Welcome to the Experian Thought Leadership Hub

Gain insights into the fast-changing world of consumer and business data through our extensive library of resources.

Gain insights into the fast-changing world of consumer and business data through our extensive library of resources.

418 resultsPage 1

Report

Report

See how a single attacker leveraged fraud ring tactics to compromise over 50 accounts in under 30 days—and how to detect and stop solo account takeover attacks at scale.

Key insights:

Report

Report

Consumers have powered the U.S. economy through repeated shocks, but new pressures are testing their resilience. As energy prices rise and economic conditions shift, the outlook is becoming more uncertain.

Report

Report

Explore how modern fraudsters use coordinated, strategic attack methods—and learn how to detect, disrupt and prevent them using behavioral intelligence and real-time insights.

Key insights:

Report

Report

Uncover a coordinated account takeover fraud ring in action and learn how it was stopped using behavioral, device and network intelligence.

Key insights:

Infographic

Infographic

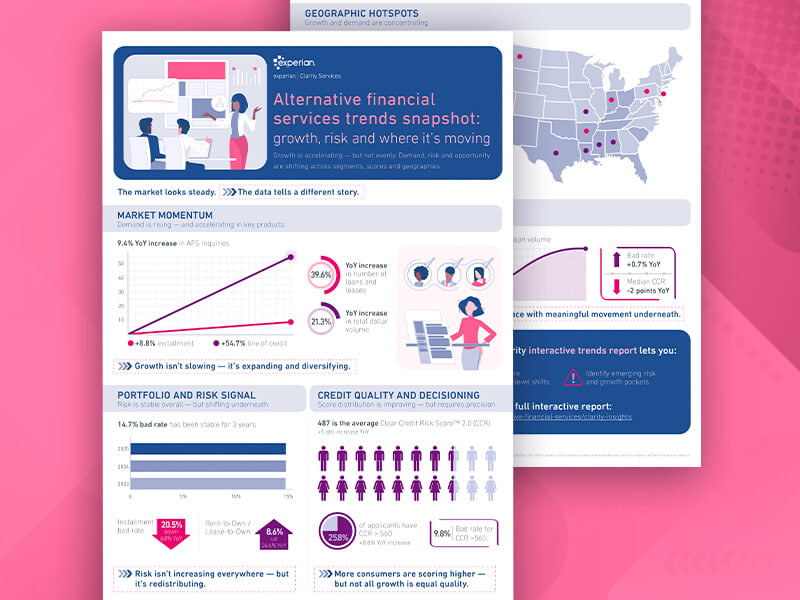

Download the latest Alternative Financial Services Trend Report to reveal new insights on growth and risk, including:

Webinar

Webinar

In this webinar, Experian experts explore how organizations can apply proven consumer fraud prevention tactics to strengthen commercial lending defenses.

What you'll learn:

Infographic

Infographic

Discover a faster, more efficient way to bring financial wellness and privacy solutions to market. Learn how to:

Case Study

Case Study

Education Credit Union modernized underwriting with Experian’s Advanced Decisioning—driving faster decisions, stronger approvals, and rapid ROI in a competitive market.

Webinar

Webinar

Gain a clearer view of how consumers earn, spend, and manage their money in today’s evolving economic landscape. In this webinar, Experian experts break down the financial behaviors shaping demand, risk, and growth—using macroeconomic trends, credit data, and transaction-level cash flow insights.

The latest insights, tips, and trends on all things related to commercial risk by the Experian Business Information Services team.

Experian Employer Services’ HR, payroll and tax experts share news, insights and best practices for employer compliance topics and challenges.

Experian's Global News Blog is your go-to source for the latest news, insights and trends in the world of data and analytics.

Experian Health’s blog features the latest trends and insights shaping the future of healthcare.

Helping businesses make faster, smarter, and more inclusive decisions with the power of data, analytics, and technology.

Marketing insights and solutions to help you drive more meaningful interactions so your consumers can connect, engage, and thrive.

Small business advice and credit education, news, and trends.