700 Credit Score: Is it Good or Bad?

Your score falls within the range of scores, from 670 to 739, which are considered Good. The average U.S. FICO® ScoreΘ, 714, falls within the Good range. Lenders view consumers with scores in the good range as "acceptable" borrowers, and may offer them a variety of credit products, though not necessarily at the lowest-available interest rates.

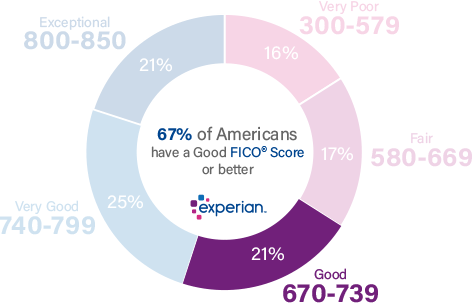

21% of U.S. consumers' FICO® Scores are in the Good range.

Approximately 9% of consumers with Good FICO® Scores are likely to become seriously delinquent in the future.

How to improve your 700 Credit Score

A FICO® Score of 700 provides access to a broad array of loans and credit card products, but increasing your score can increase your odds of approval for an even greater number, at more affordable lending terms.

Additionally, because a 700 FICO® Score is on the lower end of the Good range, you'll probably want to manage your score carefully to prevent dropping into the more restrictive Fair credit score range (580 to 669).

33% of consumers have FICO® Scores lower than 700.

The best way to determine how to improve your credit score is to check your FICO® Score. Along with your score, you'll receive information about ways you can boost your score, based on specific information in your credit file. You'll find some good general score-improvement tips here.

Understand the benefits of a good credit score

A credit score in the good range may reflect a relatively short credit history marked by good credit management. It may also characterize a longer credit history with a few mistakes along the way, such as occasional late or missed payments, or a tendency toward relatively high credit usage rates.

Late payments (past due 30 days) appear in the credit reports of 52% of people with FICO® Scores of 700.

Lenders see people with scores like yours as solid business prospects. Most lenders are willing to extend credit to borrowers with credit scores in the good range, although they may not offer their very best interest rates, and card issuers may not offer you their most compelling rewards and loyalty bonuses.

Staying the course with your Good credit history

Having a Good FICO® Score makes you pretty typical among American consumers. That's certainly not a bad thing, but with some time and effort, you can increase your score into the Very Good range (740-799) or even the Exceptional range (800-850). Moving in that direction will require understanding of the behaviors that help grow your score, and those that hinder growth:

Late and missed payments are among the most significant influences on your credit score—and they aren't good influences. Lenders want borrowers who pay their bills on time, and statisticians predict that people who have missed payments likelier to default (go 90 days past due without a payment) on debt than those who pay promptly. If you have a history of making late payments (or missing them altogether), you'll do your credit score a big solid by kicking that habit. More than one-third of your score (35%) is influenced by the presence (or absence) of late or missed payments.

Utilization rate, or usage rate, is a technical way of describing how close you are to "maxing out" your credit card accounts. You can measure utilization on an account-by-account basis by dividing each outstanding balance by the card's spending limit, and then multiplying by 100 to get a percentage. Find your total utilization rate by adding up all the balances and dividing by the sum of all the spending limits:

| Balance | Spending limit | Utilization rate (%) | |

|---|---|---|---|

| MasterCard | $1,200 | $4,000 | 30% |

| VISA | $1,000 | $6,000 | 17% |

| American Express | $3,000 | $10,000 | 30% |

| Total | $5,200 | $20,000 | 26% |

Most experts agree that utilization rates in excess of 30%—on individual accounts and all accounts in total—will push credit scores downward. The closer you get to “maxing out” any cards—that is, moving their utilization rates toward 100%—the more you hurt your credit score. Utilization is second only to making timely payments in terms of influence on your credit score; it contributes nearly one-third (30%) of your credit score.

It's old but it's good. All other factors being the same, the longer your credit history, the higher your credit score likely will be. That doesn't help much if your recent credit history is bogged down by late payments or high utilization, and there's little you can do about it if you're a new borrower. But if you manage your credit carefully and keep up with your payments, your credit score will tend to increase over time. Age of credit history is responsible for as much as 15% of your credit score.

New credit activity typically has a short-term negative effect on your credit score. Any time you apply for new credit or take on additional debt, credit-scoring systems determine that you are greater risk of being able to pay your debts. Credit scores typically dip a bit when that happens, but rebound within a few months as long as you keep up with your bills. Because of this factor, it's a good idea to "rest" six months or so between applications for new credit—and to avoid opening new accounts in the months before you plan to apply for a major loan such as a mortgage or an auto loan. New-credit activity can contribute up to 10% of your overall credit score.

A variety of credit accounts promotes credit-score improvements. The FICO® credit scoring system tends to favor individuals with multiple credit accounts, including both revolving credit (accounts such as credit cards that enable you to borrow against a spending limit and make payments of varying amounts each month) and installment loans (e.g., car loans, mortgages and student loans, with set monthly payments and fixed payback periods). Credit mix accounts for about 10% of your credit score.

60% of individuals with a 700 FICO® Score have credit portfolios that include auto loan. 36% have a mortgage.

Public records such as bankruptcies do not appear in every credit report, so these entries cannot be compared to other score influences in percentage terms. If one or more is listed on your credit report, it can outweigh all other factors and severely lower your credit score. For example, a bankruptcy can stay on your credit report for 10 years, and may shut you out of access to many types of credit for much or all of that time.

How to build up your credit score

Your FICO® Score is solid, and you have reasonably good odds of qualifying for a wide variety of loans. But if you can improve your credit score and eventually reach the Very Good (740-799) or Exceptional (800-850) credit-score ranges, you may become eligible for better interest rates that can save you thousands of dollars in interest over the life of your loans. Here are few steps you can take to begin boosting your credit scores.

Check your FICO ScoreFICO® regularly. Tracking your FICO® Score can provide good feedback as you work to build up your score. Recognize that occasional dips in score are par for the course, and watch for steady upward progress as you maintain good credit habits. To automate the process, you may want to consider a credit-monitoring service. You also may want to look into an identity theft-protection service that can flag suspicious activity on your credit reports.

Avoid high credit utilization rates. High credit utilization, or debt usage. Try to keep your utilization across all your accounts below about 30% to avoid lowering your score.

Consumers with a 700 FICO® Score have an average of 4.7 credit card accounts.

Seek a solid credit mix. No one should take on debt they don’t need, but prudent borrowing—in the form of revolving credit and installment loans—can promote good credit scores.

Pay your bills on time. You’ve heard it before, but there’s no better way to boost your credit score, so find a system that works for you and stick with it. Automated tools such as smartphone reminders and automatic bill-payment services work for many, sticky notes and paper calendars, for others. After six months or so, you may find yourself remembering without help. (Keep the system going anyway, just in case.)

Learn more about your credit score

A 700 FICO® Score is Good, but by raising your score into the Very Good range, you could qualify for lower interest rates and better borrowing terms. A great way to get started is to get your free credit report from Experian and check your credit score to find out the specific factors that impact your score the most. Read more about score ranges and what a good credit score is.