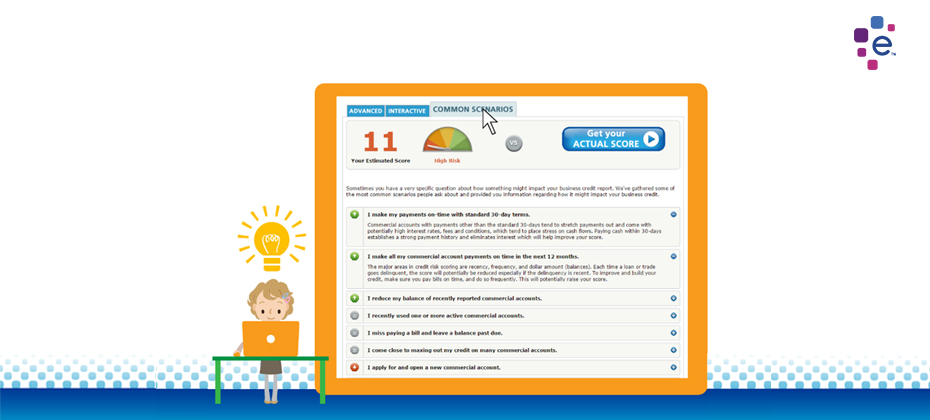

Experian has released a business credit score planner tool to help you run what-if scenarios. It helps you learn behaviors that build strong credit.

Learn more about business credit and how to build it, and why it's important to keep it separate from personal credit.

Debt Collection Scams Substantial debt can be a crippling burden to a small business, which is why they are often targeted by con artists who purport they can vastly reduce or even eliminate this debt — for a fee. This type of scam has a long and checkered history — and is showing no sign of abating. In late October of 2016, Ukrainian-born Sergiy Bezrukov — aka John Butler aka Thomas Paris aka Christopher Riley — was arrested by the FBI in upstate New York and charged with mail fraud for having allegedly duped more than 100 small business owners out of more than $500,000. His alleged scheme was simple: mass-mail an offer to reduce small business debt by up to 75 percent in just six to 12 hours. The fee for his services — required upfront — was $1,250, to be sent via wire transfer to his company, Corporate Restructure, Inc. Of course, no actual services were performed. Victims were not only out their initial $1,250, but many had their credit ratings seriously damaged — or further damaged — as a result. “Bogus credit relief schemes are not all that common, but when they do pop up, they give legitimate organizations a bad name,” said Robert Tharnish, senior vice president of ABC-Amega, Inc., a debt collection agency headquartered in Buffalo, N.Y. “There are many ways to deal with commercial debt. Owners just have to do their due diligence.” Robert Ingold, CEO of Commercial Collection Corp. in Tonawanda, N.Y., agrees. “For anyone who receives a solicitation to reduce their debt — be it commercial or consumer — be skeptical. Know who you’re dealing with.” Both Tharnish and Ingold serve on the board of the International Association of Commercial Collectors, the world’s largest international trade association for commercial debt collection professionals. Ingold noted that most companies have accountants and attorneys who should immediately raise a red flag when such sketchy offers come their way. Even so, enough small business owners either don’t have outside help or ignore their paid experts’ advice, allowing scammers like Berzukov to rake in hundreds of thousands of dollars in just a few months’ time. Dealing with a bogus agency can damage already fragile credit ratings, Ingold noted. “In most cases, a company targeted by a debt reduction scammer has debt and delinquencies that have already been noted by reporting agencies like Experian. Bezrukov’s victims weren’t just out their $1,250, but they probably fell further behind in their debt payments expecting relief, and this just decreased their business credit scores even further.” “This is an industry where all you need is a phone and list,” Ingold continued. “We see the same problem on the flip side with fraudulent collection agencies. Fly-by-night collection agencies approach lenders with wild claims of collection prowess, or buy existing paper for pennies on the dollar, then start harassing debtors in violation of all established laws and ethics.” “ Both Ingold and Tharnish noted that the legal system has numerous avenues available for businesses that find themselves over their head in debt. These include: Restructuring the debt with the existing creditors. This often includes devising a monthly payment plan that leaves the business with enough capital to keep growing. Getting an SBA or private business loan. Declaring Chapter 11 or Chapter 13 bankruptcy, which allow businesses to discharge many of their obligations and still keep their doors open. Both experts also emphasized the need for business owners to perform due diligence before hiring any debt reduction or collection agency to work on their behalf. “Ask to see their license. Their certification. Check with the Better Business Bureau,” Tharnish advised. “Also demand references. Ask, ‘Have you done business with anyone I know?’ If an agency can’t provide references, just walk away.” “When confronted with an amazing business solicitation, just remember the old saying,” Tharnish concluded. “If it sounds too good to be true, it probably is.”